Form Ct 1040Crc is the Connecticut tax form used by individuals to report their income and calculate the taxes they owe. This form must be filed by April 15th each year, and it covers income earned in the previous year. There are a number of schedules and worksheets that must be completed along with Form Ct 1040Crc, so it's important to understand all of the requirements before filing. Thankfully, our guide can help you walk through everything you need to know.

| Question | Answer |

|---|---|

| Form Name | Form Ct 1040Crc |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 2010, 1040crc, IRC, 2011 |

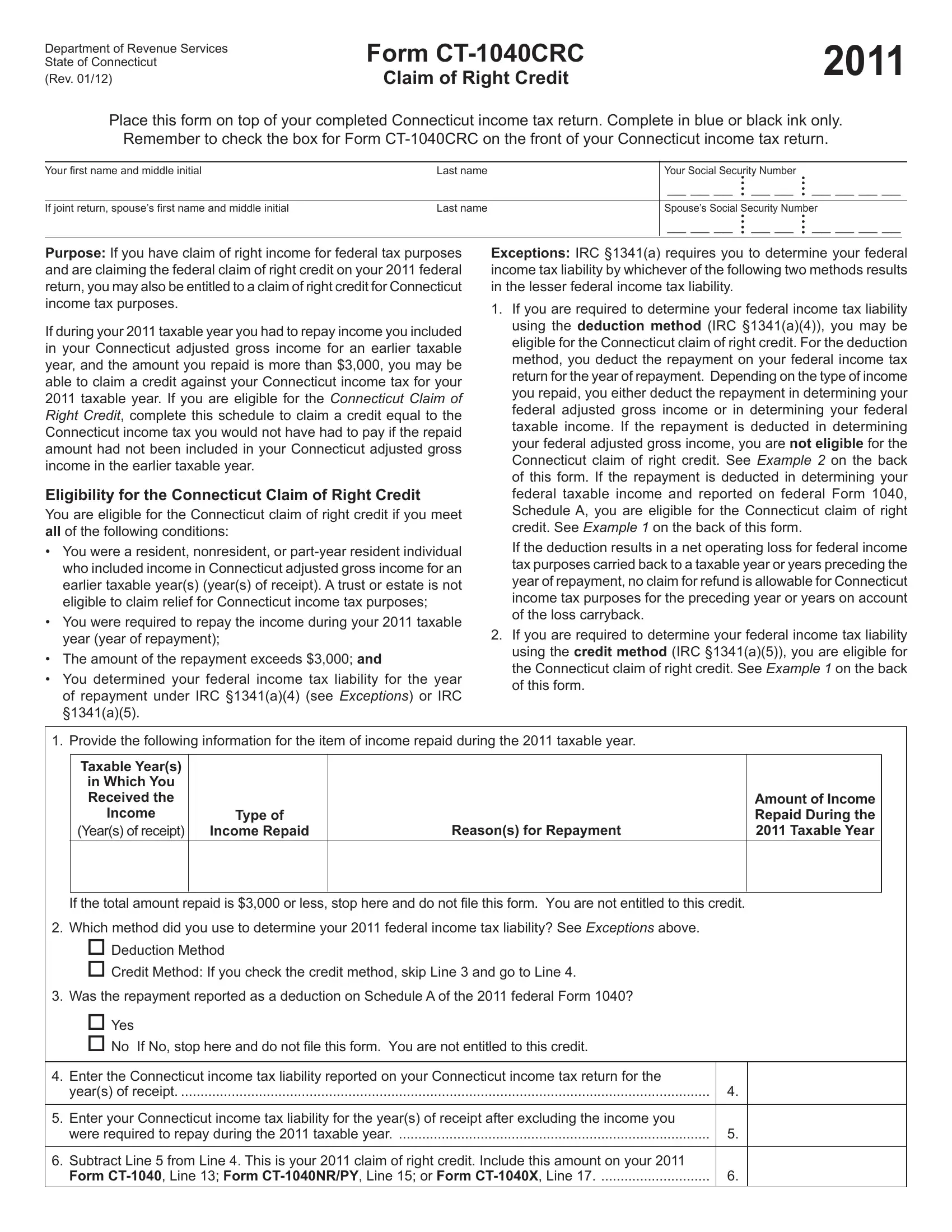

Department of Revenue Services State of Connecticut

(Rev. 01/12)

Form |

2011 |

Claim of Right Credit |

Place this form on top of your completed Connecticut income tax return. Complete in blue or black ink only. Remember to check the box for Form

Your fi rst name and middle initial |

Last name |

Your Social Security Number |

• |

|

|

||

|

|

|

• |

|

|

|

|

|

|

__ __ __ |

• |

__ __ |

• |

__ __ __ __ |

|

|

|

• |

• |

|

|||

|

|

|

• |

|

• |

|

|

If joint return, spouse’s fi rst name and middle initial |

Last name |

Spouse’s Social Security Number |

|||||

|

|

__ __ __ |

• |

__ __ |

• |

__ __ __ __ |

|

|

|

•• |

•• |

|

|||

|

|

|

• |

|

• |

|

|

Purpose: If you have claim of right income for federal tax purposes and are claiming the federal claim of right credit on your 2011 federal return, you may also be entitled to a claim of right credit for Connecticut income tax purposes.

If during your 2011 taxable year you had to repay income you included in your Connecticut adjusted gross income for an earlier taxable year, and the amount you repaid is more than $3,000, you may be able to claim a credit against your Connecticut income tax for your 2011 taxable year. If you are eligible for the Connecticut Claim of Right Credit, complete this schedule to claim a credit equal to the Connecticut income tax you would not have had to pay if the repaid amount had not been included in your Connecticut adjusted gross income in the earlier taxable year.

Eligibility for the Connecticut Claim of Right Credit

You are eligible for the Connecticut claim of right credit if you meet all of the following conditions:

•You were a resident, nonresident, or

•You were required to repay the income during your 2011 taxable year (year of repayment);

•The amount of the repayment exceeds $3,000; and

•You determined your federal income tax liability for the year of repayment under IRC §1341(a)(4) (see Exceptions) or IRC §1341(a)(5).

Exceptions: IRC §1341(a) requires you to determine your federal income tax liability by whichever of the following two methods results in the lesser federal income tax liability.

1.If you are required to determine your federal income tax liability using the deduction method (IRC §1341(a)(4)), you may be eligible for the Connecticut claim of right credit. For the deduction method, you deduct the repayment on your federal income tax return for the year of repayment. Depending on the type of income you repaid, you either deduct the repayment in determining your federal adjusted gross income or in determining your federal taxable income. If the repayment is deducted in determining your federal adjusted gross income, you are not eligible for the Connecticut claim of right credit. See Example 2 on the back of this form. If the repayment is deducted in determining your federal taxable income and reported on federal Form 1040, Schedule A, you are eligible for the Connecticut claim of right credit. See Example 1 on the back of this form.

If the deduction results in a net operating loss for federal income tax purposes carried back to a taxable year or years preceding the year of repayment, no claim for refund is allowable for Connecticut income tax purposes for the preceding year or years on account of the loss carryback.

2.If you are required to determine your federal income tax liability using the credit method (IRC §1341(a)(5)), you are eligible for the Connecticut claim of right credit. See Example 1 on the back of this form.

1. Provide the following information for the item of income repaid during the 2011 taxable year.

Taxable Year(s)

in Which You

Received the

Income

(Year(s) of receipt)

Type of

Income Repaid

Reason(s) for Repayment

Amount of Income

Repaid During the

2011 Taxable Year

If the total amount repaid is $3,000 or less, stop here and do not file this form. You are not entitled to this credit.

2.Which method did you use to determine your 2011 federal income tax liability? See Exceptions above.

Deduction Method

Credit Method: If you check the credit method, skip Line 3 and go to Line 4.

3.Was the repayment reported as a deduction on Schedule A of the 2011 federal Form 1040?

Yes

No If No, stop here and do not file this form. You are not entitled to this credit.

4. |

Enter the Connecticut income tax liability reported on your Connecticut income tax return for the |

|

|

|

year(s) of receipt |

4. |

|

|

|

|

|

5. |

Enter your Connecticut income tax liability for the year(s) of receipt after excluding the income you |

|

|

|

were required to repay during the 2011 taxable year |

5. |

|

|

|

|

|

6. |

Subtract Line 5 from Line 4. This is your 2011 claim of right credit. Include this amount on your 2011 |

|

|

|

Form |

6. |

|

|

|

|

|

Nonresidents or

If you are a nonresident or

Documentation Needed to Prove Eligibility for the Connecticut Claim of Right Credit

You must submit all of the following documentation with your 2011 Connecticut income tax return:

•A completed Form

•A copy of your completed 2011 federal income tax return, including all schedules and attachments, that you signed and filed for your 2011 taxable year;

•Proof you were required to repay income you included in Connecticut adjusted gross income for the year(s) of receipt, such as a letter from your employer requiring you to repay sales commissions;

•A copy of your completed federal income tax return, including all schedules and attachments, that you signed and filed for the year(s) of receipt; and

•Proof you repaid the income during your 2011 taxable year, such as a copy of your cancelled check.

How to Compute the Connecticut Claim of Right Credit

Your Connecticut income tax liability for the year of repayment is an amount equal to:

•The tax for the year of repayment computed as if there was no Connecticut claim of right credit; minus

•The decrease in tax for the year(s) of receipt that would result solely from the exclusion of the amount of income you were subsequently required to repay from your Connecticut adjusted gross income for the year(s) of receipt.

Line Instructions

Line 1: If you repaid income during your 2011 taxable year that you included in your Connecticut adjusted gross income for an earlier taxable year(s), enter:

•The year(s) of receipt;

•A description of the type of income repaid;

•The reason for the repayment; and

•The amount of income repaid. This income must have been included in your Connecticut adjusted gross income for the year(s) of receipt.

Line 2: Check the box to indicate if you used the deduction method or the credit method to determine your 2011 federal income tax liability. See Exceptions on the front for more information. If you checked the credit method, skip Line 3 and go to Line 4.

Line 3: Check the box to indicate if you reported the repayment as a deduction on Schedule A of your 2011 federal Form 1040.

Line 4: Enter the amount of your Connecticut income tax liability reported on your Connecticut income tax return for the year(s) of receipt. Enter the amount as originally filed, as adjusted by the Department of Revenue Services (DRS), or as you later amended it.

Line 5: Compute the amount of your Connecticut income tax liability for the year(s) of receipt after you exclude from your Connecticut adjusted gross income for the year(s) of receipt the income you repaid during your 2011 taxable year.

Repayments of Social Security benefits may require the recalculation of your taxable benefits to determine the amount to exclude from Connecticut adjusted gross income.

Line 6: Subtract Line 5 from Line 4. Include this amount on your 2011 Form

Example 1: In December 2010, James, a Connecticut resident, was advanced commissions by his employer. These commissions were included in his 2010 Connecticut adjusted gross income of $45,000. In May 2011, James’s employer advised him that some of his customers had decided to cancel their purchases and he must repay $4,000 of the commissions he received during 2010. If James was required to determine his federal income tax liability for the 2011 taxable year using the deduction method (IRC §1341(a)(4)), he would deduct the $4,000 as an itemized deduction on federal Form 1040, Schedule A. Assuming James’s filing status on his 2010 and 2011 Connecticut income tax returns is filing separately and his 2011 Connecticut adjusted gross income is $50,000, he computes his 2011 Connecticut income tax liability as follows:

2011 Connecticut income tax liability on $50,000 |

$ |

2,162 |

|

Minus difference between: |

|

|

|

2010 tax payable on $45,000 |

= $1,845 |

|

|

and |

|

|

|

2010 tax payable on $41,000 ($45,000 - $4,000) = $1,665 |

|

||

Claim of right credit |

– $ |

180 |

|

2011 Connecticut income tax liability |

|

$ |

1,982 |

If James was required to determine his federal income tax liability for the 2011 taxable year using the credit method (I.R.C. §1341(a)(5)), he would also compute his Connecticut income tax liability as shown above.

Example 2: In February 2010, Donna, a nonresident individual who works in Connecticut, realized a capital gain of $5,000 from the sale of a capital asset. The gain was not derived from or connected with Connecticut sources. Donna included the gain in her 2010 Connecticut adjusted gross income of $35,000. In September 2011, Donna was required to repay the purchaser of the assets $5,000 as a result of failure to fulfill conditions of the purchase agreement.

If Donna was required to determine her federal income tax liability for the 2011 taxable year using the deduction method (IRC §1341(a)(4)), she would deduct the repayment as a capital loss on her federal Form 1040, Schedule D. For Connecticut income tax purposes, Donna is not eligible for the claim of right credit because she deducted the repayment under IRC §1341(a)(4) in determining her federal adjusted gross income.

If Donna was required to determine her federal income tax liability using the credit method (IRC §1341(a)(5)), she is eligible for the Connecticut claim of right credit to the extent that her 2010 tax liability would be decreased as a result of excluding the $5,000 she subsequently repaid.

Form