How to Complete Delaware Form 200-ES

Follow these steps to fill out the Declaration of Estimated Income Tax correctly and on time.

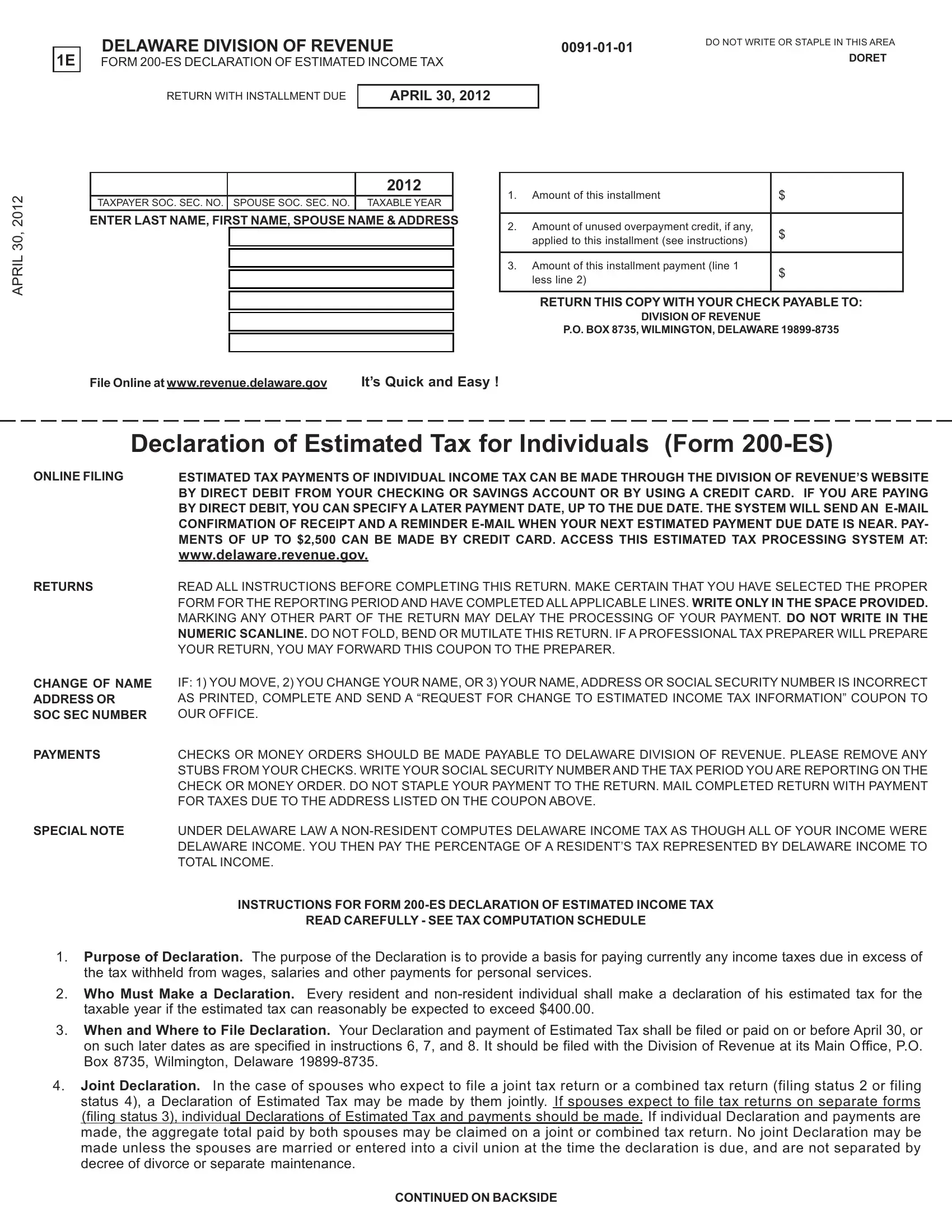

Step 1: Gather Your Tax Information

Before you begin, collect your most recent Delaware income tax return, any W-2 forms or 1099s for the current year, and your Social Security number. If you are filing jointly with a spouse, you will need the same documents for both filers.

Step 2: Calculate Your Estimated Delaware Tax

Estimate your total Delaware taxable income for the year. Apply the applicable Delaware state income tax rates to find your gross tax amount. Subtract any credits you expect to claim, then divide the remaining balance into four equal installment payments.

Step 3: Complete the Declaration

Enter your full name, current address, Social Security number, and the tax year at the top of the form. Fill in your estimated income, deductions, credits, and the payment amount for each installment period. Confirm that the totals on the form match your worksheet calculations before you sign.

Step 4: Submit and Pay

Mail the completed form with your check to the Delaware Division of Revenue, or pay electronically through the state's official payment portal. Payments are due April 30, June 30, September 30, and January 15. Keep a copy of the submitted form and your payment confirmation for your records.

Frequently Asked Questions

Who must file Form 200-ES?

Any individual who expects to owe more than $400 in Delaware income tax must file. This includes self-employed filers, retirees with pension or investment income, and anyone whose employer does not withhold enough Delaware tax during the year.

What are the installment payment due dates?

The four installments are due April 30, June 30, September 30, and January 15 of the following year. Missing a deadline or underpaying may trigger a penalty from the Delaware Division of Revenue.

Can I amend my estimated tax declaration?

Yes. If your income or deductions change mid-year, you may file a revised Form 200-ES for any remaining installment period. Adjust only the payments that have not yet come due.

For additional Delaware state forms, see the Delaware Form 1089 or browse other estimated tax payment forms by state.