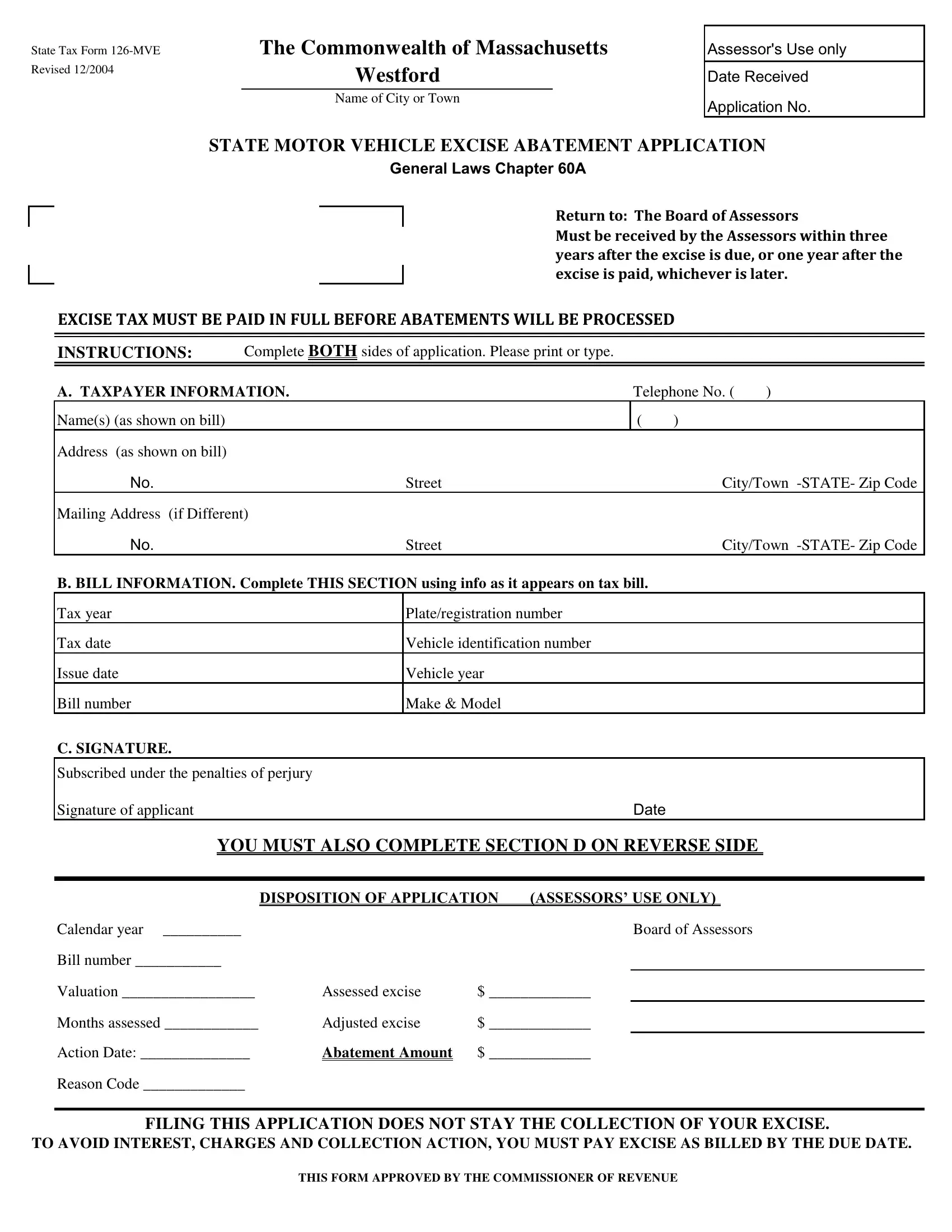

In the Commonwealth of Massachusetts, vehicle owners are subject to an excise tax, which is a levy on motor vehicles registered in the state, calculated as a percentage of the car's manufacturer's list price when new. The State Tax Form 126-MVE, revised in December 2004, serves as a crucial document for those seeking an abatement, or reduction, of this excise under certain conditions outlined by General Laws Chapter 60A. This application, addressing a range of circumstances such as vehicle transfer, theft, or relocation out of Massachusetts, must reach the Board of Assessors no later than three years after the due date of the excise or one year following its payment, adhering to the stipulation that excise taxes must be settled in full beforehand. Detailed within the form are specifications for taxpayer and vehicle information, alongside a mandate for applicants to elucidate their reasons for seeking abatement, all under the specter of perjury for any misinformation. An insightful aspect of the procedure is the non-eligibility for abatement if one cancels their vehicle's registration but retains ownership or relocates within Massachusetts within the same calendar year. Not only does the form navigate taxpayers through the abatement process, but it also emphasizes the non-deferral of excise collection upon filing, outlining potential financial and legal repercussions of non-compliance. By completion, the 126-MVE form emerges as a significant document for Massachusetts vehicle owners, encapsulating the intricacy of state tax obligations while offering a pathway to financial relief under specific legal frameworks.

| Question | Answer |

|---|---|

| Form Name | Form 126 Mve |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Assessors, junked, 2004, Excises |

State Tax Form |

The Commonwealth of Massachusetts |

|

Revised 12/2004 |

Westford |

|

|

||

|

|

|

|

Name of City or Town |

|

Assessor's Use only

Date Received

Application No.

STATE MOTOR VEHICLE EXCISE ABATEMENT APPLICATION

General Laws Chapter 60A

Return to: The Board of Assessors

Must be received by the Assessors within three years after the excise is due, or one year after the excise is paid, whichever is later.

EXCISE TAX MUST BE PAID IN FULL BEFORE ABATEMENTS WILL BE PROCESSED

INSTRUCTIONS: |

Complete BOTH sides of application. Please print or type. |

|

|

|

|||||||

|

|

|

|

|

|

|

|||||

A. TAXPAYER INFORMATION. |

|

|

|

|

Telephone No. ( |

) |

|||||

Name(s) (as shown on bill) |

|

|

|

|

|

|

( |

) |

|

|

|

Address (as shown on bill) |

|

|

|

|

|

|

|

|

|

|

|

No. |

|

|

|

|

Street |

|

|

|

|

City/Town |

|

Mailing Address |

(if Different) |

|

|

|

|

|

|

|

|

||

No. |

|

|

|

|

Street |

|

|

|

|

City/Town |

|

B. BILL INFORMATION. Complete THIS SECTION using info as it appears on tax bill. |

|

|

|

||||||||

Tax year |

|

|

|

|

Plate/registration number |

|

|

|

|||

Tax date |

|

|

|

|

Vehicle identification number |

|

|

|

|||

Issue date |

|

|

|

|

Vehicle year |

|

|

|

|

|

|

Bill number |

|

|

|

|

Make & Model |

|

|

|

|

|

|

C. SIGNATURE. |

|

|

|

|

|

|

|

|

|

|

|

Subscribed under the penalties of perjury |

|

|

|

|

|

|

|

|

|||

Signature of applicant |

|

|

|

|

|

|

Date |

|

|

|

|

|

YOU MUST ALSO COMPLETE SECTION D ON REVERSE SIDE |

|

|||||||||

|

|

|

|

|

|

|

|||||

|

|

|

DISPOSITION OF APPLICATION |

(ASSESSORS’ USE ONLY) |

|

|

|||||

Calendar year |

__________ |

|

|

|

|

|

|

Board of Assessors |

|

||

Bill number ___________ |

|

|

|

|

|

|

|

|

|

|

|

Valuation _________________ |

Assessed excise |

$ _____________ |

|

|

|

|

|||||

Months assessed ____________ |

Adjusted excise |

$ _____________ |

|

|

|

|

|||||

Action Date: ______________ |

Abatement Amount |

$ _____________ |

|

|

|

|

|||||

Reason Code _____________ |

|

|

|

|

|

|

|

|

|||

FILING THIS APPLICATION DOES NOT STAY THE COLLECTION OF YOUR EXCISE.

TO AVOID INTEREST, CHARGES AND COLLECTION ACTION, YOU MUST PAY EXCISE AS BILLED BY THE DUE DATE.

THIS FORM APPROVED BY THE COMMISSIONER OF REVENUE

D.REASON(S) ABATEMENT SOUGHT. Check reason(s) you are applying and provide the specified documentation.

q Vehicle sold or traded |

1.) |

Bill of sale OR COPY of P&S AND |

2.) Plate return receipt or A COPY |

||||

|

|

OF the NEW registration form if plate transferred to another vehicle |

|||||

q Vehicle stolen or total loss |

|

Insurance settlement letter from Ins. C AND |

|

|

|

||

1.) |

2.) Plate return receipt or A COPY |

||||||

|

|

OF the NEW registration form if plate transferred to another vehicle |

|||||

q Vehicle repossessed |

1.) |

Notice from lienholder |

2.) |

AND plate return receipt, |

|||

q Vehicle junked |

1.) |

Receipt from junk yard |

2.) |

AND plate return receipt, |

|||

q Vehicle returned |

1.) |

Letter from dealer certifying return of vehicle |

'(Lemon Law) |

2.) AND plate return receipt, |

|

q Moved from billing city/town |

1.) |

Proof RMV was notified before January 1 of GARAGING change for registration |

before January 1 of tax year |

|

INSURANCE COVERAGE PAGE SHOWING GARAGING OF VEHICLE AS OF JANUARY 1 |

NOTE: |

|

You are not entitled to an abatement if you moved to another Massachusetts city or town |

Date of move: ________/________/_________ |

|

during the same calendar year of the excise tax. You must notify the RMV within 30 days |

|

|

of moving and before January 1 to be billed by your new city or town next year. |

q Moved from Massachusetts |

1.) |

COPY OF Registration from the new state |

Date of move: ________/________/_________ |

|

AND 2.) Plate return receipt or A LOST PLATE |

q Exemption Type: |

1.) |

_______________________________ Documentation establishing qualifications |

q Other Explain: |

1.) |

____________________________________________ Relevant documentation |

INFORMATION ABOUT YOUR MOTOR VEHICLE EXCISE

MOTOR VEHICLE EXCISE: You must pay an excise tax for any calendar year you own and register a motor vehicle in Massachusetts.

The excise is assessed as of January 1, or the first day of the month the vehicle is registered if registered after January 1. Bills are issued by the city or town where you reside or have your principal place of business based on Registry of Motor Vehicle registration records as of that assessment date. The excise valuation is a percentage of the manufacturer's recommended list price of the vehicle when new (not the sales price or current market value). The percentages are: 50% for the calendar year before the model year, 90% for the model year, 60% for the second year, 40% for the third year, 25% for the fourth year, and 10% for the fifth and following years. Excises for vehicles registered after January 1 are

ABATEMENTS. You may be entitled to an abatement (or a refund if the excise has been paid) if the vehicle is valued at more than the percentage of manufacturer’s list price that applies for the calendar year. Abatements may also be granted if you do any of the

following during the same calendar year: (1) transfer ownership of the vehicle, (2) move out of Massachusetts, (3)

DEADLINE. Your abatement application must be received by the Board of Assessors within three years after the excise was due, or one year after the excise was paid, whichever is later. To preserve your right to an abatement and to appeal, you must

file on time. By law, Assessors may only act on late applications in limited circumstances where the excise is still unpaid and their decision in those cases is final.

PAYMENT. Filing an application does not stay the collection of your excise. Failure to pay the excise when due may subject you to interest charges, fines, fees and collection action, including

collection charges or action, you must pay the excise in full within 30 days of the bill’s issue date.

You will receive a refund if an abatement is granted.

DISPOSITION. The assessors have 3 months from the application filing date to act unless you agree in writing to their request to

extend the action period for a specific time. If the assessors do not act on your application within the original or extended period, it is deemed denied. You will be notified in writing if an abatement has been granted or denied.

CONTACT THE ASSESSORS’ OFFICE IF YOU HAVE ANY QUESTIONS ABOUT YOUR EXCISE BILL OR ABATEMENT RIGHTS