Are you planning to file a Tennessee Fae 173 form? Do you want to know the rules and guidelines for filing this document? If so, then this blog post is for you. We’ll provide an overview of the process as well as tips on how best to proceed when it comes to filing your Tennessee Fae 173. Whether it’s understanding what kind of information needs to be entered onto the form or advice on where and when this form should be sent - we’ve got you covered! So read through these brief yet informative points in order to benefit from expert insight into navigating the Tennessee Fae 173 form with ease.

| Question | Answer |

|---|---|

| Form Name | Tennessee Fae 173 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | tn fae 173 instructions, tn 173 instructions, tennessee form fae 173 instructions, tn fae extension |

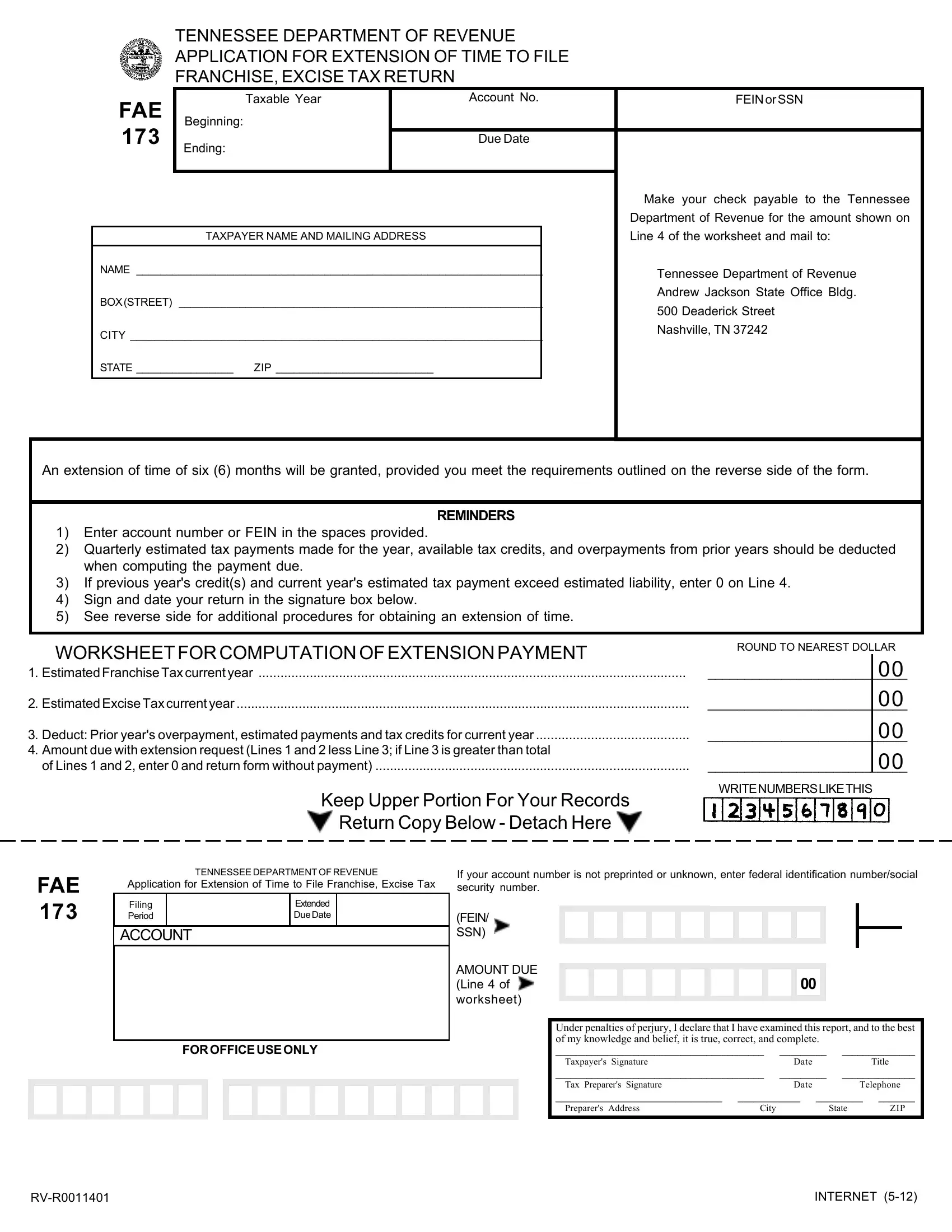

TENNESSEE DEPARTMENT OF REVENUE

APPLICATION FOR EXTENSION OF TIME TO FILE

FRANCHISE, EXCISE TAX RETURN

|

FAE |

Taxable Year |

|

Account No. |

FEINorSSN |

|

|

Beginning: |

|

|

|

|

|

|

173 |

Ending: |

|

Due Date |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Make your check payable to the Tennessee |

|

|

|

|

|

|

|

|

|

|

|

|

|

Department of Revenue for the amount shown on |

|

|

TAXPAYER NAME AND MAILING ADDRESS |

|

|

Line 4 of the worksheet and mail to: |

|

|

|

|

|

|||

|

NAME ___________________________________________________________________ |

|

Tennessee Department of Revenue |

|||

|

|

|

|

|

|

|

|

BOX(STREET) ____________________________________________________________ |

|

Andrew Jackson State Office Bldg. |

|||

|

|

500 Deaderick Street |

||||

|

|

|

|

|

|

|

|

CITY ____________________________________________________________________ |

|

Nashville, TN 37242 |

|||

|

|

|

||||

|

STATE ________________ ZIP __________________________ |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

An extension of time of six (6) months will be granted, provided you meet the requirements outlined on the reverse side of the form.

REMINDERS

1)Enter account number or FEIN in the spaces provided.

2)Quarterly estimated tax payments made for the year, available tax credits, and overpayments from prior years should be deducted when computing the payment due.

3)If previous year's credit(s) and current year's estimated tax payment exceed estimated liability, enter 0 on Line 4.

4)Sign and date your return in the signature box below.

5)See reverse side for additional procedures for obtaining an extension of time.

WORKSHEETFORCOMPUTATIONOFEXTENSIONPAYMENT

1.EstimatedFranchiseTaxcurrentyear .....................................................................................................................

2.EstimatedExciseTaxcurrentyear ............................................................................................................................

3.Deduct: Prior year's overpayment, estimated payments and tax credits for current year ..........................................

4.Amount due with extension request (Lines 1 and 2 less Line 3; if Line 3 is greater than total

of Lines 1 and 2, enter 0 and return form without payment) ......................................................................................

Keep Upper Portion For Your Records

Return Copy Below - Detach Here

ROUND TO NEAREST DOLLAR

00

___________________________00

00

00

WRITENUMBERSLIKETHIS

FAE

173

TENNESSEE DEPARTMENT OF REVENUE

Application for Extension of Time to File Franchise, Excise Tax

Filing |

|

Extended |

|

Period |

|

DueDate |

|

|

|

|

|

ACCOUNT

FOROFFICEUSEONLY

If your account number is not preprinted or unknown, enter federal identification number/social security number.

(FEIN/

SSN)

AMOUNT DUE

(Line 4 of 00 worksheet)

Under penalties of perjury, I declare that I have examined this report, and to the best of my knowledge and belief, it is true, correct, and complete.

________________________________________ |

_________ |

______________ |

|||

Taxpayer's Signature |

|

Date |

|

|

Title |

________________________________________ |

_________ |

______________ |

|||

Tax Preparer's Signature |

|

Date |

|

Telephone |

|

________________________________ |

____________ |

_________ |

_______ |

||

Preparer's Address |

City |

|

|

State |

ZIP |

INTERNET |

PROCEDURES FOR OBTAINING AN EXTENSION OF TIME

NOTE: This form can be filed electronically free of charge at apps.tn.gov/fnetax

1.Required Payment:

•Payments equal to the lesser of 100% of the prior year tax liability or 90% of the current year tax liability must be made by the original due date.

•If the prior tax year covered less than twelve months, the prior period tax must be annualized when calculating the required payment.

•If there was no liability for the prior year, the required payment is $100.

•Quarterly estimated payments, prior year overpayments and any other

2.Extension requests should be made as follows:

•If you are not required to make a payment because you have already made sufficient payments, either the state form or a copy of your federal extension request can be submitted. The form or copy of the federal extension need not be filed on the original due date of the return. Instead, it should be attached to the return itself, which is to be filed on or before the extended due date.

•If a payment is needed to meet the payment requirement and you do not file your federal return as part of a consolidated group, either the state form or a copy of your federal extension request can be submitted. In this case, the form or copy of your federal extension must be filed with the extension payment on or before the original due date of the return.

•If a payment is required and you file your federal return as part of a consolidated group, you must use this form or file an extension request electronically. This form or the electronic version of this form must be filed with the extension payment on or before the original due date of the return.

3.Other important information:

•Penalty will be computed as though no extension had been granted if, (1) the amount paid on or before the original due date does not satisfy the payment requirement indicated above, or (2) the return is not filed by the extended due date.

•An approved extension does not affect interest. Interest will be computed on any unpaid tax from the original due date of the return until the date the tax is paid.