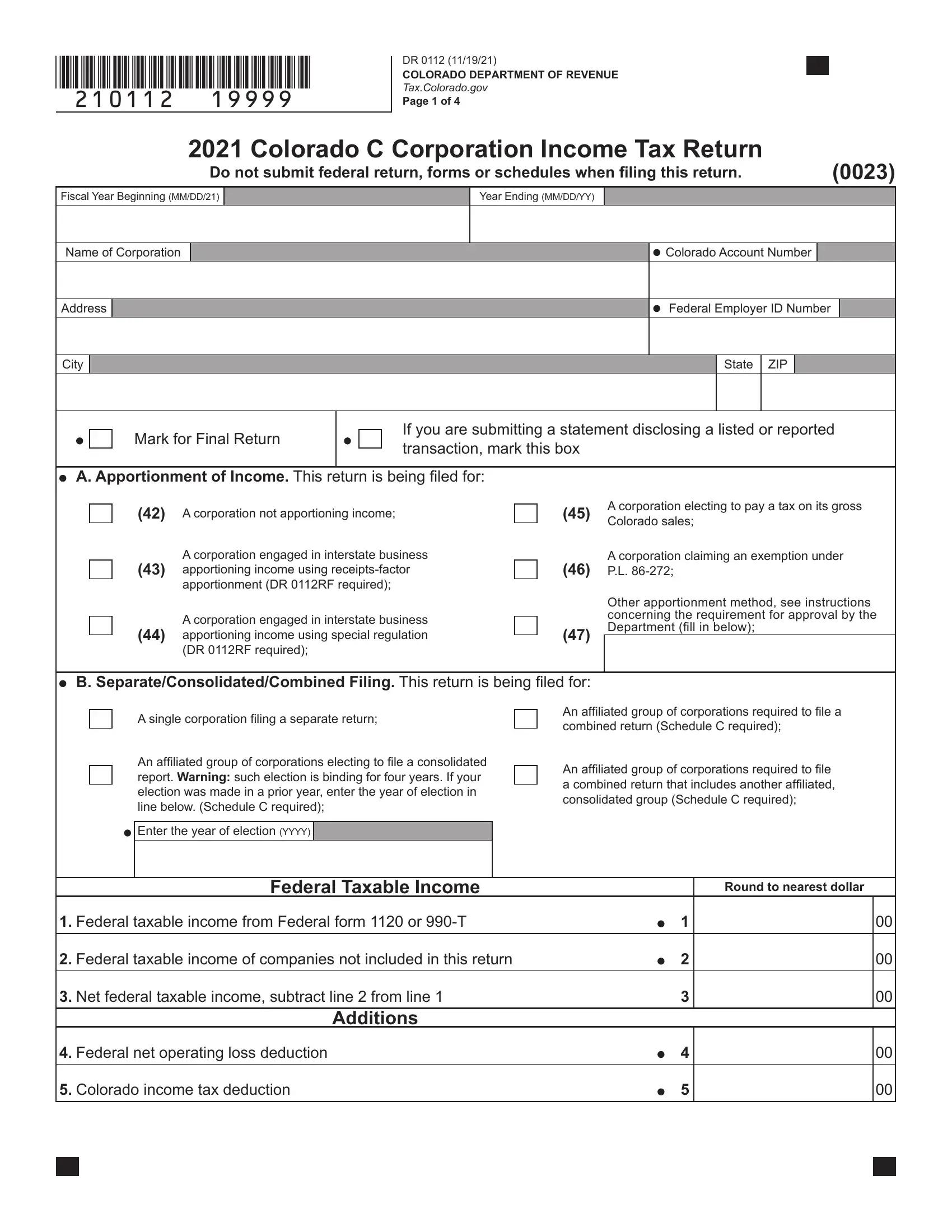

The DR 0112 filing kit is the essential resource for C corporations submitting an annual state income tax return to the Department of Revenue. This comprehensive packet covers the DR 0112 C Corporation Income Tax Return along with all related schedules: the DR 0158-C for extending the filing deadline, the DR 0900C for corporation tax payment, the DR 0112RF for the Receipts Factor Apportionment schedule, Schedule C for corporation affiliations, and the DR 0112CR for applicable corporation credits. The packet specifies separate mailing addresses for return submissions with and without payment, so each corporation knows exactly where to send its documents. It also outlines electronic filing options through the Revenue Online portal, which accepts the DR 0112 return and provides immediate confirmation while reducing errors. C corporations on a calendar year must file their return by April 15, with an automatic extension to October 15 for those needing more time. Starting from the federal taxable income reported on IRS Form 1120, the DR 0112 applies state-level adjustments to arrive at the correct amount owed. For all related state tax forms, see the Colorado Tax Form collection at FormsPal.

| Question | Answer |

|---|---|

| Form Name | Colorado Form 112 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | how to 112 tax form colorado, 2020 112 form co, how colorado form 112 instructions, colorado form dr 0112 |