Who Should File This Form?

File this form if you need more time to complete your Delaware individual income tax return. The extension is automatic and moves the filing deadline from April 30 to October 15. Joint filers must have both spouses sign the form, even if only one spouse had income during the year. If a taxpayer cannot sign due to illness or absence, a duly authorized agent may file on their behalf.

Does the Extension Cover Tax Payments?

No. The extension applies to the filing deadline only, not the payment deadline. Any tax balance owed must be paid by the original due date. Unpaid amounts accrue interest from the original due date until paid in full. Submit your estimated payment with the form to avoid interest charges.

What Are the Consequences of Filing Late?

Filing your Delaware income tax return after the deadline without an approved extension results in a penalty for late filing. The penalty applies unless you have reasonable cause for the delay. Filing Form 1027 by the original due date protects you from this penalty and gives you until October 15 to submit your complete return.

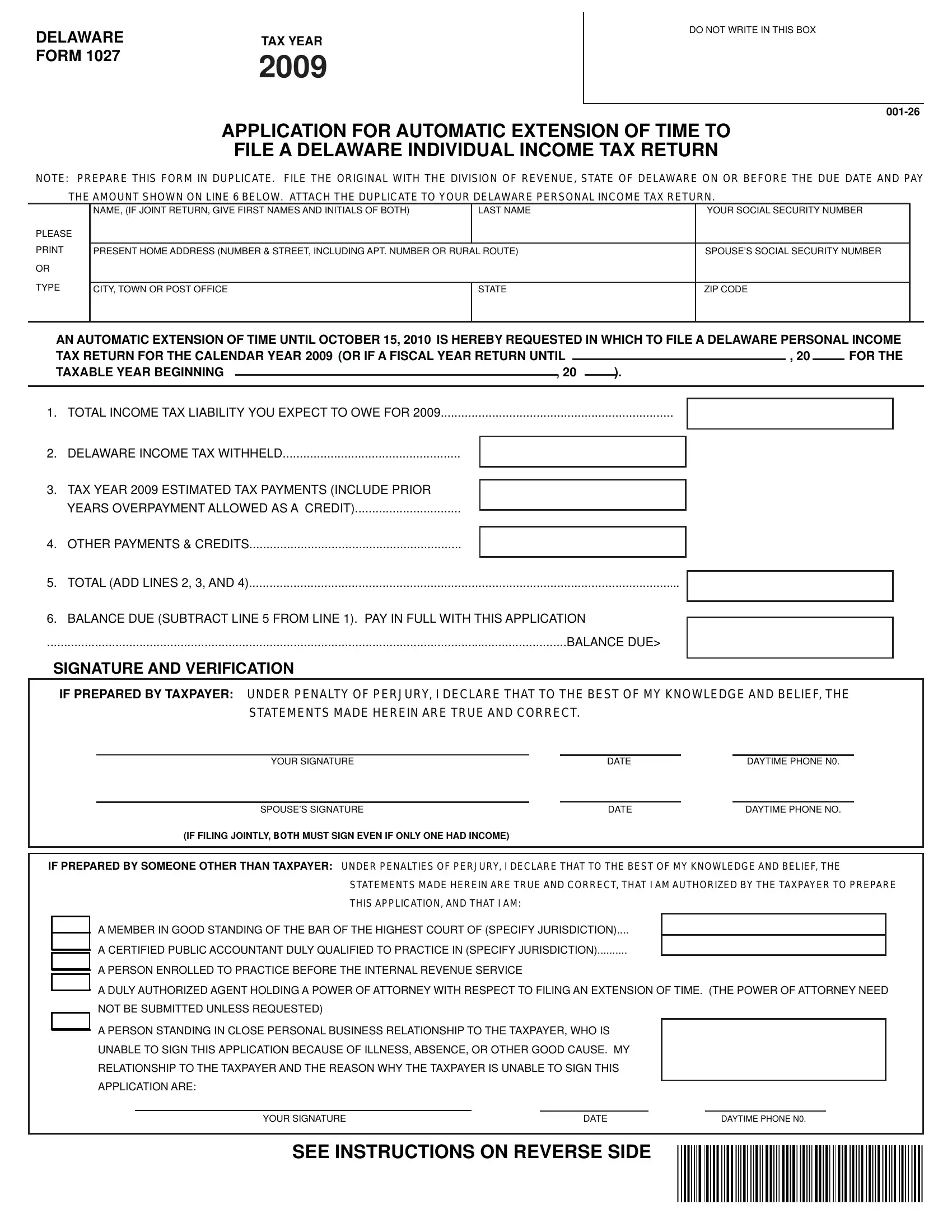

How to Complete the Form Step by Step

- Enter your expected total income tax liability for the current tax year.

- Record all Delaware state withholdings deducted from wages and other income sources.

- List estimated tax payments made during the year, including any prior year overpayment applied as a credit.

- Subtract withholdings and credits from your total liability to calculate the balance due.

- Submit payment for any balance due along with the original copy of the form.

- Keep the duplicate copy to attach to your final return when you file by October 15.

Related Tax Forms on FormsPal

After filing your extension, you will need to prepare your complete state tax return. Explore our annual income tax return form for general filing guidance, the income withholding form for reporting state withholdings, and the DC estate tax return form if you have additional state filing requirements.