Form Ct 2210 is an important legal form in Connecticut. It is used to create a written document that outlines the child custody agreement between the parents of a child. This form can be used to specify who will have physical and legal custody of the child, as well as set forth other important information such as visitation rights. It is important to note that both parents must sign this form for it to be legally binding. If you are considering filing for custody of a child, or if you are currently involved in a custody dispute, it is highly recommended that you consult with an attorney to ensure that your rights are protected.

| Question | Answer |

|---|---|

| Form Name | Form Ct 2210 |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | Connecticut, 2006, Underpayment, CT-1041 |

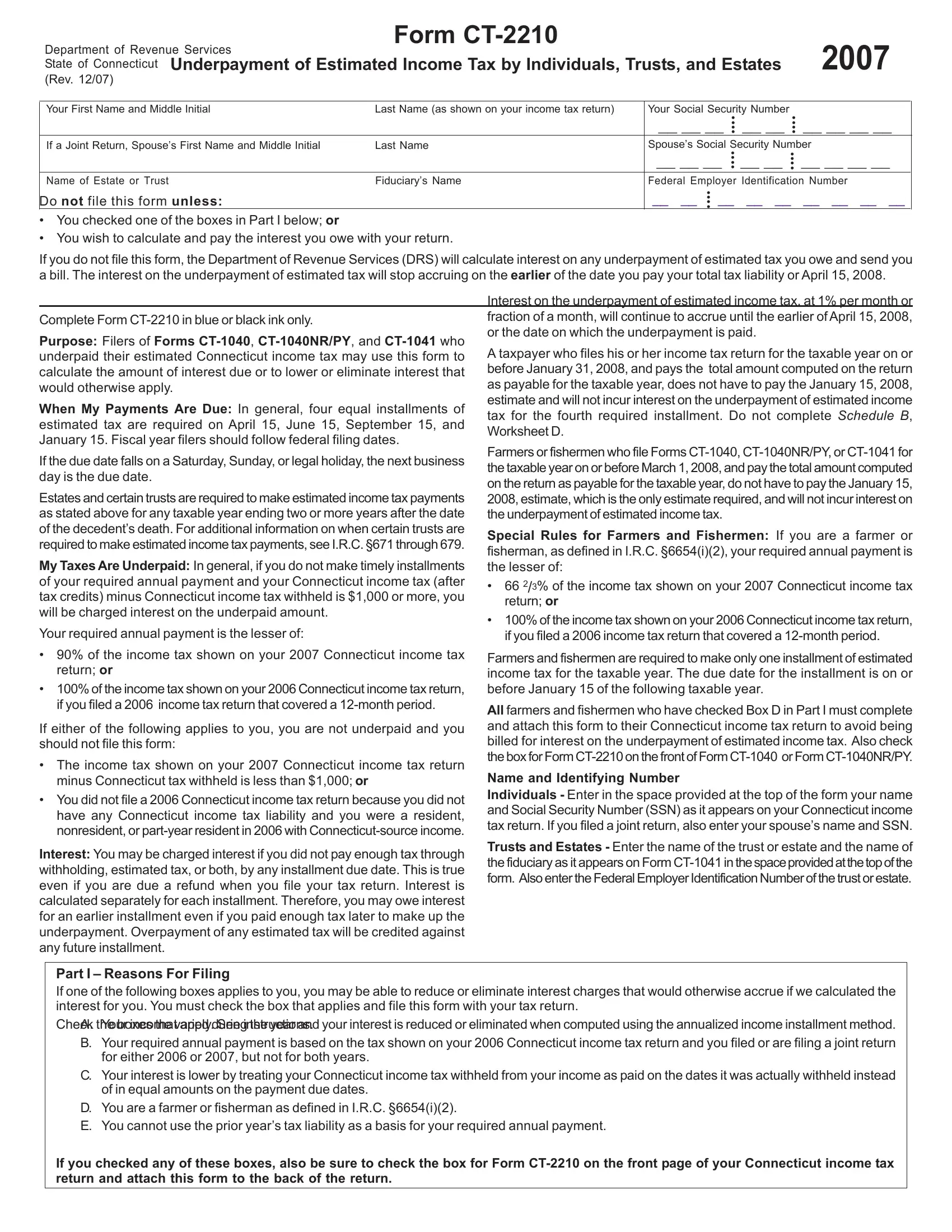

Department of Revenue Services State of Connecticut

Form |

2007 |

(Rev. 12/07) |

Underpayment of Estimated Income Tax by Individuals, Trusts, and Estates |

|

|

|||

|

|

|

||||

|

|

|

|

|

||

Your First Name and Middle Initial |

Last Name (as shown on your income tax return) |

Your Social Security Number |

|

|

||

|

|

|

• |

__ __ |

• |

__ __ __ __ |

|

|

|

__ __ __ •• |

•• |

||

|

|

|

• |

|

• |

|

If a Joint Return, Spouse’s First Name and Middle Initial |

Last Name |

Spouse’s Social Security Number |

||||

|

|

|

• |

__ __ |

• |

__ __ __ __ |

|

|

|

__ __ __ •• |

•• |

||

|

|

|

• |

|

• |

|

Name of Estate or Trust |

|

Fiduciary’s Name |

Federal Employer Identification Number |

|||

|

|

|

• |

__ __ |

__ __ __ __ |

|

|

|

|

__ __ •• __ |

|||

|

|

|

• |

|

|

|

Do not file this form unless:

•You checked one of the boxes in Part I below; or

•You wish to calculate and pay the interest you owe with your return.

If you do not file this form, the Department of Revenue Services (DRS) will calculate interest on any underpayment of estimated tax you owe and send you a bill. The interest on the underpayment of estimated tax will stop accruing on the earlier of the date you pay your total tax liability or April 15, 2008.

Complete Form

Purpose: Filers of Forms

When My Payments Are Due: In general, four equal installments of estimated tax are required on April 15, June 15, September 15, and January 15. Fiscal year filers should follow federal filing dates.

If the due date falls on a Saturday, Sunday, or legal holiday, the next business day is the due date.

Estates and certain trusts are required to make estimated income tax payments as stated above for any taxable year ending two or more years after the date of the decedent’s death. For additional information on when certain trusts are required to make estimated income tax payments, see I.R.C. §671 through 679.

My Taxes Are Underpaid: In general, if you do not make timely installments of your required annual payment and your Connecticut income tax (after tax credits) minus Connecticut income tax withheld is $1,000 or more, you will be charged interest on the underpaid amount.

Your required annual payment is the lesser of:

•90% of the income tax shown on your 2007 Connecticut income tax return; or

•100% of the income tax shown on your 2006 Connecticut income tax return, if you filed a 2006 income tax return that covered a

If either of the following applies to you, you are not underpaid and you should not file this form:

•The income tax shown on your 2007 Connecticut income tax return minus Connecticut tax withheld is less than $1,000; or

•You did not file a 2006 Connecticut income tax return because you did not have any Connecticut income tax liability and you were a resident, nonresident, or

Interest: You may be charged interest if you did not pay enough tax through withholding, estimated tax, or both, by any installment due date. This is true even if you are due a refund when you file your tax return. Interest is calculated separately for each installment. Therefore, you may owe interest for an earlier installment even if you paid enough tax later to make up the underpayment. Overpayment of any estimated tax will be credited against any future installment.

Interest on the underpayment of estimated income tax, at 1% per month or fraction of a month, will continue to accrue until the earlier of April 15, 2008, or the date on which the underpayment is paid.

A taxpayer who files his or her income tax return for the taxable year on or before January 31, 2008, and pays the total amount computed on the return as payable for the taxable year, does not have to pay the January 15, 2008, estimate and will not incur interest on the underpayment of estimated income tax for the fourth required installment. Do not complete Schedule B, Worksheet D.

Farmers or fishermen who file Forms

Special Rules for Farmers and Fishermen: If you are a farmer or fisherman, as defined in I.R.C. §6654(i)(2), your required annual payment is the lesser of:

•66 2/3% of the income tax shown on your 2007 Connecticut income tax return; or

•100% of the income tax shown on your 2006 Connecticut income tax return, if you filed a 2006 income tax return that covered a

Farmers and fishermen are required to make only one installment of estimated income tax for the taxable year. The due date for the installment is on or before January 15 of the following taxable year.

All farmers and fishermen who have checked Box D in Part I must complete and attach this form to their Connecticut income tax return to avoid being billed for interest on the underpayment of estimated income tax. Also check

Name and Identifying Number

Individuals - Enter in the space provided at the top of the form your name and Social Security Number (SSN) as it appears on your Connecticut income tax return. If you filed a joint return, also enter your spouse’s name and SSN.

Trusts and Estates - Enter the name of the trust or estate and the name of the fiduciary as it appears on Form

Part I – Reasons For Filing

If one of the following boxes applies to you, you may be able to reduce or eliminate interest charges that would otherwise accrue if we calculated the interest for you. You must check the box that applies and file this form with your tax return.

Check the boxes that apply. See instructions.

̨A. Your income varied during the year and your interest is reduced or eliminated when computed using the annualized income installment method.

̨B. Your required annual payment is based on the tax shown on your 2006 Connecticut income tax return and you filed or are filing a joint return for either 2006 or 2007, but not for both years.

̨C. Your interest is lower by treating your Connecticut income tax withheld from your income as paid on the dates it was actually withheld instead of in equal amounts on the payment due dates.

̨D. You are a farmer or fisherman as defined in I.R.C. §6654(i)(2).

̨E. You cannot use the prior year’s tax liability as a basis for your required annual payment.

If you checked any of these boxes, also be sure to check the box for Form

Part II – Required Annual Payment

Complete Part II to determine if you were required to make estimated payments. See Instructions.

1. |

2007 Connecticut income tax |

1. |

_________________________________ |

2. |

Multiply Line 1 by 90% (.90). Farmers and fishermen, see instructions |

2. |

_________________________________ |

3. |

Connecticut income tax withheld |

3. |

_________________________________ |

4.Subtract Line 3 from Line 1. If the result is less than $1,000, stop here. Do not

complete or file this form |

4. |

_________________________________ |

5. Enter your 2006 Connecticut income tax. See instructions |

5. |

_________________________________ |

6.Enter the smaller of Line 2 or Line 5. This is your required annual payment

for 2007 |

6. _________________________________ |

7.Subtract Line 3 from Line 6. If the result is zero or less, stop here. Do not

complete or file this form |

7. _________________________________ |

Part III – Calculate Your Underpayment and Interest for Each Calendar Quarter See instructions.

|

|

|

|

A |

B |

C |

|

D |

|

TOTAL |

|

|

|

|

|

|

|

|

|

||

8. |

Enter the required annual payment, Part II, Line 6. Enter |

|

|

|

|

|

|

|

||

|

the same amount in Columns A, B, C, and D. If you |

|

|

|

|

|

|

|

||

|

checked Part I, Box A, or Box D, see instructions. |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

9. |

Installment percentages |

|

|

.25 |

.50 |

.75 |

|

1.00 |

234567890123Page of46 |

|

|

|

|

|

|

|

|

||||

10. |

Multiply Line 8 by Line 9. Enter each result in the |

|

|

|

|

|

||||

|

appropriate column. If you checked Part I, Box A, see |

|

|

|

|

|

||||

|

instructions. |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||||

11. |

Enter the total Connecticut tax withheld, Part II, Line 3. |

|

|

|

|

|

||||

|

Enter the same amount in Columns A, B, C, and D. |

|

|

|

|

|

||||

|

If you checked Part I, Box C, skip this line and see |

|

|

|

|

|

||||

|

instructions for Line 13. |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

12. |

Withholding percentages |

|

|

.25 |

.50 |

.75 |

|

1.00 |

||

|

|

|

|

|

||||||

|

|

|

|

|

|

|

||||

13. |

Multiply Line 11 by Line 12. Enter each result in the |

|

|

|

|

|

||||

|

appropriate column. If you checked Part 1, Box C, see |

|

|

|

|

|

||||

|

instructions. |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||||

14. |

Subtract Line 13 from Line 10. Enter each result in the |

|

|

|

|

|

||||

|

appropriate column. If Line 13 is equal to or greater than |

|

|

|

|

|

||||

|

Line 10 in any column, enter “0” in that column. |

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

15. |

Enter the estimated tax payments. See instructions. |

|

|

|

|

|

||||

|

|

|

|

|

|

|

||||

16. |

Underpayments - Subtract Line 15 from Line 14. Enter |

this worksheet |

for your |

records. |

|

|

||||

Form |

Attach |

Keep a copy of |

|

|

||||||

|

each result in the appropriate column. If Line 15 is equal |

|

|

|

|

|

|

|

||

|

to or greater than Line 14 in any column, enter “0” in that |

|

|

|

|

|

|

|

||

|

column. |

|

|

|

|

|

|

|

|

|

17. |

Interest - Use Worksheets A, B, C, and D of Schedule B |

|

|

|

|

|

|

|

||

|

and enter each result in the appropriate column. Add |

|

|

|

|

|

|

|

||

|

Columns A, B, C, and D. Enter the total in the Total |

|

|

|

|

|

|

|

||

|

Column and on the appropriate line of your Connecticut |

|

|

|

|

|

|

|

||

|

income tax return. |

|

|

|

|

|

|

|

|

|

|

|

|

this form to the back of your Connecticut income tax return. |

|

|

|

||||

Schedule A

Annualized Income Installment Schedule

|

|

|

(a) |

(b) |

(c) |

(d) |

|

|

|

|

|

|

|

Trusts and estates should not use the period ending |

|

|||||

dates shown to the right. Instead, use |

|

to |

to |

to |

to |

|

|

||||||

|

|

|

|

|

|

|

1. |

Enter your Connecticut adjusted gross income for each |

|

|

|

|

|

|

period. See instructions. |

1 |

|

|

|

|

|

|

|

|

|

|

|

2. |

Annualization amounts: Trusts and estates, see instructions. |

2 |

4 |

2.4 |

1.5 |

1 |

|

|

|

|

|

|

|

3. |

Annualized income: Multiply Line 1 by Line 2. |

3 |

|

|

|

|

|

|

|

|

|

|

|

4. |

Enter the tax for the amount on Line 3. See instructions. |

4 |

|

|

|

|

|

|

|

|

|

|

|

5. |

Credit for income taxes paid to qualifying jurisdictions: |

|

|

|

|

|

|

Residents and |

5 |

|

|

|

|

6. |

Subtract Line 5 from Line 4. |

6 |

|

|

|

|

|

|

|

|

|

|

|

7. |

Connecticut alternative minimum tax: See instructions. |

7 |

|

|

|

|

|

|

|

|

|

|

|

8. |

Add Line 6 and Line 7. |

8 |

|

|

|

|

|

|

|

|

|

|

|

9. |

Credit for property taxes paid on your primary residence |

|

|

|

|

|

|

or motor vehicle, or both: Residents only, see instructions. |

9 |

|

|

|

|

|

|

|

|

|

|

|

10. Subtract Line 9 from Line 8. If less than zero, enter “0.” |

10 |

|

|

|

|

|

|

|

|

|

|

|

|

11. |

Adjusted net Connecticut minimum tax credit: |

|

|

|

|

|

|

See instructions. |

11 |

|

|

|

|

|

|

|

|

|

|

|

12. Subtract Line 11 from Line 10. |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

13. Applicable percentages |

13 |

0.225 |

0.45 |

0.675 |

0.90 |

|

|

|

|

|

|

|

|

14. Multiply Line 12 by Line 13. |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Complete Lines 15 - 25 in one column before going to the next column. |

|

||||

|

|

|

|

|

|

|

15. Add the amounts in all preceding columns of Line 21. |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

16. Annualized income installment. Subtract Line 15 from |

|

|

|

|

|

|

|

Line 14. If zero or less, enter “0.” |

16 |

|

|

|

|

|

|

|

|

|

|

|

17. Enter 25% (.25) of your required annual payment from |

|

|

|

|

|

|

|

Form |

17 |

|

|

|

|

|

|

|

|

|

|

|

18. Enter amount from Line 20 of the preceding column of |

|

|

|

|

|

|

|

this schedule. |

18 |

|

|

|

|

|

|

|

|

|

|

|

19. Add Line 17 and Line 18 and enter the total. |

19 |

|

|

|

|

|

|

|

|

|

|

|

|

20. If Line 19 is more than Line 16, subtract Line 16 from |

|

|

|

|

|

|

|

Line 19; otherwise enter “0.” |

20 |

|

|

|

|

|

|

|

|

|

|

|

21. Enter the smaller of Line 16 or Line 19. |

21 |

|

|

|

|

|

|

|

|

|

|

|

|

22. Enter the amount from Line 21, Column (a) here and on |

|

|

|

|

|

|

|

Form |

22 |

|

|

|

|

23. Add Line 21, Column (b) and Line 22, Column (a). Enter |

|

|

|

|

|

|

|

here and on Form |

23 |

|

|

|

|

|

|

|

|

|

|

|

24. Add Line 21, Column (c) and Line 23, Column (b). Enter |

|

|

|

|

|

|

|

here and on Form |

24 |

|

|

|

|

|

|

|

|

|

|

|

25. Add Line 21, Column (d) and Line 24, Column (c). Enter |

|

|

|

|

|

|

|

here and on Form |

25 |

|

|

|

|

|

|

|

|

|

|

|

If you completed this schedule, attach it to Form

Form |

2345678901234 |

Page 3 of 6 |

Schedule B

Interest Calculation

Worksheet A — For period beginning after April 15, 2007, and ending on or before June 15, 2007. |

|

|||||

|

Date |

Amount |

Interest |

Interest |

||

|

Rate |

|||||

|

|

1 |

2 |

3 |

|

4 |

|

|

|

|

|

|

|

Line a - Underpayment |

|

|

|

.01 |

|

|

|

|

|

|

|

|

|

Line b - Late payment |

|

|

|

|

||

|

|

|

|

|

|

|

Line c - Revised underpayment |

|

|

|

.01 |

|

|

|

|

|

|

|

|

|

Line d - Late payment |

to |

|

|

|

|

|

|

|

|

|

|

|

|

Line e - Total interest |

|

|

|

|

|

|

|

|

|

|

|

||

Worksheet B — For period beginning after June |

5, 2007, and ending on or before September 15, 2007. |

|||||

|

|

|

2 |

|

|

4 |

|

|

|

|

|

|

|

Line a - Underpayment |

|

|

|

.01 |

|

|

|

|

|

|

|

|

|

Line b - Late payment |

to |

|

|

|

|

|

|

|

|

|

|

|

|

Line c - Revised underpayment |

|

|

|

.01 |

|

|

|

|

|

|

|

|

|

Line d - Late payment |

to |

|

|

|

|

|

|

|

|

|

|

|

|

Line e - Revised underpayment |

|

|

|

.01 |

|

|

|

|

|

|

|

|

|

Line f - Late payment |

to |

|

|

|

|

|

|

|

|

|

|

|

|

Line g - Total interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Worksheet C — For period beginning after September 15, 2007, and ending on or before January 15, 2008.

|

|

2 |

|

|

4 |

|

|

|

|

|

|

Line a - Underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line b - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line c - Revised underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line d - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line e - Revised underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line f - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line g - Revised underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line h - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line i - Total interest |

|

|

|

|

|

|

|

|

|

|

|

Worksheet D — For period beginning after January 1 , 2008, and ending on or before April 15, 2008. |

|

||||

|

|

2 |

|

|

4 |

|

|

|

|

|

|

Line a - Underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line b - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line c - Revised underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line d - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line e - Revised underpayment |

|

|

.01 |

|

|

|

|

|

|

|

|

Line f - Late payment |

|

|

|

|

|

|

|

|

|

|

|

Line g - Total interest |

|

|

|

|

|

|

|

|

|

|

|

|

Keep a copy of this schedule for your records. |

|

|||

Form |

Page of 6 |

Form

Any reference in this document to a spouse also refers to a party to a civil union recognized under Connecticut law.

Part I - Reasons for Filing

Complete Part I only if one of the following boxes applies to you. By checking the box that applies to you, you may be able to reduce or eliminate interest charges that would otherwise accrue if we calculated the interest for you under the normal requirements for making estimated tax payments. If you checked any of the boxes in Part I, also be sure to check the box for Form

Box A - Check this box if you are using the annualized income installment method. If your income fluctuated during the year, this method may reduce or eliminate the amount of one or more required quarterly payments. See instructions for Schedule A.

Box B - Check this box if your estimated tax payments were based on the tax shown on your 2006 Connecticut income tax return and your filing status changed from last year. See Changes in Filing Status in Part II, Line 5, below.

Box C - Check this box if you want income tax withheld in 2007 to be applied when it was actually withheld rather than in four equal installments. See instructions for Part III, Line 11 and Line 13.

Box D - Check this box if you are a farmer or fisherman and:

•You are required to make only one installment of estimated Connecticut income tax; or

•You have filed your tax return for the taxable year on or before March 1, 2008, and have paid the amount computed on the return as payable for the taxable year.

If you have filed your return for the taxable year and paid the amount computed as payable on or before March 1, 2008, and therefore are not required to make an estimated income tax payment, you must check Form

If you are required to make an estimated income tax payment, it is due on or before January 15, 2008. The installment is the lesser of 66 2/3% of the income tax shown on your 2007 Connecticut income tax return or 100% of the income tax shown on your 2006 Connecticut income tax return. See the instructions for Part III, Line 8.

Box E - Check this box if you cannot use your 2006 Connecticut income tax as a basis for your required annual payment.

You may only use your 2006 Connecticut income tax if:

•You filed a 2006 Connecticut income tax return that covered a

•During the 2006 taxable year, you were a resident,

If you do not meet one of the above conditions, your required annual payment must be 90% of the income tax shown on your 2007 Connecticut income tax return.

Part II - Required Annual Payment

Line 1: Enter the amount of income tax shown on your 2007 Connecticut income tax return (Form

Line 2: Farmers and fishermen multiply Line 1 by 66 2/3% (.6667).

Line 3: Enter Connecticut income tax withheld in 2007. Do not enter any estimated tax payments or taxes withheld for the IRS or other jurisdictions.

Line 5: If your filing status was the same on your 2006 and 2007 Connecticut income tax returns and your 2006 Connecticut income tax return covered a

Enter “0” if you did not file a 2006 Connecticut income tax return because you did not have a Connecticut income tax liability and you were a resident, nonresident, or

If you were a nonresident or

Changes in Filing Status From 2006 to 2007: If you are filing a joint Connecticut return for 2007 but filed separate Connecticut returns for 2006 as single, married filing separately, or head of household, you must combine your 2006 separate tax liabilities to determine your combined 2006 income tax. If either you or your spouse did not file a 2006 Connecticut income tax return, see the instructions for Part I, Box E, to determine if you can use the prior year’s tax as the basis for your required annual payment.

If you are filing separate Connecticut returns for 2007 but filed a joint Connecticut return for 2006, you must determine your share of the 2006 tax (Form

Your separate 2006 tax liability

Both spouses’ separate 2006 tax liabilities x Your 2006 joint tax liability

Part III - Calculate Your Underpayment and Interest

Line 8: If you are using the annualized income installment method, skip Line 8 and Line 9 and go on to Line 10. Be sure you also check Part I, Box A.

If you checked Part I, Box D, because you are a farmer or fisherman and you have made only one installment of estimated income tax, complete Column D only.

Line 10: If you checked Part I, Box A, because you are using the annualized income installment method, enter the amounts from Schedule A, Lines 22 through 25, in the appropriate columns. Attach Schedule A to Form

Line 11: Enter the total amount of Connecticut income tax withheld in 2007 in Columns A, B, C, and D. Do not enter estimated tax payments or taxes withheld for the Internal Revenue Service (IRS) or other jurisdictions.

Example: If your total 2007 Connecticut income tax withheld was $1,300, enter $1,300 in Columns A, B, C, and D.

If you want Connecticut income tax withholding to apply when it was actually withheld, skip Line 11 and Line 12 and go on to Line 13. Be sure you also check Part I, Box C.

Line 13: If you want Connecticut income tax withholding to apply when it was actually withheld, enter the actual cumulative withholding amounts on Line 13.

Example: If $600 was withheld in March, $200 in May, $200 in August, and $300 in November, enter $600 in Column A, $800 in Column B, $1,000 in Column C, and $1,300 in Column D.

Line 15: Enter in the appropriate columns all timely installment payments you made. Timely installment payments are all payments (other than any tax withheld) made on or before the due date including any previous installment payments.

Form |

Page 5 of 6 |

Example: If estimated Connecticut income tax payments of $100 each were made on April 15, 2007, June 15, 2007, September 15, 2007, and January 15, 2008, enter $100 in Column A, $200 in Column B, $300 in Column C, and $400 in Column D.

Schedule A

Annualized Income Installment General Instructions

You may benefit from using the annualized income installment method if your income varied throughout the year because you earned more money later in the year than you did in the early part of the year, such as from lottery winnings, investment income, or

By using this method, you may be able to reduce or eliminate the amount of one or more required installments.

For information on filing estimated tax payments using the annualized income installment method, see Informational Publication 2006(25), A Guide to Calculating Your Annualized Estimated Income Tax Installments and Worksheet

If you use the annualized income installment method for any installment due date, you must use this method for all installment due dates. Form

If you use the annualized income installment method, you are required to complete all of the following steps:

1. Check BoxAon Form

2Enter the amounts from Schedule A, Lines 22 through 25 in the appropriate columns on Form

3.Attach Form

4.Attach your calculations of your Connecticut adjusted gross income for each period; and

5.Check the box for Form

Line Instructions

Line 1: Attach a schedule showing how you computed your Connecticut adjusted gross income for each period.

Trusts and estates must enter their Connecticut taxable income and use the following period ending dates:

Line 2: Trusts and estates do not use the amounts shown in Columns (a) through (d). Instead, use 6, 3, 1.71429, and 1.09091, as the annualization amounts.

Line 4: Resident individuals must compute the tax on the amount shown on Line 3 using the Tax Tables or the Tax Calculation Schedule. Resident trusts and estates must multiply Line 3 by 5% (.05).

Nonresidents and

a. Annualized income from Line 3 of this schedule |

|

b. Annualized Connecticut source income |

|

c. Enter the greater of Line a or Line b. |

|

d. Enter the tax due on Line c using the Tax Tables or the |

|

Tax Calculation Schedule. |

|

Trusts and estates: Multiply Line c by 5% (.05). |

|

e. Divide Connecticut source income for the period by |

|

Connecticut adjusted gross income (Connecticuttaxable |

|

income for trusts and estates) for the period. This is your |

|

allocated Connecticut income tax percentage. If Line b |

|

is greater than Line a, enter 1.0000. |

• |

f. Multiply Line d by Line e. |

|

Enter here and on Schedule A, Line 4. |

|

Line 5: The credit for tax paid to a qualifying jurisdiction is based wholly or partly on the annualized income for each period.

Line 7: You must annualize your adjusted federal alternative minimum taxable income using the annualization amounts on Line 2. Use Form

Line 9: Resident Individuals - Enter the credit for property taxes paid on your primary residence, motor vehicle, or both, as calculated on your 2007 Form

The credit may not exceed $500 and may be further reduced. Refer to Form

Line 11: The adjusted net Connecticut minimum tax credit is based wholly or partly on the annualized income for each period.

Lines 15 through 25: You must complete Lines 15 through 25 in one column before continuing to the next column.

Schedule B

Interest Calculation

General Instructions

Complete a separate worksheet for each underpayment shown on Form

Example: If the underpayment is shown in Part III, Line 16, Column A, complete Worksheet A. If no underpayment is shown in Part III, Line 16, Column B, but an underpayment is shown in Part III, Line 16, Column C, skip Worksheet B and complete Worksheet C.

Interest at 1% per month or fraction of a month will continue to accrue until the earlier of April 15, 2008, or the date on which the underpayment is paid. A month is measured from the sixteenth day of the first month to the fifteenth day of the next month. Any fraction of a month is considered a whole month.

Line Instructions

Before calculating your interest, list all estimated payments and Connecticut tax withholding for 2007 on a separate sheet of paper. For Connecticut income tax withheld, you are considered to have paid 25% of this amount on each payment due date (4/15, 6/15, 9/15, and 1/15) unless you can show otherwise.

Worksheet A

Line a: Enter in Column 2 the underpayment shown on Form

Multiply Column 2 by Column 3 and enter the result in Column 4.

Line b: Enter in Column 2 the amount paid during the period listed in Column 1. If multiple payments were made during the period listed, combine those payments and enter the total.

Line c: Subtract Line b from Line a in Column 2. Enter the result on Line c, Column 2. Multiply Column 2 by Column 3 and enter the result in Column 4.

Line d: Follow the instructions for Line b above.

Line e: Add all amounts in Column 4. Enter the total on Form

Worksheets B and D

Lines a through d: Follow the instructions for these lines on Worksheet A above.

Line e: Subtract Line d from Line c in Column 2. Enter the result on Line e, Column 2. Multiply Column 2 by Column 3 and enter the result in Column 4.

Line f: Enter in Column 2 the amount paid during the period listed in Column 1. If multiple payments were made during the period listed, combine those payments and enter the total.

Line g: Add all amounts in Column 4. Enter the total on Form

Worksheet C

Lines a through f: Follow the instructions for these lines on Worksheets B and D above.

Line g: Subtract Line f from Line e in Column 2. Enter the result on Line g, Column 2. Multiply Column 2 by Column 3 and enter the result in Column 4.

Line h: Enter in Column 2 the amount paid during the period listed in Column 1. If multiple payments were made during the period listed, combine those payments and enter the total.

Form |

Page 6 of 6 |

|