In case you desire to fill out Form 5884, it's not necessary to download and install any sort of software - simply give a try to our online tool. In order to make our tool better and easier to work with, we constantly come up with new features, with our users' suggestions in mind. Getting underway is easy! All you need to do is adhere to these basic steps down below:

Step 1: Press the "Get Form" button in the top part of this webpage to open our tool.

Step 2: After you start the file editor, you'll notice the document made ready to be filled out. Besides filling in various blank fields, you may also perform other actions with the form, namely putting on any textual content, editing the initial textual content, inserting graphics, affixing your signature to the document, and much more.

For you to complete this document, make certain you enter the information you need in each and every area:

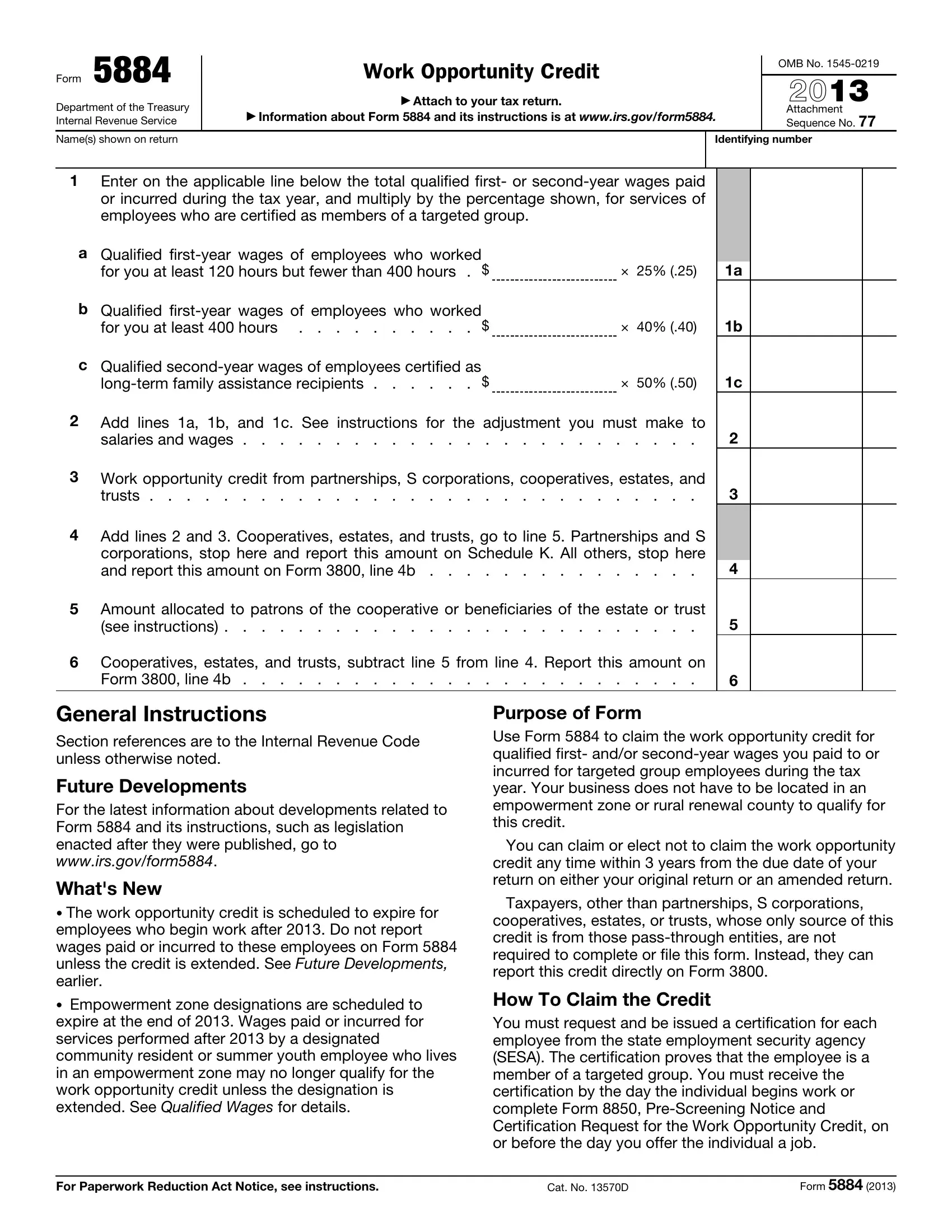

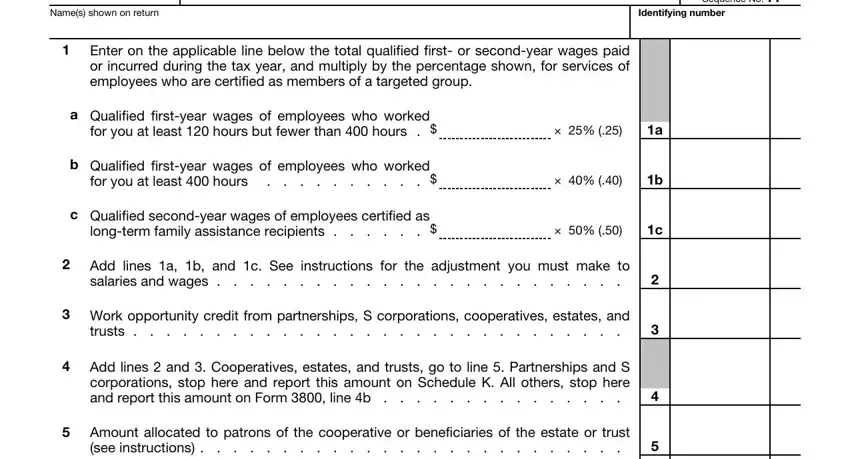

1. The Form 5884 necessitates specific details to be typed in. Make sure the next blank fields are finalized:

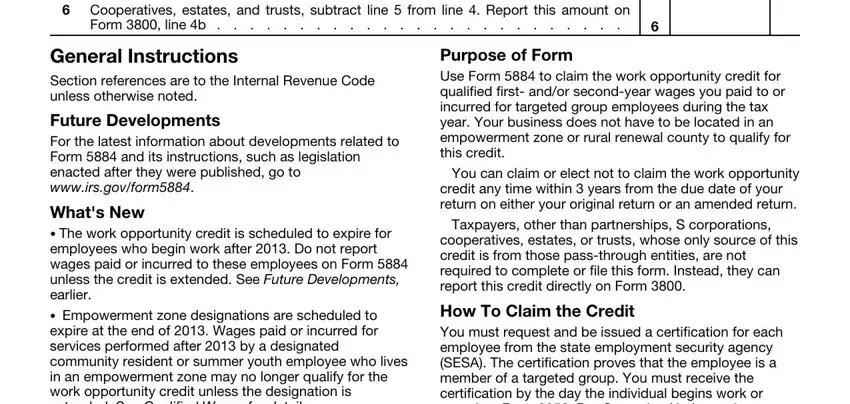

2. Once your current task is complete, take the next step – fill out all of these fields - Cooperatives estates and trusts, Form line b, General Instructions Section, Future Developments For the latest, Whats New The work opportunity, Purpose of Form Use Form to claim, You can claim or elect not to, credit any time within years from, Taxpayers other than partnerships, cooperatives estates or trusts, and How To Claim the Credit You must with their corresponding information. Make sure to double check that everything has been entered correctly before continuing!

Always be extremely mindful when completing You can claim or elect not to and Taxpayers other than partnerships, because this is where a lot of people make errors.

Step 3: Check that the details are right and just click "Done" to finish the project. Join FormsPal right now and instantly access Form 5884, ready for download. Every last change you make is handily saved , helping you to modify the file later as needed. FormsPal ensures your data privacy via a secure method that never records or shares any type of personal information used. Rest assured knowing your documents are kept confidential whenever you work with our service!