If you're a U.S. citizen or resident and made over $100,000 in freelance income last year, then you're required to file Form 8885 with your tax return. This form is used to calculate and report your self-employment taxes, and it's important to make sure you complete it correctly. In this post, we'll walk you through the basics of Form 8885 and show you how to correctly fill it out. We'll also outline some common mistakes people make when filing this form, so that you can avoid them!

| Question | Answer |

|---|---|

| Form Name | Form 8885 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | f8885 2010 form 8885 |

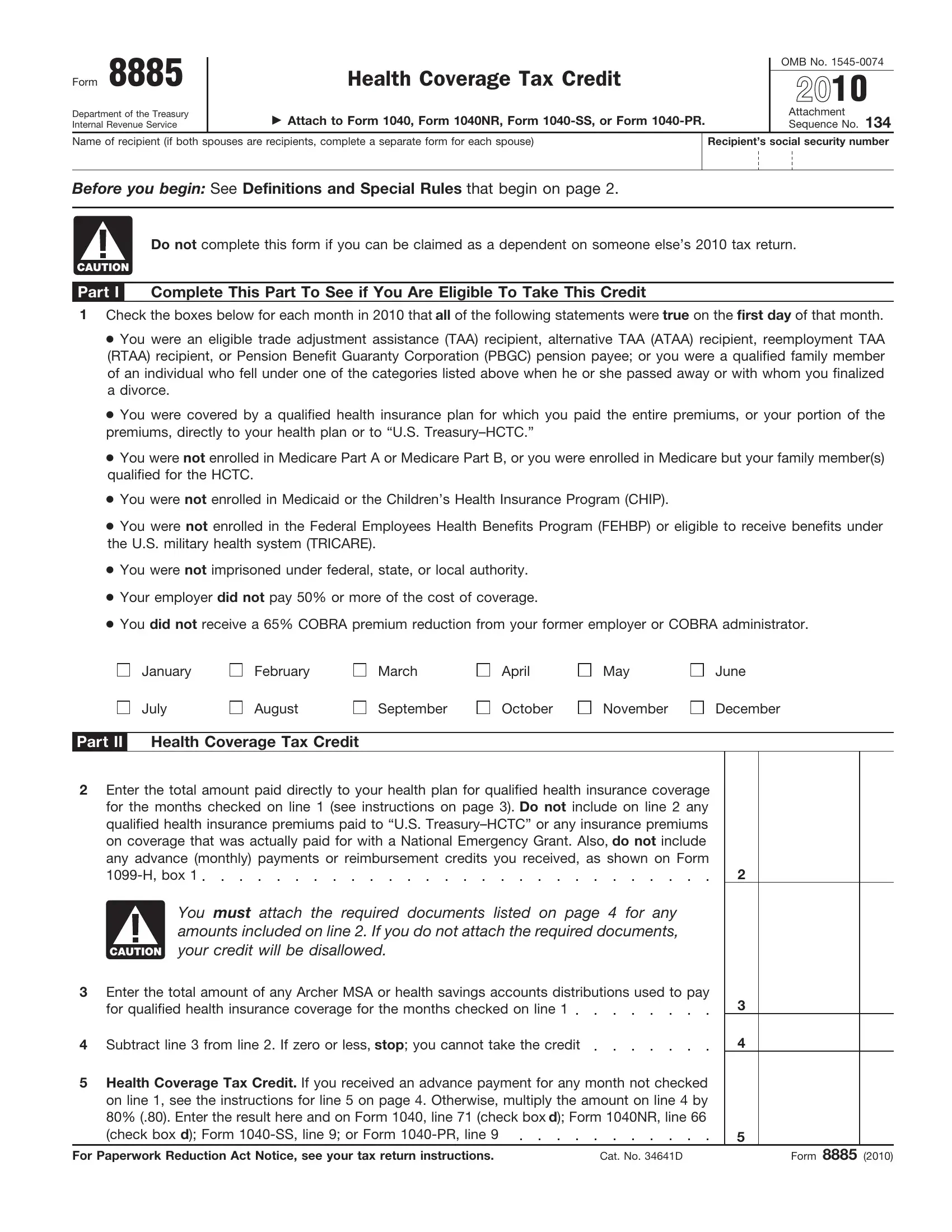

Form 8885

Department of the Treasury Internal Revenue Service

Health Coverage Tax Credit

▶Attach to Form 1040, Form 1040NR, Form

OMB No.

2010

Attachment Sequence No. 134

Name of recipient (if both spouses are recipients, complete a separate form for each spouse)

Recipient’s social security number

Before you begin: See Definitions and Special Rules that begin on page 2.

Do not complete this form if you can be claimed as a dependent on someone else’s 2010 tax return.

CAUTION

Part I Complete This Part To See if You Are Eligible To Take This Credit

1Check the boxes below for each month in 2010 that all of the following statements were true on the first day of that month.

●You were an eligible trade adjustment assistance (TAA) recipient, alternative TAA (ATAA) recipient, reemployment TAA (RTAA) recipient, or Pension Benefit Guaranty Corporation (PBGC) pension payee; or you were a qualified family member of an individual who fell under one of the categories listed above when he or she passed away or with whom you finalized a divorce.

●You were covered by a qualified health insurance plan for which you paid the entire premiums, or your portion of the premiums, directly to your health plan or to “U.S.

●You were not enrolled in Medicare Part A or Medicare Part B, or you were enrolled in Medicare but your family member(s) qualified for the HCTC.

●You were not enrolled in Medicaid or the Children’s Health Insurance Program (CHIP).

●You were not enrolled in the Federal Employees Health Benefits Program (FEHBP) or eligible to receive benefits under the U.S. military health system (TRICARE).

●You were not imprisoned under federal, state, or local authority.

●Your employer did not pay 50% or more of the cost of coverage.

●You did not receive a 65% COBRA premium reduction from your former employer or COBRA administrator.

January

July

February

August

March

September

April

October

May

November

June

December

Part II Health Coverage Tax Credit

2Enter the total amount paid directly to your health plan for qualified health insurance coverage for the months checked on line 1 (see instructions on page 3). Do not include on line 2 any qualified health insurance premiums paid to “U.S.

on coverage that was actually paid for with a National Emergency Grant. Also, do not include |

|

any advance (monthly) payments or reimbursement credits you received, as shown on Form |

|

2 |

You must attach the required documents listed on page 4 for any amounts included on line 2. If you do not attach the required documents,

CAUTION your credit will be disallowed.

3Enter the total amount of any Archer MSA or health savings accounts distributions used to pay

for qualified health insurance coverage for the months checked on line 1 |

3 |

4 Subtract line 3 from line 2. If zero or less, stop; you cannot take the credit |

4 |

5Health Coverage Tax Credit. If you received an advance payment for any month not checked on line 1, see the instructions for line 5 on page 4. Otherwise, multiply the amount on line 4 by 80% (.80). Enter the result here and on Form 1040, line 71 (check box d); Form 1040NR, line 66

(check box d); Form |

|

5 |

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 34641D |

Form 8885 (2010) |

Form 8885 (2010) |

Page 2 |

|

|

General Instructions

Section references are to the Internal Revenue Code unless otherwise noted.

Purpose of Form

Use Form 8885 to figure the amount, if any, of your health coverage tax credit (HCTC).

Who Can Take This Credit

You can take this credit only if (a) you were an eligible trade adjustment assistance (TAA) recipient, alternative TAA (ATAA) recipient, reemployment TAA (RTAA) recipient, or Pension Benefit Guaranty Corporation (PBGC) pension payee in 2010; or you were the family member of a TAA, ATAA, or RTAA recipient or PBGC payee who passed away or with whom you finalized a divorce in 2010, (b) you cannot be claimed as a dependent on someone else’s 2010 tax return, and (c) you met all of the other conditions listed on line 1. If you cannot be claimed as a dependent on someone else’s 2010 tax return, complete Form 8885, Part I, to see if you are eligible to take this credit.

Definitions and Special Rules

TAA Recipient

You were an eligible TAA recipient on the first day of the month if, for any day in that month or the prior month, you:

●Received a trade readjustment allowance, or

●Would have been entitled to receive such an allowance except that you had not exhausted all rights to any unemployment insurance (except additional compensation that is funded by a state and is not reimbursed from any federal funds) to which you were entitled (or would be entitled if you applied).

Example. You received a trade readjustment allowance for January 2010. You were an eligible TAA recipient on the first day of January and February.

ATAA Recipient

You were an eligible ATAA recipient on the first day of the month if, for that month or the prior month, you received benefits under an alternative trade adjustment assistance program for older workers established by the Department of Labor.

Example. You received benefits under an alternative trade adjustment assistance program for older workers for October 2010. The program was established by the Department of Labor. You were an eligible ATAA recipient on the first day of October and November.

RTAA Recipient

You were an eligible RTAA recipient on the first day of the month if, for that month or the prior month, you received benefits under a reemployment trade adjustment assistance program for older workers established by the Department of Labor.

Example. You received benefits under a reemployment trade adjustment assistance program for older workers for October 2010. The program was established by the Department of Labor. You were an eligible RTAA recipient on the first day of October and November.

PBGC Pension Payee

You were an eligible PBGC pension payee on the first day of the month, if both of the following apply.

1.You were age 55 or older on the first day of the month.

2.You received a benefit for that month that was paid by the

PBGC under title IV of the Employee Retirement Income Security Act of 1974 (ERISA).

If you received a

Family Members in Certain Life Events

Family members (spouses and dependents) are eligible to receive the HCTC for any month through December 31, 2010, from the month a TAA, ATAA, RTAA recipient or PBGC payee died or with whom you finalized a divorce.

Example. Your spouse was a PBGC payee and died on August 20, 2010. You are eligible to receive the HCTC for August through December 2010.

Qualified Health Insurance Plan

A qualified health insurance plan is any of the following.

1.Coverage under a group health plan available through the employment of your spouse. But see the instructions for line 1 on page 3.

2.Coverage under individual health insurance if you were covered under individual health insurance during the entire

3.Coverage under a COBRA continuation provision (as defined in section 9832(d)(1)).

Note. As of February 2009, electing to receive the 65% COBRA premium reduction will disqualify you from receiving the HCTC in the same month. You must pay more than 50% of your COBRA coverage to be eligible for the HCTC.

4.Coverage under a

a. Continuation coverage provided by the state under a state law that requires such coverage.

b. A qualified state high risk pool (as defined in section 2744(c)(2) of the Public Health Service Act).

c. A health insurance program offered for state employees.

d. A

e. An arrangement entered into by a state and (a) a group health plan (including such a plan which is a multiemployer plan as defined in section 3(37) of ERISA), (b) an issuer of health insurance coverage,

(c)an administrator, or (d) an employer.

f.A state arrangement with a private sector health care coverage purchasing pool.

g.A

Exception. A qualified health insurance plan does not include any of the following.

●Any

●A flexible spending or similar arrangement.

●Any insurance if substantially all of its coverage is of excepted benefits described in section 9832(c). For example, if you purchase dental or vision benefits separately, these benefits are not part of a qualified health insurance plan for the HCTC. But, if you purchase dental or vision benefits as part of a comprehensive package and these benefits do not represent substantially all of its coverage, these benefits may be part of a qualified health insurance plan and the premiums paid may be eligible for the HCTC.

If you are not sure whether your health insurance plan is a qualified health insurance plan, go to IRS.gov, enter

TIP HCTC Additional Resources for Individuals in the search box and link to the HCTC Program Kit found under that heading. You can also contact the HCTC Customer Contact Center

at

Form 8885 (2010) |

Page 3 |

|

|

Qualifying Family Member

A qualifying family member is:

●Your spouse (but see Married Persons Filing Separate Returns below), or

●Anyone whom you can claim as a dependent (but see the exception for Children of Divorced or Separated Parents below).

For any month that you are eligible to claim the HCTC, you can

include premiums paid for a qualifying family member for that month if all of the following statements were true as of the first day of that month.

●The qualifying family member was covered by a qualified health insurance plan (defined earlier) for which you paid the premiums. You and your qualifying family member do not have to be covered by the same plan.

●The qualifying family member was not enrolled in Medicare Part A, B, or C.

●The qualifying family member was not enrolled in Medicaid or the Children’s Health Insurance Program (CHIP).

●The qualifying family member was not enrolled in the Federal Employees Health Benefits Program (FEHBP) or eligible to receive benefits under the U.S. military health system (TRICARE).

●The qualifying family member was not covered by, or eligible for coverage under, any

Additionally, qualifying family members of TAA, ATAA, and RTAA recipients or PBGC payees who enrolled in Medicare in 2010 are eligible to receive the HCTC from the date of Medicare enrollment through December 31, 2010. In order to receive the HCTC, the family member must meet all of the requirements described above.

Married Persons Filing Separate Returns

Your spouse is not treated as a qualifying family member if your filing status is married filing separately and either (1) or (2) below applies.

1.Your spouse also was an eligible TAA recipient, ATAA recipient, RTAA recipient, or PBGC pension payee in 2010.

2.All of the following apply:

a.You lived apart from your spouse during the last 6 months of 2010.

b.A qualifying family member (other than your spouse) lived in your home for more than half of 2010.

c.You provided over half of the cost of keeping up your home.

Children of Divorced or Separated Parents

Even if you cannot claim your child as a dependent, he or she is treated as your qualifying family member for the HCTC if both of the following apply.

●You were the child’s custodial parent. This is the parent with whom the child lived for the greater number of nights in 2010. If the child was with each parent for an equal number of nights, the custodial parent is the parent with the higher adjusted gross income.

●The child’s other parent can claim the child as a dependent under the rules for children of divorced or separated parents (see the instructions for Form 1040, line 6c, or Pub. 501, Exemptions, Standard Deduction, and Filing Information, for details).

If both of the above apply, the child’s other parent cannot treat the child as a qualifying family member for the HCTC.

The child must also meet all of the other conditions of a qualifying family member defined above.

CAUTION

Specific Instructions

Line 1

(2) next apply.

1.You were covered under any

insurance plan (including any

2.You were an ATAA or RTAA recipient and either of the following applies.

a. You were eligible for coverage under any qualified health insurance plan (including any

b. You were covered under any qualified health insurance plan (including any

Any amounts contributed to the cost of coverage by you or your spouse on a

CAUTION

Check the boxes on line 1 for each month that, on the first day of the month, neither (1) nor (2) above applies and you met all of the other conditions listed on line 1.

Example 1. On October 1, 2010, your only health insurance coverage was under an

Example 2. Assume the same facts as in Example 1 except that the employer paid only 25% of the cost of the coverage. The employer is considered to have paid 45% of the cost of the coverage (25% that was paid by the employer plus 20% that you paid through

●You were not eligible for coverage under any qualified health insurance plan (including any

●The plan was a type of plan listed under 3, 4a, or 4e in the definition of Qualified Health Insurance Plan on page 2.

●You met all of the other conditions listed on line 1.

Line 2

|

|

|

If your qualified health insurance plan covers anyone |

|

|

|

other than you and your qualifying family members, see |

|

|

|

Pub. 502, Medical and Dental Expenses (Including the |

CAUTION |

Health Coverage Tax Credit), before completing line 2. |

||

|

|||

Enter the total amount of insurance premiums paid for coverage for you and all qualifying family members under a qualified health insurance plan (as defined on page 2) for all months checked on line

1.But do not include any qualified health insurance premiums you paid to “U.S.

Example 1. You checked January on line 1. You paid $225 ($200 for basic coverage and $25 for dental benefits which are purchased separately) to your insurance company for coverage in January. The $25 you paid for dental benefits is ineligible for the HCTC. You would include the $200 you paid for your basic insurance on line 2.

Form 8885 (2010) |

Page 4 |

Example 2. Your insurance coverage for January cost $225 ($200 for basic coverage and $25 for dental benefits ineligible for the HCTC). You paid $65 to “U.S.

Required Documents

You must provide verifiable proof that your health insurance plan is qualified and that you paid the qualified health insurance premiums by attaching the documents listed below to your Form 8885.

All health plans. For all health plans you must include both of the following documents.

1.A copy of your health insurance bills or COBRA payment coupons.* The bills must have:

a. Your name (or name of the policy holder),

b. The name of your health plan,

c. Your monthly premium amount,

d. Dates of coverage, and

e. Your health plan identification number(s).

*If your qualified health plan does not provide members with an insurance bill or COBRA payment coupon, you must provide health plan enrollment documents or an official letter from your health plan that has the required information listed under 1a through 1e earlier. If your monthly premium includes amounts that do not count towards the HCTC, such as dental or vision coverage or coverage for family members who are not eligible for the HCTC, your documentation must also specify those ineligible amounts.

2. Proof of payment such as:**

a. Canceled checks (copy of front and back), b. Bank statements,

c. Credit card statements, or

d. Money orders.

**Your proof of payment must indicate the amount paid and to whom it was paid. If you do not have one of these types of proof of payment, contact your health plan for a record of your payment(s).

COBRA coverage. You must include the information under All health plans and one of the following documents.

1.A copy of your completed and signed COBRA Election Letter. It may also be called a COBRA Enrollment Form, Application Form, Enrollment Application for Continuing Coverage, or Election Agreement.

2.A letter from your former employer or COBRA administrator saying you have COBRA coverage. The letter must have:

a. The COBRA coverage start and end dates,

b. Name of the health plan,

c. Your home address, and

d. Covered family members, their dates of birth, their relationship to you, and their social security numbers.

3. A copy of “Notice of Rights to Continue Coverage.”

●A letter or other document from your former employer or your unemployment office that shows the date you left your job.

●A document from your health plan that shows your first date of coverage. Your first day of coverage in a

Coverage through your spouse’s employer. You must include the information under All health plans and the following documents.

●Copies of paycheck stubs showing the health coverage deductions for the qualified months.

●A letter or other statement from your spouse’s employer that states the employer contributed less than 50% of the cost of the coverage.

Example 1. You are eligible to claim the HCTC for October and November. You paid $500 of qualified health insurance premiums in each month for yourself and $250 for your qualifying family members. The amount on Form 8885, line 2, is $1,500 ($750 for October and $750 for November). You did not receive any HCTC advance payments during 2010. You must attach copies of your health insurance bills and proof of payment for you and your qualifying family members totaling $1,500, along with any other required documents. The bills and proof of payment should be for October and November.

Example 2. The facts are the same as in Example 1 except that, instead of paying the $750 premium for November, you paid $150 (20% of the $750 November premium) to “U.S.

Line 5

If you received an advance payment for any month not checked on line 1, you must reduce the amount on line 5 by the total of those advanced payments. If the result is less than zero, show the amount on line 5 as a negative number by enclosing it in parentheses. This amount is treated as an additional tax and must be treated as a positive amount and included in the total you enter on Form 1040, line 60; Form 1040NR, line 59; Form