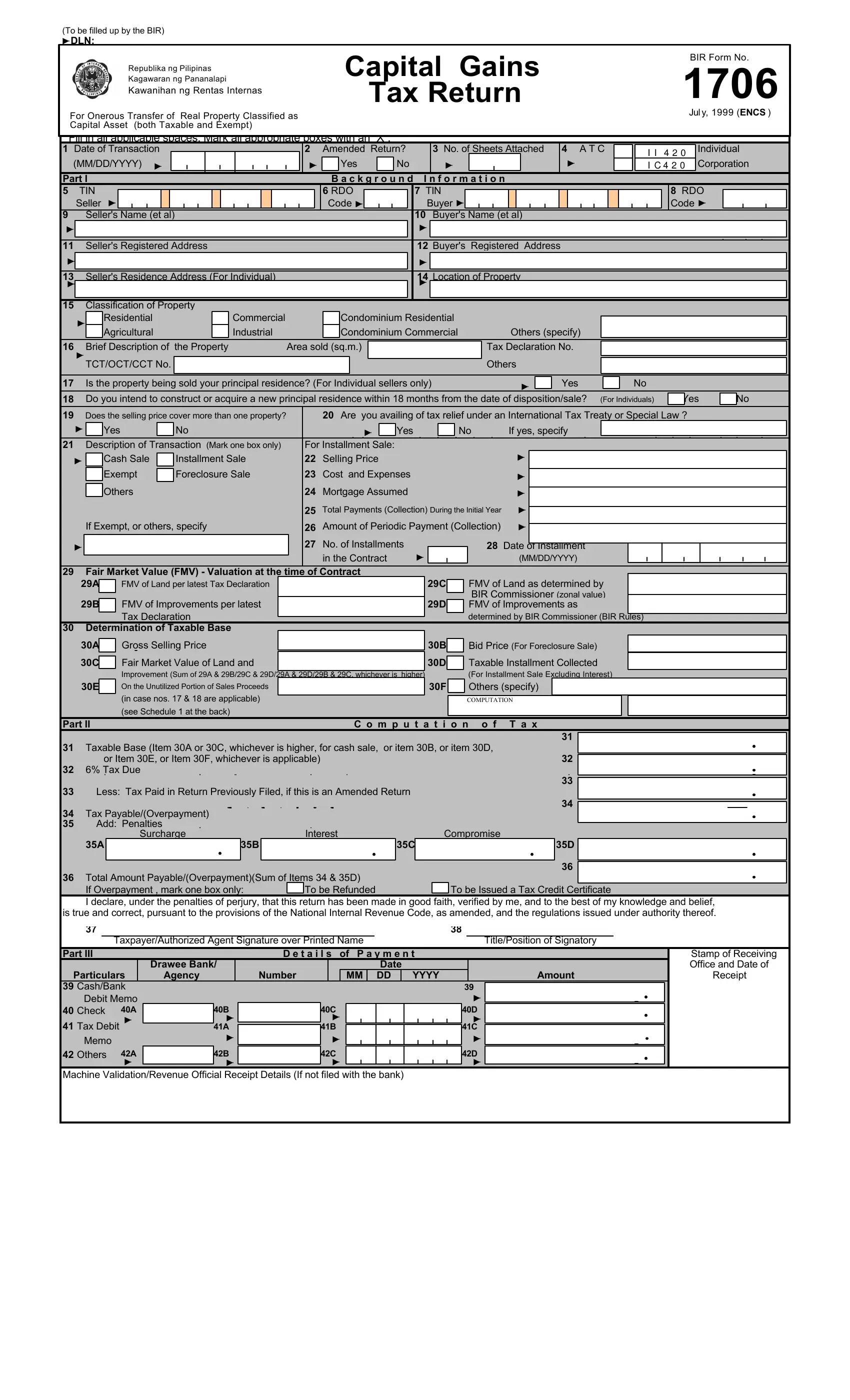

BIR Form 1706 is the Capital Gains Tax Return for the Philippines. It covers the onerous transfer of real property classified as a capital asset, including cash sales, installment sales, and foreclosure sales. Both individual taxpayers and corporations must file this form whenever they sell, exchange, or otherwise dispose of real property not used in business operations.

You must file the 1706 Form when you complete any of the following transactions involving real property in the Philippines:

The taxable base for the 1706 Form is the higher of the gross selling price or the fair market value of the property. Capital gains tax is fixed at 6% of the computed taxable base. The form requires a complete description of the transaction, including the date, seller and buyer information, and full property details.

Taxpayers must file BIR Form 1706 at the Revenue District Office that has jurisdiction over the property location. The filing deadline is 30 days from the date the deed of sale is notarized. Taxpayers who reinvest the proceeds from the sale of a principal residence into a new principal residence within 18 months may qualify for a capital gains tax exemption.

After filing the 1706 Form, you may also need the BIR Form 2000-OT for documentary stamp tax on the same transaction. For payment of other BIR taxes and fees, use BIR Form 0605. For annual income tax obligations as an individual, see BIR Form 1701.

| Question | Answer |

|---|---|

| Form Name | 1706 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 1706 bir form 2018, 1706 bir form, bir form 1706 january 2018 encs, bir form 1706 |