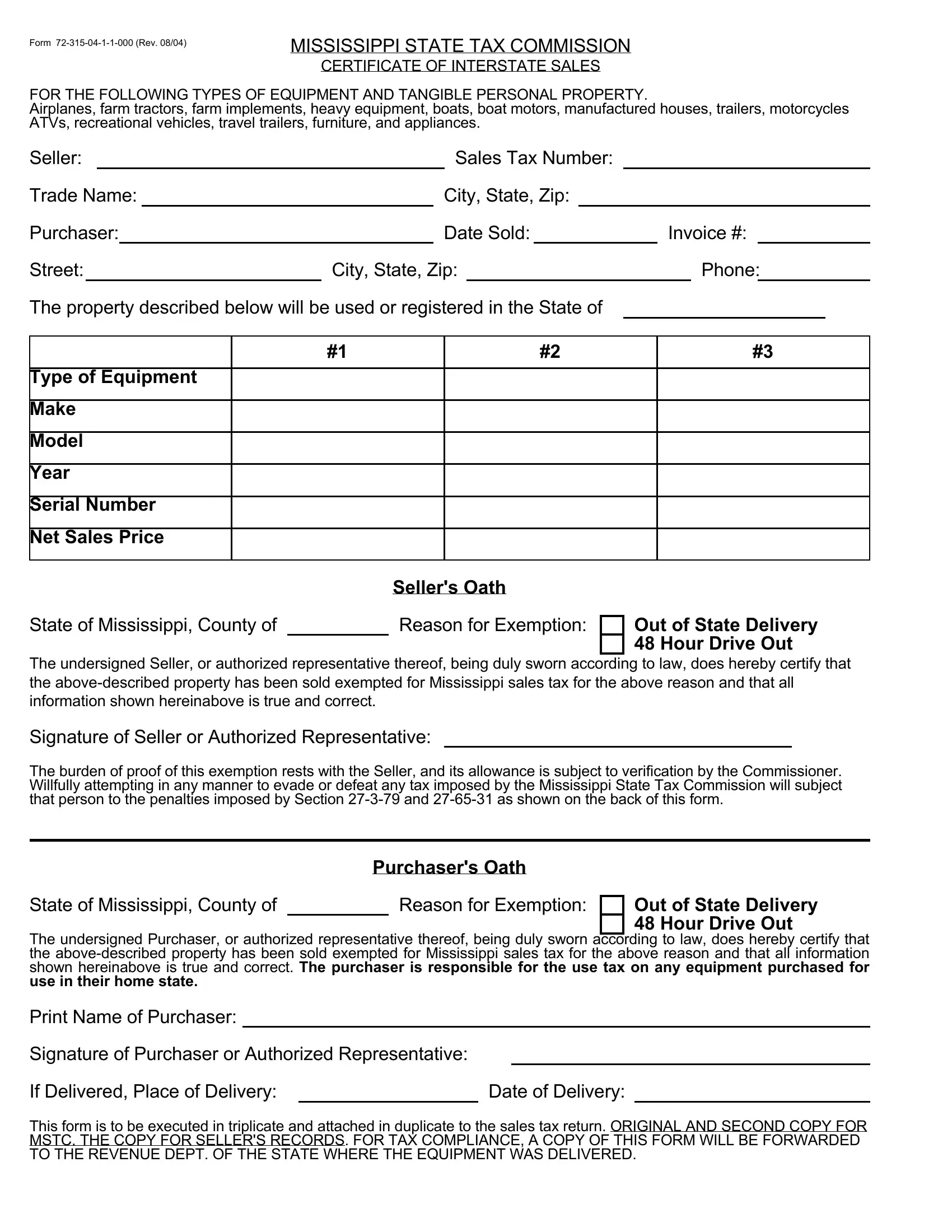

Understanding the nuances of the Form 72-315-04-1-1-000 is crucial for businesses involved in the sale of specific types of equipment and tangible personal property, such as airplanes, farm tractors, heavy machinery, boats, and various recreational vehicles, among others, in the state of Mississippi. This form, revised in August 2004 by the Mississippi State Tax Commission, serves as a certificate for interstate sales, allowing transactions to be exempted from Mississippi sales tax under specific conditions like out-of-state delivery or a 48-hour drive-out period. Sellers must provide comprehensive details about the sale, including their sales tax number and the items sold, while affirming their compliance through a signed oath. Similarly, purchasers are required to attest to the information's accuracy and acknowledge their responsibility for use tax in their home state if applicable. The significance of this form extends beyond tax exemption; it emphasizes the legal obligation of both seller and buyer to accurately report such transactions. Misrepresentation or attempts to evade taxes can lead to severe penalties, as outlined by Sections 27-3-79 and 27-65-31, including fines and imprisonment. Moreover, the form underlines the principle that funds collected in anticipation of sales tax are to be held in trust for the state, reinforcing the legal and fiscal responsibilities incumbent upon businesses operating within or engaging with counterparts in Mississippi.

| Question | Answer |

|---|---|

| Form Name | Form 72 315 04 1 1 000 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Mississippi ms state tax commission atv form |

Form

MISSISSIPPI STATE TAX COMMISSION

CERTIFICATE OF INTERSTATE SALES

FOR THE FOLLOWING TYPES OF EQUIPMENT AND TANGIBLE PERSONAL PROPERTY.

Airplanes, farm tractors, farm implements, heavy equipment, boats, boat motors, manufactured houses, trailers, motorcycles ATVs, recreational vehicles, travel trailers, furniture, and appliances.

Seller: |

|

|

|

Sales Tax Number: |

|

|

|

|

|

|||||||

Trade Name: |

|

|

|

City, State, Zip: |

|

|

|

|

|

|

||||||

Purchaser: |

|

|

Date Sold: |

|

Invoice #: |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Street: |

|

|

City, State, Zip: |

|

|

|

Phone: |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||

The property described below will be used or registered in the State of |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

#1 |

|

#2 |

|

|

#3 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Type of Equipment |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Make |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Model |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Year |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Serial Number |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Net Sales Price |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller's Oath

State of Mississippi, County of |

|

Reason for Exemption: |

Out of State Delivery 48 Hour Drive Out

The undersigned Seller, or authorized representative thereof, being duly sworn according to law, does hereby certify that the

Signature of Seller or Authorized Representative:

The burden of proof of this exemption rests with the Seller, and its allowance is subject to verification by the Commissioner. Willfully attempting in any manner to evade or defeat any tax imposed by the Mississippi State Tax Commission will subject that person to the penalties imposed by Section

|

Purchaser's Oath |

|

|

|

State of Mississippi, County of |

|

Reason for Exemption: |

|

Out of State Delivery |

|

|

|||

|

|

|

|

48 Hour Drive Out |

The undersigned Purchaser, or authorized representative thereof, being duly sworn according to law, does hereby certify that the

use in their home state.

Print Name of Purchaser:

Signature of Purchaser or Authorized Representative:

If Delivered, Place of Delivery: |

|

Date of Delivery: |

This form is to be executed in triplicate and attached in duplicate to the sales tax return. ORIGINAL AND SECOND COPY FOR MSTC. THE COPY FOR SELLER'S RECORDS. FOR TAX COMPLIANCE, A COPY OF THIS FORM WILL BE FORWARDED TO THE REVENUE DEPT. OF THE STATE WHERE THE EQUIPMENT WAS DELIVERED.

Section

Any person who willfully attempts in any manner to evade or defeat any tax imposed by the State Tax Commission or assists in the evading of such tax or in the payment thereof, shall in addition to other penalties provided by law, be guilty of a felony and, upon conviction thereof shall be fined not more than One Hundred Thousand Dollars ($100,000.00) and, in the case of a corporation, not more than Five Hundred Thousand Dollars ($500,000.00), or imprisoned not more than five (5) years, or both.

Section

The funds collected by the taxpayer (Seller) from the Purchaser pursuant to the provisions of this chapter shall be considered "trust Fund monies" and the taxpayer shall hold these funds in trust for the State of Mississippi; said funds to be separately accounted for as provided by regulation of the Commissioner. If the taxpayer fails to remit these trust fund monies as required by law, then the taxpayer may be assessed with a penalty in three (3) times that amount of taxes due. This penalty is to be assessed and collected in the same manner as taxes imposed by this chapter and shall be in addition to all other penalties and/or interest other wise imposed. For purposes of this section, there shall be a presumption that the taxpayer collected the tax from the customer or purchaser.

******************************************************************************************************************************