Navigating the complexities of tax assessments, penalties, and the appeals process can be daunting for taxpayers in Alaska. The 0405 775 form, officially known as the Alaska Department of Revenue Request for Informal Conference, serves as a critical tool for those who find themselves in disagreement with the decisions made by the Department of Revenue concerning their tax obligations. This form allows individuals and entities to formally request an informal conference to discuss and potentially dispute assessments or adjustments, including tax penalties. It mandates the provision of detailed information such as taxpayer identification, contact details, and the specific basis of the appeal, thereby setting the stage for a comprehensive review of the case by an Appeals Officer. Furthermore, it outlines the procedural steps required, including the necessity of filing within a specified timeframe to avoid mandatory payment of the disputed amount and the importance of attaching pertinent documentation, such as a copy of the assessment letter. Beyond its operational directives, the form also tacitly introduces the appellants to the reality of accrued interest on tax deficiencies, as dictated by Alaska Statute AS 43.05.225, underscoring the financial implications of the appeal process. Through this form, the Alaskan tax system provides a pathway for taxpayers to voice their concerns and seek redress, while also emphasizing the legal and financial responsibilities that accompany the pursuit of an appeal.

| Question | Answer |

|---|---|

| Form Name | Form 0405 775 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | conference alaska request for informal conference |

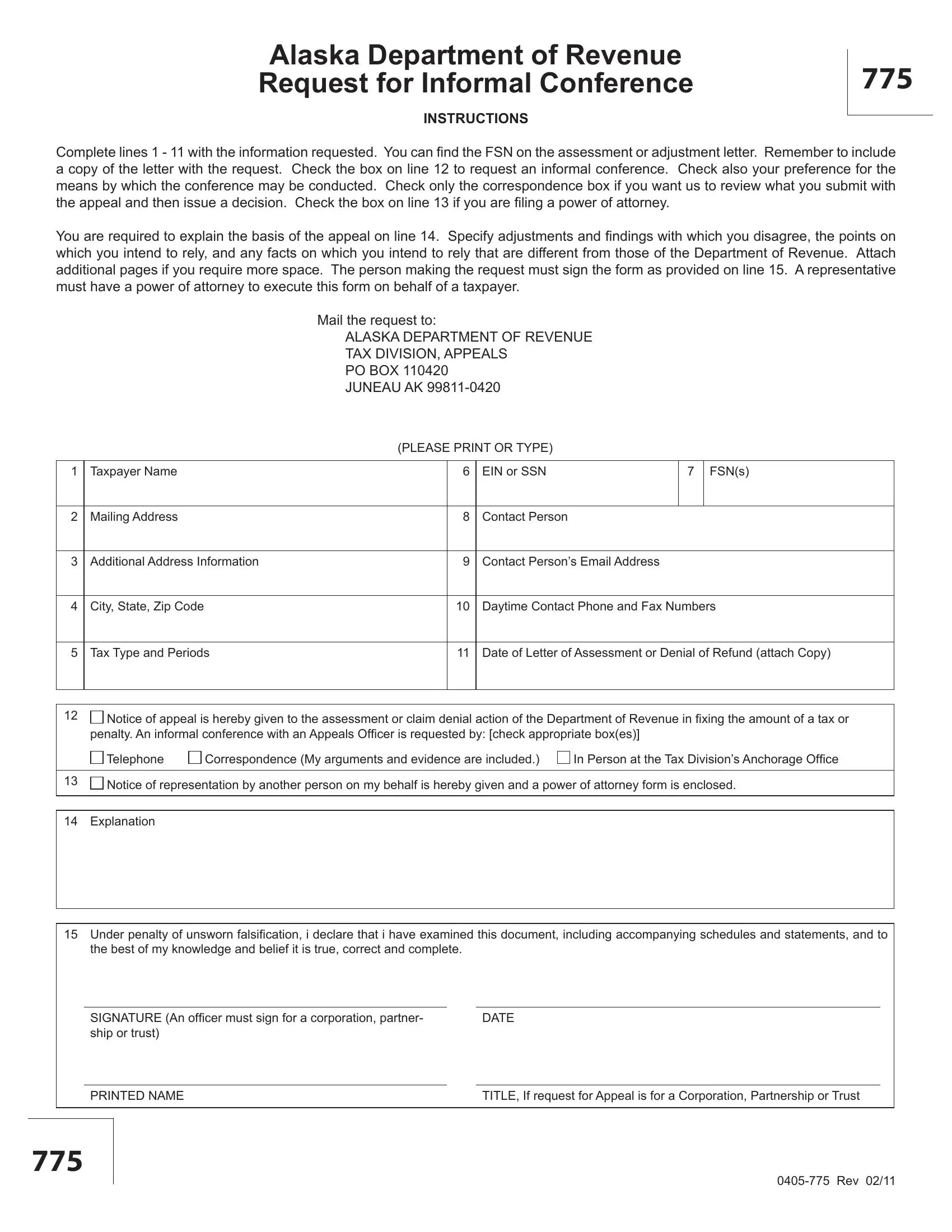

Alaska Department of Revenue Request for Informal Conference

INSTRUCTIONS

775

Complete lines 1 - 11 with the information requested. You can ind the FSN on the assessment or adjustment letter. Remember to include a copy of the letter with the request. Check the box on line 12 to request an informal conference. Check also your preference for the means by which the conference may be conducted. Check only the correspondence box if you want us to review what you submit with the appeal and then issue a decision. Check the box on line 13 if you are iling a power of attorney.

You are required to explain the basis of the appeal on line 14. Specify adjustments and indings with which you disagree, the points on which you intend to rely, and any facts on which you intend to rely that are different from those of the Department of Revenue. Attach additional pages if you require more space. The person making the request must sign the form as provided on line 15. A representative must have a power of attorney to execute this form on behalf of a taxpayer.

Mail the request to:

ALASKA DEPARTMENT OF REVENUE

TAX DIVISION, APPEALS

PO BOX 110420

JUNEAU AK

(PLEASE PRINT OR TYPE)

1 |

Taxpayer Name |

|

6 |

EIN or SSN |

|

7 |

FSN(s) |

|

|

|

|

|

|

|

|

|

|

2 |

Mailing Address |

|

8 |

Contact Person |

|

|

|

|

|

|

|

|

|||||

3 |

Additional Address Information |

9 |

Contact Person’s Email Address |

|||||

|

|

|

|

|

||||

4 |

City, State, Zip Code |

|

10 |

Daytime Contact Phone and Fax Numbers |

||||

|

|

|

|

|||||

5 |

Tax Type and Periods |

11 |

Date of Letter of Assessment or Denial of Refund (attach Copy) |

|||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

12 |

Notice of appeal is hereby given to the assessment or claim denial action of the Department of Revenue in ixing the amount of a tax or |

|||||||

|

penalty. An informal conference with an Appeals Oficer is requested by: [check appropriate box(es)] |

|||||||

|

Telephone |

Correspondence (My arguments and evidence are included.) |

In Person at the Tax Division’s Anchorage Ofice |

|||||

|

|

|

|

|

|

|

||

13 |

Notice of representation by another person on my behalf is hereby given and a power of attorney form is enclosed. |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

Explanation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

15 |

Under penalty of unsworn falsiication, i declare that i have examined this document, including accompanying schedules and statements, and to |

|||||||

|

the best of my knowledge and belief it is true, correct and complete. |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

SIGNATURE (An oficer must sign for a corporation, partner- |

|

DATE |

|

|

|

|

|

|

ship or trust) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PRINTED NAME |

|

|

TITLE, If request for Appeal is for a Corporation, Partnership or Trust |

||||

|

|

|

|

|

|

|

|

|

775

Alaska Department of Revenue

Request for Informal Conference

THE APPEAL PROCESS

If you disagree with the action of the Department of Revenue in ixing the amount of a tax or penalty, you must request an informal conference within 60 days of the date of the assessment, refund denial, or other action. You are not required to pay the amounts in dispute if the request is iled on time. A request that is not iled on time will be dismissed. The United States postmark date on the envelope is considered the iling date. A return receipt from certiied mail is accepted as proof of mailing.

The Department will assign the request to an Appeals Oficer to conduct the informal conference. The Appeals Oficer will contact you, if appropriate, at a future date to schedule a date and time for the conference. The informal conference process by the Appeals Oficer is not necessarily limited to the issues in the request. At the conclusion of the process, the Department will issue a written informal conference decision. The informal conference decision is the inal decision by the Department of Revenue on the action. Appeal of the informal conference decision is to the Ofice of Administrative Hearings in the Department of Administration.

IMPORTANT NOTICE REGARDING INTEREST

The Alaska interest provision, AS 43.05.225, provides that statutory interest accrues on a tax deiciency. A tax is deicient on the day following the day on which it is due and unpaid. A tax is due on the last day allowed by law for payment without regard to extensions of time to ile or pay. The current interest rate is compounded quarterly. The interest when compounded each quarter becomes part of the tax and increases the base for computing additional interest. Interest is not computed on a penalty. A penalty therefore does not have any effect on the interest that may otherwise be due.

The law does not allow the department to give up or decrease any interest that has accrued on a tax deiciency. Interest is not a penalty but is instead a charge for the time value of money. The Alaska Supreme Court has held that interest accrues on a tax deiciency regardless of whether a party is at fault. Therefore, an administrative delay or other omission in resolving a tax dispute does not inluence the accrual of interest.

A taxpayer that receives a tax assessment must decide whether to pay the assessment to stop additional interest from accruing. The payment of the tax assessment does not prevent a taxpayer from disputing the assessment by iling a request for informal conference with the Department. Since the appeal process can take years to come to a conclusion, and taking into consideration that both the taxpayer and the department can appeal adverse decisions to the courts, a taxpayer that pays the assessment is protected against additional interest charges. Furthermore, since the department pays interest to a taxpayer on the same basis as paid by the taxpayer, the taxpayer will receive interest on the amount paid if the assessment is overturned. Thus, a taxpayer must choose to accept the risk of owing additional interest by not paying the assessment or to shift that risk to the department by paying it.