Navigating the nuances of Texas Sales and Use Tax Return, as outlined in the 01 922 1 form, is integral for entities operating within diverse frameworks ranging from multiple outlet ownership to those engaged in specific contractual constructions, including out-of-state operations. This comprehensive document serves as a guide to accurately fulfill tax obligations, specifying who must file, the variegated filing frequencies, due dates, penalties for late submissions, and the intricacies of amending returns. Moreover, it addresses unique circumstances such as prepayments, claiming credits for overpayments or taxes paid in error, including the procedural intricacies for organizations like cities or special purpose districts retaining local sales and use tax. Detailed instructions provided ensure entities not only comply with filing requirements but also accurately report taxable sales, exempt transactions, and manage outlet-specific information. Emphasizing the criticality of maintaining detailed sales records to facilitate state audit processes, it underscores the legal implications of non-compliance. Additionally, it delineates the process for securing refunds, reinforcing the state's commitment to transparency and taxpayer support through readily available assistance channels and resources for further guidance.

| Question | Answer |

|---|---|

| Form Name | Form 01 922 1 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | form 01 922 tax form, form 01 922 pdf, texas 01 922, form01 922 |

Instructions for Completing

Texas Sales and Use Tax Return

These instructions are provided to assist in properly completing the

Texas Sales and Use Tax Return and supplements.

Who must file - You must file the long form if you:

•have more than one outlet or place of business;

•report tax to more than one city, transit authority, county or special purpose district (SPD);

•prepay your state and local taxes;

•report use tax from

•are a city, county or SPD that has chosen to retain your own local sales and use tax as authorized by the Texas Tax Code;

•have taken credit for taxes paid in error on purchases; or

•have custom broker refunds to report.

Returns must be filed for every period (month, quarter or year) even if there is no amount subject to tax or any tax due. If you're not sure whether you should file monthly, quarterly or yearly, call us at

When to file and pay - Returns must be filed or postmarked on or before the 20th day of the month following the end of each reporting period. If the due date falls on a Saturday, Sunday or legal holiday, the next business day will be the due date. Penalties and interest apply to taxes paid after they are due. A separate penalty applies to a report filed after the due date. See Item 14.

Business changes - If you are no longer in business or if your mailing or outlet address has changed, visit www.window.state.tx.us/taxinfo/sales, "Sales Tax Permit and Account Updates," or blacken the appropriate box to the right of Item g. on the return.

Instructions for filing amended Texas Sales and Use Tax Returns -

1)Make a copy of the original return you filed, or download a return online at

2)Write "Amended Return" on the top of the form, as shown in the example here:

3)If you're using a copy of your original return, cross out and revise the incorrect amounts. If you're using a blank return, enter the amounts as they should have appeared on the original return.

4)Sign and date the return.

If the amended return shows you underpaid your taxes, please

send the additional tax due plus any penalties and interest that may apply to the address provided on the return.

If the amended return shows you overpaid your taxes and you are requesting a refund, you must meet all of the requirements for a refund claim. Please refer to the Sales Tax

Need help? - For sales tax assistance, visit the Comptroller’s field office in your area or call

You must keep complete and detailed records of all sales as well as any deductions claimed, so returns can be verified by a state auditor. Failure to file this return or to pay applicable tax may result in collection action as prescribed by Title 2 of the Tax Code.

Disclosure of your Social Security number is required and authorized under law, for the purpose of tax administration and identi- fication of any individual affected by applicable law, 42 U.S.C. sec. 405(c)(2)(C)(i); Tex. Gov't Code Secs. 403.011 and 403.078. Release of information on this form in response to a public information request will be governed by the Public Information Act, Chapter 552, Government Code, and applicable federal law.

How can we better serve you? We welcome your feedback on these instructions through our quick online survey at

Form

Specific In |

|

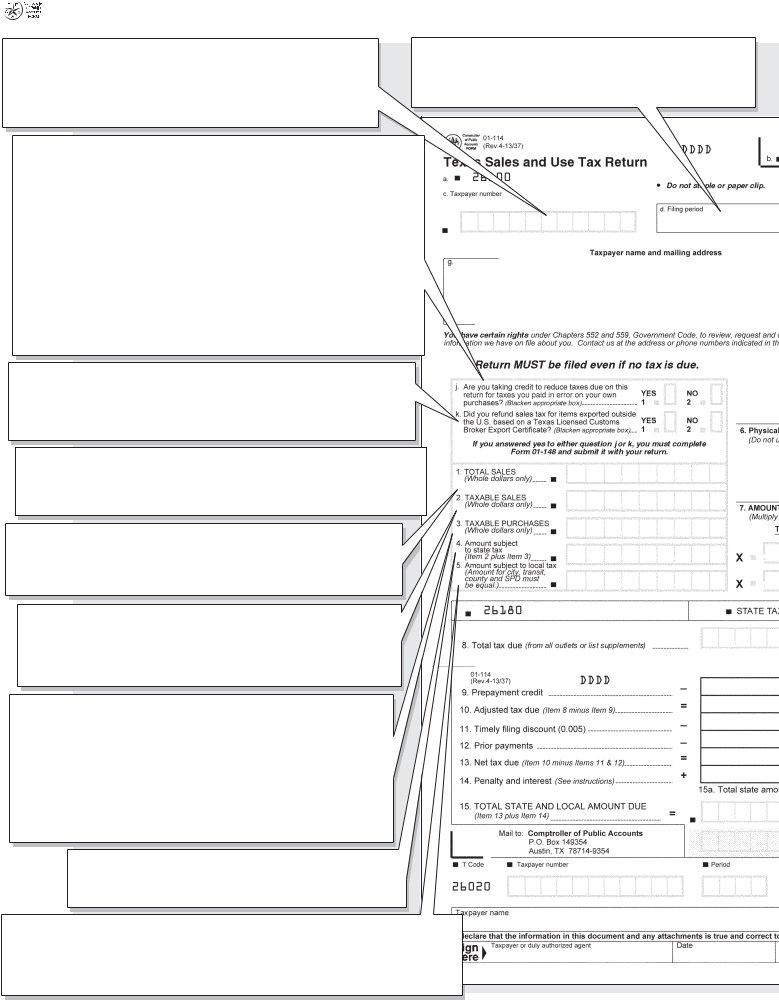

Item c. Enter the taxpayer number shown on your sales tax permit. |

Item d. If the return is not preprinted, enter the filing period |

If you have not received your sales tax permit and you are a |

of this report (month, quarter or year) and the last day of the |

sole owner, enter your Social Security number. Other types of |

period. Examples: “Quarter Ending |

organizations may enter their Federal Employer Identification |

|

Number (FEIN), if a taxpayer number has not been assigned. |

|

Item j. Indicate if you are taking a credit to reduce taxes due on this return for taxes you paid in error. If "YES," complete and submit the Credits and Customs Broker Schedule (Form

•tax paid in error to a vendor for items purchased for resale;

•tax paid in error to a vendor on exempt manufacturing equipment; or

•tax refunded to a purchaser for tax collected in error.

Claim the credit on Item 2 by subtracting the sum of purchases you paid taxes on in error, or refunded to a purchaser for tax collected in error, from the amount of taxable sales. Credit for a local taxing jurisdiction cannot be taken unless you have reported that jurisdiction on a previously filed tax return. A claim for refund must be filed directly with the Comptroller. Refund instructions are available at www.window.state.tx.us/taxinfo/refunds/sales/index.html.

Item k. If you refunded sales tax for items exported outside the U.S. based on a Texas Licensed Customs Broker Export Certificate, you must complete and submit the Credits and Customs Broker Schedule (Form

Items 1 - 7. If you have more than one place of business, you must file the outlet supplement (Form

Item 1. Enter the total amount (not including tax) of ALL sales, services, leases and rentals of tangible personal property including all related charges made during the reporting period. Report whole dollars only. Enter “0” if you have no sales to report.

Item 2. Enter the total amount (not including tax) of all TAXABLE services and TAXABLE sales, leases and rentals of tangible personal property including all TAXABLE related charges made during the reporting period. Report whole dollars only. Enter “0” if you have no taxable sales to report.

Item 3. Enter the total amount of taxable purchases that you made for your own use. Taxable purchases include items that were purchased, leased or rented for personal or business use on which sales or use tax was not paid. This includes purchases from in- or

Item 4. Add Taxable Sales (Item 2) to Taxable Purchases (Item 3), and enter the result in Item 4. Do not include Total Sales (Item 1) in this total. Report whole dollars only.

Item 5. To report local tax by outlet, the amount subject to local tax must be the same for all local taxing authorities (city, transit, county and/or special purpose district) for that outlet. If any of these local amounts are different for the outlet, you MUST report your local tax on the List Supplement (Form

nstructions

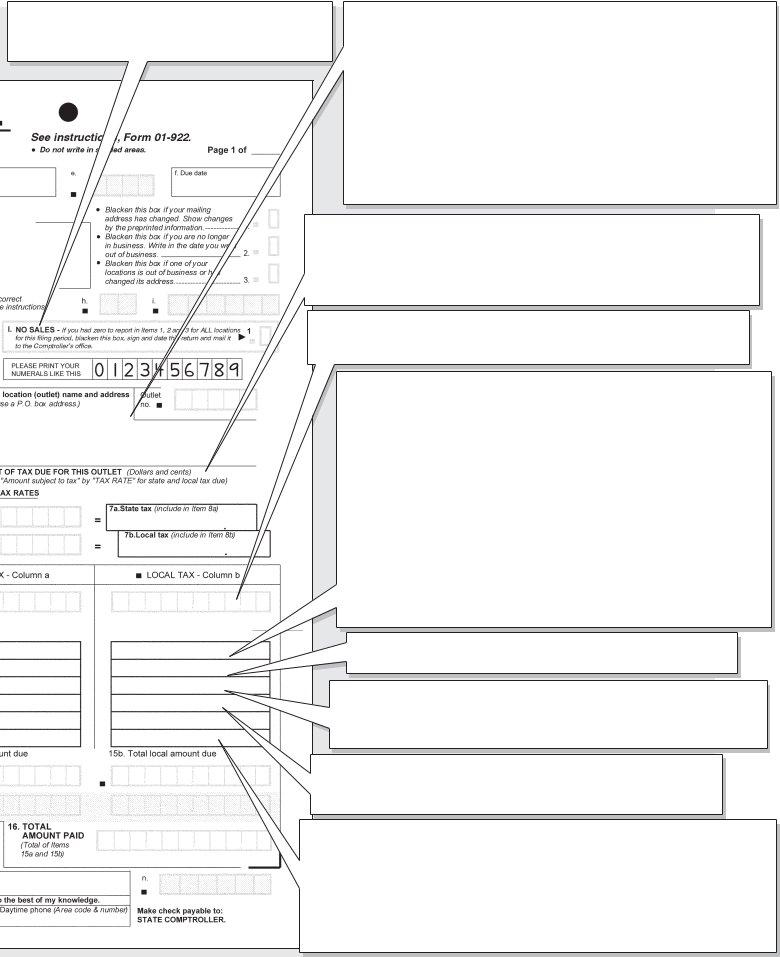

Item l. If you had zero to report in Items 1, 2 and 3 for all outlets during this filing period, blacken this box, sign and date this return and mail to the Comptroller’s office.

Item 6. Enter the trade name, actual location and five digit outlet number shown on your sales tax permit for each outlet you are reporting. Use street address. Do not use P.O. Box or Rural Route number.

•If you do not have a permit, leave outlet number blank.

•If you are reporting use tax from

•If the physical location (outlet) is no longer in business, write “out of business” and date of closing next to any outlet that is no longer in business.

•If the physical location address is different from the preprinted physical location address, make correction next to the incorrect information.

•If a new outlet has been opened, write the outlet trade name, actual location and opening date in a blank space on the return along with a brief description of the business.

Items 7a and 7b. Multiply Item 4 by the state tax rate and enter in Item 7a. Multiply Item 5 by the local tax rate and enter in Item 7b. If your return is not

Item 8. Combine the state sales tax due from all outlets (Items 7a) and enter the total tax in Column a. Combine local sales tax due from Item 7b from all pages and enter the total tax in Column b.

Item 9. The amount preprinted in Item 9 includes the amount of your pre- payment plus the allowable prepayment discount.

•If you prepaid timely and the amount is not printed in Item 9, calculate the credit by dividing the prepaid amount by .9825, and enter the result in Item 9.

•If the total tax due in either column of Item 8 is greater than the prepayment, enter the difference in Item 10. Multiply the difference by .005 and enter the result in Item 11.

•If the total due in either Item 8a or 8b is less than the prepayment credit in Item 9a or 9b, enter the difference in Item 10a or 10b. Multiply the difference by .9825 and enter the result in Item 13 to determine the amount of refund. Bracket the amount as <xxx.xx>.

•If you are filing your return or paying the tax late, mark out the preprinted amount in Item 9 and enter the actual amount paid with your prepayment report.

Note: Discount applies only if all prepayment requirements are met AND your regular sales and use tax return AND any additional payments are postmarked by the due date.

Item 10. Subtract the prepayment credit in Item 9 from the total tax due in Item 8. Enter the result in Item 10.

Item 11. If you are filing your return and paying the tax due on or before the due date, multiply the total tax due in Item 8 by 1/2 percent (.005) and enter the result in Item 11. (Prepayers: See instructions for Item 9.)

Note: Do not take the discount if the return and/or payment is not timely.

Item 12. If you requested that a prior payment and/or an overpayment be applied to this period, a preprinted return from the Comptroller's office will include this amount in Item 12.

Item 14. Penalty and interest

•

•

•Over 60 days late: Enter 10 percent (.10) penalty plus interest. Calculate interest at the rate published online at www.window.state.tx.us, or call the Comptroller at

Note: An additional $50 late filing penalty will be assessed each time a return is filed after the due date.

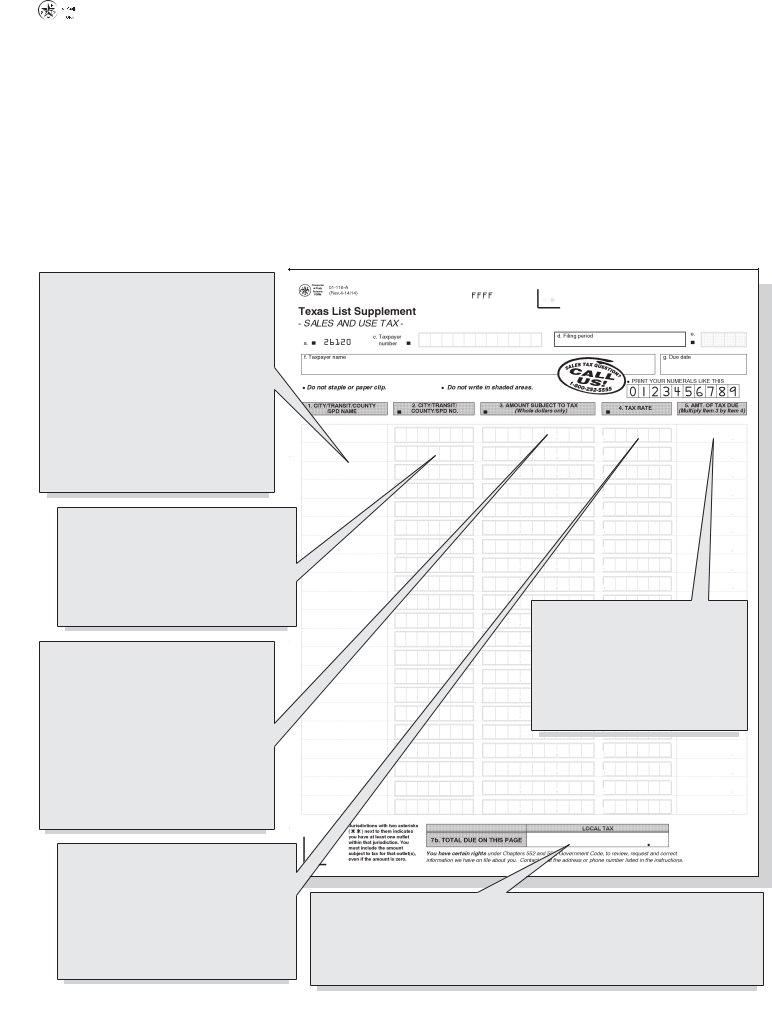

Instructions for Completing Texas Sales and Use Tax Return List Supplement

Who must file the list supplement? You must file the list supplement with the Texas Sales and Use Tax Return if you:

•are an

•are a contractor performing new constructions under a separate contract;

•are a contractor performing residential real property repair and remodeling under a separated contract;

•are an itinerant vendor; or

•are an auctioneer.

You must also file the list supplement if you provide any of the following services:

• nonresidential real property repair or remodeling |

• |

mobile telecommunications services; |

|

|

services; |

• |

landline telecommunications services; |

• |

amusement services; |

• |

waste collections services; |

• |

cable or satellite television services; |

• |

natural gas or electricity. |

Note: Other circumstances may require you to file by list. If you have specific questions, call us at

Column 1. This column should include the names of all cities, transit organizations, counties and special purpose districts (SPDs) in which you did business during the reporting period. If the form is preprinted, names of some jurisdictions will already be printed in this column. Jurisdictions with two asterisks (**) next to them indicates you have at least one outlet within that jurisdiction. You must include the amount subject to tax for that outlet(s), even if the amount is zero.

Column 2. This column should include the

Column 3. The amount subject to tax is the taxable sales plus taxable purchases that are subject to local tax for each jurisdiction listed in Column 1. Jurisdictions with two asterisks (**) next to them indicates you have at least one outlet within that jurisdiction. You must include the amount subject to tax for that outlet(s), even if the amount is zero. Report whole dollars only. If an amount is negative, bracket it as <x,xxx>.

Column 4. This column should include the local tax rate, ranging from 1/8 of 1 percent to 2 percent, for each local taxing jurisdiction listed in Column 1. Local rates can be found online at www.window.state.tx.us/taxinfo/local/.

Column 5. AMOUNT OF TAX DUE - To calculate the tax due, multiply each amount in Column 3 by the respective tax rate listed in Column 4. Enter dollars and cents. If an amount is negative, bracket it as <x,xxx.xx>.

Item 7b. Add the amounts in Column 5 of this page and enter the total in Item 7b. Combine the totals in Item 7b of all List Supplements (Form