The FT 1014 form is a IRS form used to report certain financial transactions. This form is used for both individual and business taxpayers and can be filed electronically or by mail. The FT 1014 form is due April 15th of the following year, and must be filed even if you do not owe any taxes. There are a number of transactions that must be reported on the FT 1014 form, so make sure you are aware of what needs to be included. If you have any questions about the FT 1014 form, speak with an accountant or tax specialist for assistance.

| Question | Answer |

|---|---|

| Form Name | Ft 1014 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | USC, nonresidential, 1817, gallonage |

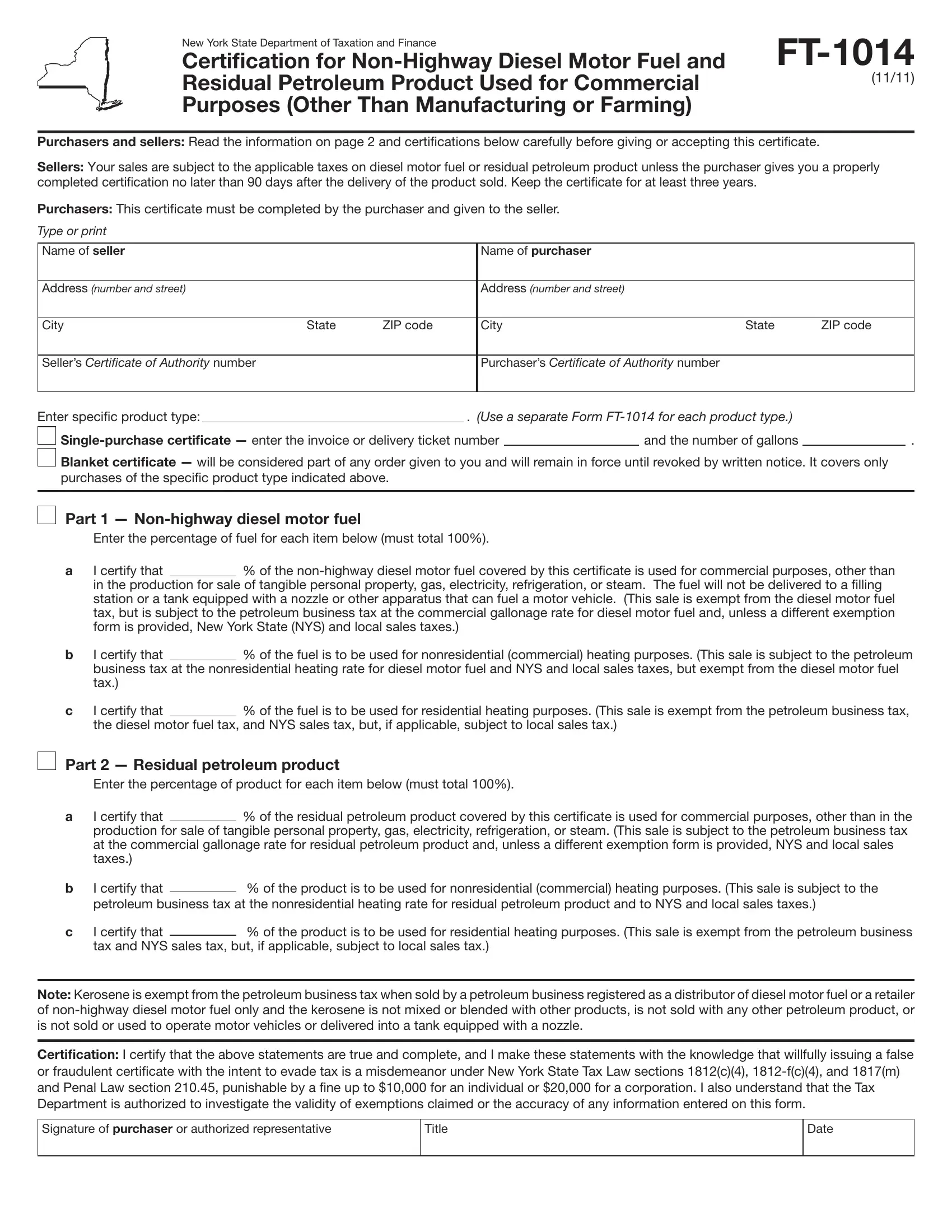

New York State Department of Taxation and Finance

Certification for

(11/11)

Purchasers and sellers: Read the information on page 2 and certiications below carefully before giving or accepting this certiicate.

Sellers: Your sales are subject to the applicable taxes on diesel motor fuel or residual petroleum product unless the purchaser gives you a properly completed certiication no later than 90 days after the delivery of the product sold. Keep the certiicate for at least three years.

Purchasers: This certiicate must be completed by the purchaser and given to the seller.

Type or print

Name of seller |

|

|

Name of purchaser |

|

|

|

|

|

|

|

|

Address (number and street) |

|

|

Address (number and street) |

|

|

|

|

|

|

|

|

City |

State |

ZIP code |

City |

State |

ZIP code |

|

|

|

|

|

|

Seller’s Certificate of Authority number |

|

|

Purchaser’s Certificate of Authority number |

|

|

|

|

|

|

|

|

Enter speciic product type: |

|

. (Use a separate Form |

|

|

||

|

and the number of gallons |

|

. |

|||

Blanket certificate — will be considered part of any order given to you and will remain in force until revoked by written notice. It covers only purchases of the speciic product type indicated above.

Part 1 —

Enter the percentage of fuel for each item below (must total 100%).

a |

I certify that |

|

% of the |

|

in the production for sale of tangible personal property, gas, electricity, refrigeration, or steam. The fuel will not be delivered to a illing |

||

|

station or a tank equipped with a nozzle or other apparatus that can fuel a motor vehicle. (This sale is exempt from the diesel motor fuel |

||

|

tax, but is subject to the petroleum business tax at the commercial gallonage rate for diesel motor fuel and, unless a different exemption |

||

|

form is provided, New York State (NYS) and local sales taxes.) |

||

b |

I certify that |

|

% of the fuel is to be used for nonresidential (commercial) heating purposes. (This sale is subject to the petroleum |

|

business tax at the nonresidential heating rate for diesel motor fuel and NYS and local sales taxes, but exempt from the diesel motor fuel |

||

|

tax.) |

|

|

c |

I certify that |

|

% of the fuel is to be used for residential heating purposes. (This sale is exempt from the petroleum business tax, |

the diesel motor fuel tax, and NYS sales tax, but, if applicable, subject to local sales tax.)

Part 2 — Residual petroleum product

Enter the percentage of product for each item below (must total 100%).

a |

I certify that |

|

% of the residual petroleum product covered by this certiicate is used for commercial purposes, other than in the |

|

|||

|

production for sale of tangible personal property, gas, electricity, refrigeration, or steam. (This sale is subject to the petroleum business tax |

||

|

at the commercial gallonage rate for residual petroleum product and, unless a different exemption form is provided, NYS and local sales |

||

|

taxes.) |

|

|

b |

I certify that |

|

% of the product is to be used for nonresidential (commercial) heating purposes. (This sale is subject to the |

|

|||

|

petroleum business tax at the nonresidential heating rate for residual petroleum product and to NYS and local sales taxes.) |

||

c |

I certify that |

|

% of the product is to be used for residential heating purposes. (This sale is exempt from the petroleum business |

|

|||

|

tax and NYS sales tax, but, if applicable, subject to local sales tax.) |

||

Note: Kerosene is exempt from the petroleum business tax when sold by a petroleum business registered as a distributor of diesel motor fuel or a retailer of

Certification: I certify that the above statements are true and complete, and I make these statements with the knowledge that willfully issuing a false or fraudulent certiicate with the intent to evade tax is a misdemeanor under New York State Tax Law sections 1812(c)(4),

Signature of purchaser or authorized representative

Title

Date

Page 2 of 2

Instructions

General information

This certiicate can be used to claim exemption from the petroleum business tax, diesel motor fuel tax, and NYS sales and use tax on

For farm production, use Form

For manufacturing, use Form

For exempt organizations, use Form

Definitions

Commercial gallonage means gallonage that:

•is

•is included in the full measure of the

•does not and will not qualify:

—for the utility credit or reimbursement,

—as manufacturing gallonage,

—for the

—as fuel used for heating/cooling; and

•will not be used and has not been used in the fuel tank connecting with the engine of a vessel.

Highway diesel motor fuel means any diesel motor fuel which is not

Dyed diesel motor fuel means diesel motor fuel which has been dyed in accordance with and for the purpose of complying with the provisions of 26 USC 4082(a).

Residual petroleum product means the topped crude of reinery operations including No. 5 fuel oil, No. 6 fuel oil, bunker C, and the special grade of diesel product designated as No. 4 diesel fuel, that is not suitable for use in the operation of a motor vehicle engine. This product is sometimes used for the production of electric power, space heating, vessel bunkering, and other industrial purposes.

Need help?

Visit our Web site at www.tax.ny.gov

•get information and manage your taxes online

•check for new online services and features

Telephone assistance |

|

Miscellaneous Tax Information Center: |

(518) |

To order forms and publications: |

(518) |

Text Telephone (TTY) Hotline (for persons with

hearing and speech disabilities using a TTY): (518)

Persons with disabilities: In compliance with the

Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and other facilities are

accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.