Navigating the complexities of managing capital losses can often seem daunting to both seasoned investors and novices alike. Central to this process is the Capital Loss Carryover Worksheet, a crucial tool for individuals looking to carry over losses from one tax year to another. This form becomes relevant when taxpayers find themselves in a position where their capital losses exceed their capital gains, allowing them to apply these losses in future tax years. Its significance lies in the intricate details required for accurately reporting the sales price of assets, whether they be stocks, bonds, or other securities, with special consideration given to the amount reported on Form 1099-B or its equivalent. Moreover, the worksheet guides users through calculating the cost or other basis of sold assets, a process further complicated by numerous factors such as depreciation, inheritance, or receiving the property as a gift. Adjustments to the basis are necessary in several unique scenarios, including transactions involving nondividend distributions before a sale, stock splits, or properties acquired through various means that may not allow the use of the actual cost as the basis. Importantly, the worksheet aids in determining the amount of loss that can be carried over to future years, a calculation that hinges on the specifics of the taxpayer’s financial situation, including their losses and income for the reporting year. Understanding the Capital Loss Carryover Worksheet in its entirety not only provides taxpayers with the opportunity to make the most of their capital losses but also ensures compliance with the intricate regulations overseeing capital gains and losses.

| Question | Answer |

|---|---|

| Form Name | Capital Loss Carryover Worksheet Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | capital loss carryover worksheet 2020, 2020 capital loss carryover worksheet, irs capital loss carryover worksheet, capital carryover worksheet |

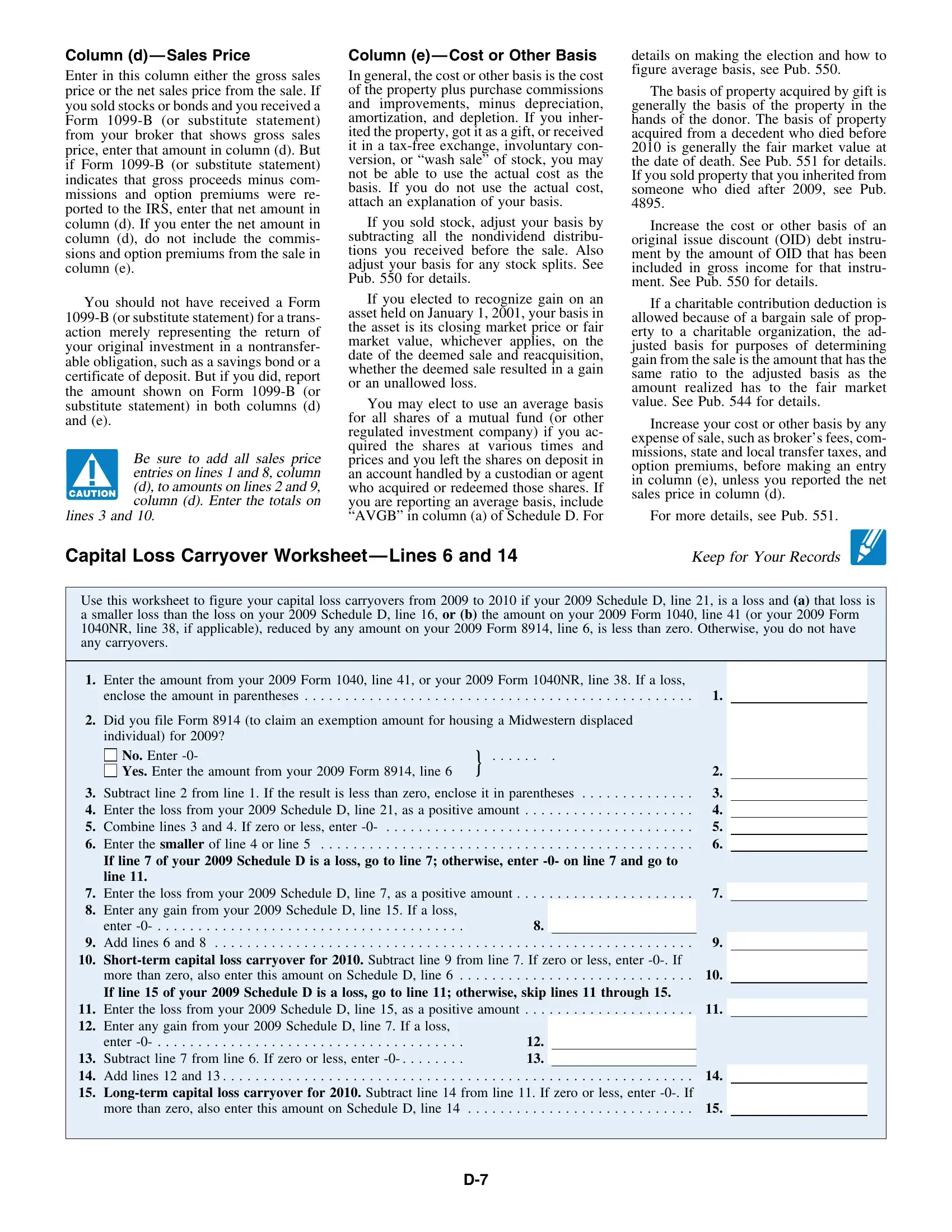

Column (d) — Sales Price

Enter in this column either the gross sales price or the net sales price from the sale. If you sold stocks or bonds and you received a Form

You should not have received a Form

Be sure to add all sales price entries on lines 1 and 8, column (d), to amounts on lines 2 and 9, column (d). Enter the totals on

lines 3 and 10.

Column (e) — Cost or Other Basis

In general, the cost or other basis is the cost of the property plus purchase commissions and improvements, minus depreciation, amortization, and depletion. If you inher- ited the property, got it as a gift, or received it in a

If you sold stock, adjust your basis by subtracting all the nondividend distribu- tions you received before the sale. Also adjust your basis for any stock splits. See Pub. 550 for details.

If you elected to recognize gain on an asset held on January 1, 2001, your basis in the asset is its closing market price or fair market value, whichever applies, on the date of the deemed sale and reacquisition, whether the deemed sale resulted in a gain or an unallowed loss.

You may elect to use an average basis for all shares of a mutual fund (or other regulated investment company) if you ac- quired the shares at various times and prices and you left the shares on deposit in an account handled by a custodian or agent who acquired or redeemed those shares. If you are reporting an average basis, include “AVGB” in column (a) of Schedule D. For

details on making the election and how to figure average basis, see Pub. 550.

The basis of property acquired by gift is generally the basis of the property in the hands of the donor. The basis of property acquired from a decedent who died before 2010 is generally the fair market value at the date of death. See Pub. 551 for details. If you sold property that you inherited from someone who died after 2009, see Pub. 4895.

Increase the cost or other basis of an original issue discount (OID) debt instru- ment by the amount of OID that has been included in gross income for that instru- ment. See Pub. 550 for details.

If a charitable contribution deduction is allowed because of a bargain sale of prop- erty to a charitable organization, the ad- justed basis for purposes of determining gain from the sale is the amount that has the same ratio to the adjusted basis as the amount realized has to the fair market value. See Pub. 544 for details.

Increase your cost or other basis by any expense of sale, such as broker’s fees, com- missions, state and local transfer taxes, and option premiums, before making an entry in column (e), unless you reported the net sales price in column (d).

For more details, see Pub. 551.

Capital Loss Carryover Worksheet — Lines 6 and 14 |

Keep for Your Records |

Use this worksheet to figure your capital loss carryovers from 2009 to 2010 if your 2009 Schedule D, line 21, is a loss and (a) that loss is a smaller loss than the loss on your 2009 Schedule D, line 16, or (b) the amount on your 2009 Form 1040, line 41 (or your 2009 Form 1040NR, line 38, if applicable), reduced by any amount on your 2009 Form 8914, line 6, is less than zero. Otherwise, you do not have any carryovers.

1.Enter the amount from your 2009 Form 1040, line 41, or your 2009 Form 1040NR, line 38. If a loss,

enclose the amount in parentheses |

1. |

2.Did you file Form 8914 (to claim an exemption amount for housing a Midwestern displaced individual) for 2009?

|

|

No. Enter |

} |

. |

|

|

|

|

|

|

|

|

|

|

|||

|

|

Yes. Enter the amount from your 2009 Form 8914, line 6 |

|

2. |

|

|

|

|

3. |

. . . . . . . . . . . . . .Subtract line 2 from line 1. If the result is less than zero, enclose it in parentheses |

3. |

|

|

|

|||

4. |

. . .Enter the loss from your 2009 Schedule D, line 21, as a positive amount |

. . . . . . . . . . . . . . . . . . |

4. |

|

|

|

||

5. |

. . . . . . . . . . .Combine lines 3 and 4. If zero or less, enter |

. . . . . . . . . |

. . . . . . . . . . . . . . . . . . |

5. |

|

|

|

|

6. |

. . . . . . . . . . . . . . . . . . .Enter the smaller of line 4 or line 5 |

. . . . . . . . . |

. . . . . . . . . . . . . . . . . . |

6. |

|

|

|

|

|

If line 7 of your 2009 Schedule D is a loss, go to line 7; otherwise, enter |

|

|

|

|

|||

|

line 11. |

|

|

|

|

|

|

|

7. |

. . . .Enter the loss from your 2009 Schedule D, line 7, as a positive amount |

. . . . . . . . . . . . . . . . . . |

7. |

|

|

|

||

|

|

|

|

|

|

|

|

|

8.Enter any gain from your 2009 Schedule D, line 15. If a loss,

|

enter |

8. |

|

|

9. |

Add lines 6 and 8 |

. . .9 |

||

10.

more than zero, also enter this amount on Schedule D, line 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10.

If line 15 of your 2009 Schedule D is a loss, go to line 11; otherwise, skip lines 11 through 15.

11. |

Enter the loss from your 2009 Schedule D, line 15, as a positive amount |

11. |

|

12. |

Enter any gain from your 2009 Schedule D, line 7. If a loss, |

|

|

|

enter |

12. |

|

13. |

Subtract line 7 from line 6. If zero or less, enter |

13. |

|

14. |

Add lines 12 and 13 |

14. |

|

15. |

|

||

|

more than zero, also enter this amount on Schedule D, line 14 |

15. |

|

|

|

|

|