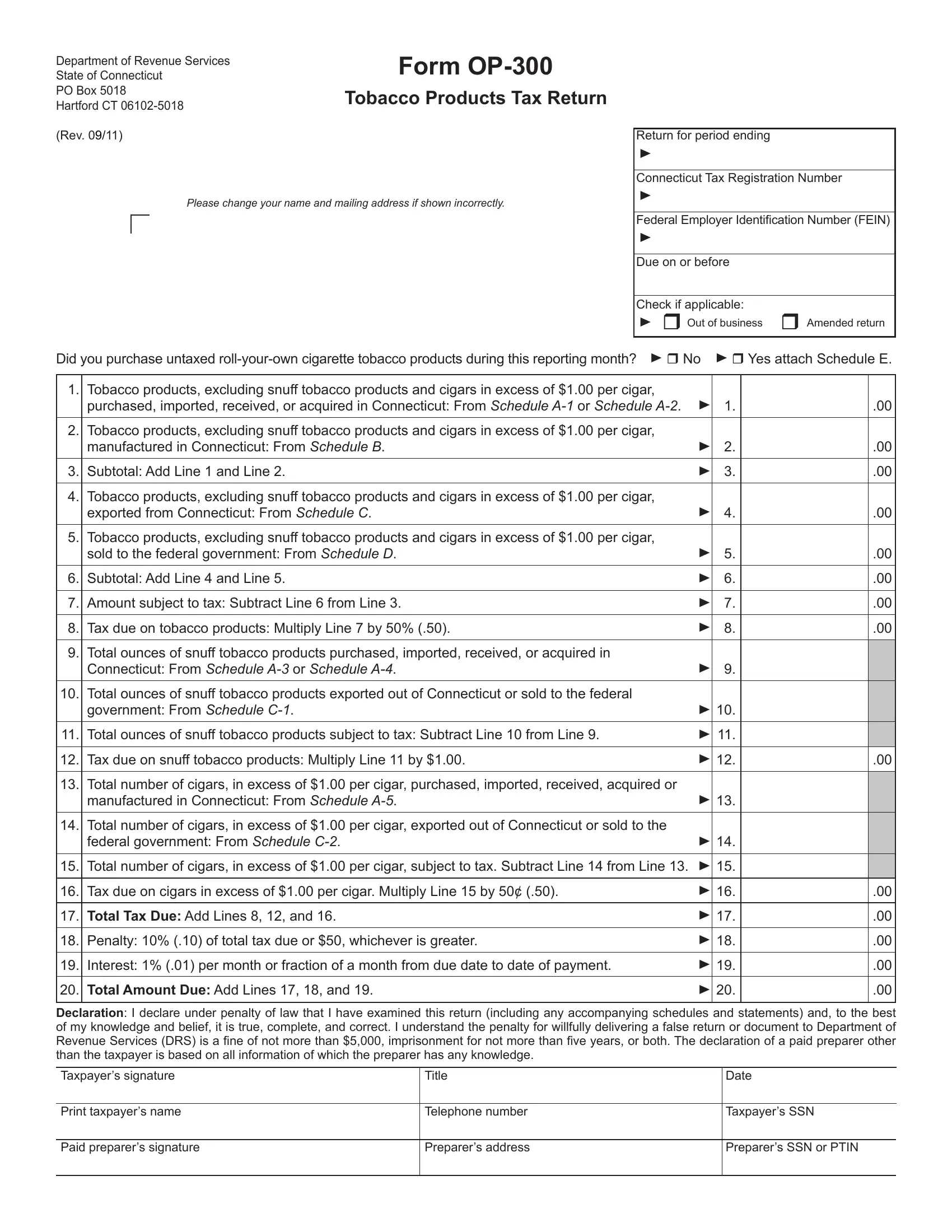

The Connecticut Op 300 form serves as a crucial document for entities dealing with tobacco products within the state, guiding them through the process of reporting and paying taxes on these goods. Issued by the Department of Revenue Services, this form is updated periodically to reflect the current tax rates and regulations impacting the tobacco industry. It meticulously outlines the reporting requirements for various categories of tobacco products, including but not limited to cigarettes, snuff, and cigars. Those required to file this return include distributors of tobacco products who have engaged in purchasing, importing, receiving, manufacturing, or acquiring tobacco products within Connecticut. The form is designed to calculate the tax due based on product type, with different sections dedicated to tobacco products in general, snuff tobacco products, and cigars priced over $1.00 each. Additionally, it factors in exemptions for products exported out of Connecticut or sold to the federal government. The comprehensive nature of this form highlights its importance in ensuring that tobacco product distributors comply with Connecticut's taxation laws, thereby contributing to the state's fiscal health. The instructions provided with the form emphasize the need for accuracy and timeliness in submitting both the payment and the documentation, including penalties for failure to do so, underlining the state's commitment to enforcing its tax policies.

| Question | Answer |

|---|---|

| Form Name | Connecticut Form Op 300 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | op 300 op300 ct form |

Department of Revenue Services |

Form |

|

State of Connecticut |

||

PO Box 5018 |

Tobacco Products Tax Return |

|

Hartford CT |

||

|

||

(Rev. 09/11) |

|

Please change your name and mailing address if shown incorrectly.

Return for period ending

Connecticut Tax Registration Number

Federal Employer Identiication Number (FEIN)

Due on or before

Check if applicable:

Out of business Amended return

Did you purchase untaxed

1. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

purchased, imported, received, or acquired in Connecticut: From Schedule |

|

1. |

|

.00 |

|

|

|

|

|

|

2. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

manufactured in Connecticut: From Schedule B. |

|

2. |

|

.00 |

|

|

|

|

|

|

3. |

Subtotal: Add Line 1 and Line 2. |

|

3. |

|

.00 |

|

|

|

|

|

|

4. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

exported from Connecticut: From Schedule C. |

|

4. |

|

.00 |

|

|

|

|

|

|

5. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

sold to the federal government: From Schedule D. |

|

5. |

|

.00 |

|

|

|

|

|

|

6. |

Subtotal: Add Line 4 and Line 5. |

|

6. |

|

.00 |

|

|

|

|

|

|

7. |

Amount subject to tax: Subtract Line 6 from Line 3. |

|

7. |

|

.00 |

|

|

|

|

|

|

8. |

Tax due on tobacco products: Multiply Line 7 by 50% (.50). |

|

8. |

|

.00 |

|

|

|

|

|

|

9. |

Total ounces of snuff tobacco products purchased, imported, received, or acquired in |

|

|

|

|

|

Connecticut: From Schedule |

|

9. |

|

|

10. |

Total ounces of snuff tobacco products exported out of Connecticut or sold to the federal |

|

|

|

|

|

government: From Schedule |

|

10. |

|

|

11. |

Total ounces of snuff tobacco products subject to tax: Subtract Line 10 from Line 9. |

|

11. |

|

|

12. |

Tax due on snuff tobacco products: Multiply Line 11 by $1.00. |

|

12. |

|

.00 |

|

|

|

|

|

|

13. |

Total number of cigars, in excess of $1.00 per cigar, purchased, imported, received, acquired or |

|

|

|

|

|

manufactured in Connecticut: From Schedule |

|

13. |

|

|

14. |

Total number of cigars, in excess of $1.00 per cigar, exported out of Connecticut or sold to the |

|

|

|

|

|

federal government: From Schedule |

|

14. |

|

|

15. |

Total number of cigars, in excess of $1.00 per cigar, subject to tax. Subtract Line 14 from Line 13. |

|

15. |

|

|

16. |

Tax due on cigars in excess of $1.00 per cigar. Multiply Line 15 by 50¢ (.50). |

|

16. |

|

.00 |

17. |

Total Tax Due: Add Lines 8, 12, and 16. |

|

17. |

|

.00 |

|

|

|

|

|

|

18. |

Penalty: 10% (.10) of total tax due or $50, whichever is greater. |

|

18. |

|

.00 |

|

|

|

|

|

|

19. |

Interest: 1% (.01) per month or fraction of a month from due date to date of payment. |

|

19. |

|

.00 |

|

|

|

|

|

|

20. |

Total Amount Due: Add Lines 17, 18, and 19. |

|

20. |

|

.00 |

|

|

|

|

|

|

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to Department of

Revenue Services (DRS) is a ine of not more than $5,000, imprisonment for not more than ive years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer’s signature |

Title |

Date |

Print taxpayer’s name

Telephone number

Taxpayer’s SSN

Paid preparer’s signature

Preparer’s address

Preparer’s SSN or PTIN

General Instructions

Complete the return in blue or black ink only.

Taxpayers must ile a return for each calendar month by the

Example: The tobacco products tax return for January 1 through

January 31 must be iled on or before February 25.

Taxpayers must ile a return even if no tax is due. All

supporting schedules can be found on the Department of Revenue Services (DRS) website at www.ct.gov/DRS

The owner, a partner, or a principal oficer must sign this

return.

Pay Electronically: Visit www.ct.gov/TSC to use the Taxpayer Service Center (TSC) to make a direct tax

payment. After logging onto the TSC, select the Make Payment Only option and choose a tax type from the drop down box. Using this option authorizes the DRS to electronically withdraw from your bank account (checking or savings) a payment on a date you select up to the due date.

As a reminder, even if you pay electronically you must still ile your return by the due date. Tax not paid on or before the

due date will be subject to penalty and interest.

If you do not pay electronically, make check payable to Commissioner of Revenue Services. DRS may submit

your check to your bank electronically.

Mail to: Department of Revenue Services

State of Connecticut

PO Box 5018

Hartford CT

Deinitions

TOBACCO PRODUCTS means: Cigars, cheroots, stogies, periques, granulated, plug cut, crimp cut, ready rubbed and

other smoking tobacco, cavendish, plug and twist tobacco, ine cut and other chewing tobaccos, shorts, refuse scraps,

clippings, cuttings and sweepings of tobacco, and all other kinds and forms of tobacco prepared in a manner as to be suitable for chewing or smoking in a pipe or otherwise for both

chewing and smoking, but does not include any cigarettes as deined in Conn. Gen. Stat.

SNUFF TOBACCO PRODUCTS means: Tobacco products that have imprinted on the packages the designation “snuff” or

“snuff lour” or the federal tax designation “Tax Class M,” or

both.

WHOLESALE SALES PRICE means:

•In the case of a distributor that is the manufacturer of the tobacco products, the price set for these products or, if no price has been set, the wholesale value of these products.

•In the case of a distributor that is not the manufacturer of the tobacco products, the price at which the distributor purchased the products.

Speciic Instructions

Check Box: You must check the appropriate box concerning the purchase of untaxed

Line 1

Resident Distributor: Enter from Schedule

wholesale sales price of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar)

purchased, imported, received, or acquired in Connecticut by the distributor.

Nonresident Distributor: Enter from Schedule

tobacco products and cigars in excess of $1.00 per cigar)

imported into Connecticut by the distributor.

Line 2 - Enter from Schedule B the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) manufactured in

Connecticut by the distributor.

Line 4 - Enter from Schedule C the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) exported from Connecticut

that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor. Prepare a separate Schedule C for each state of destination. (Use Line 9 and Line 10 to report snuff products and Line 13 and

Line 14 to report cigars in excess of $1.00 per cigar.)

Line 5 - Enter from Schedule D the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) sold to the federal

government that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor.

Line 9 - Enter from Schedule

Line 10 - Enter from Schedule

Line 13 - Enter from Schedule

acquired, or manufactured in Connecticut.

Line 14 - Enter from Schedule

sold to the federal government.

For Further Information

If you need additional information or assistance, please call the Excise Taxes Unit at

Forms and Publications: Visit the DRS website at www.ct.gov/DRS to download and print Connecticut tax

forms and publications.

TTY, TDD, and Text Telephone users only may transmit inquiries anytime by calling