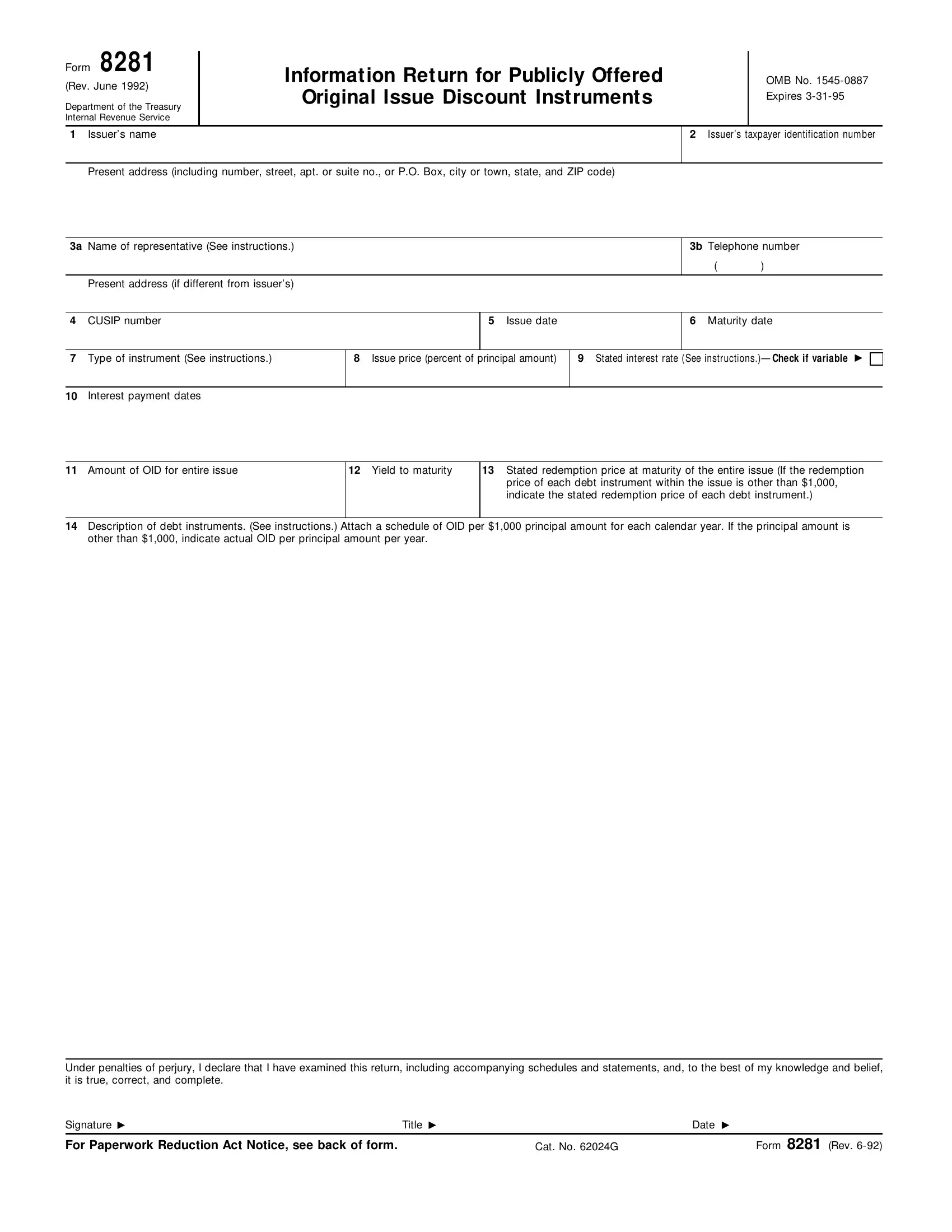

In the complex and evolving landscape of financial regulations, Form 8281, issued by the Department of the Treasury's Internal Revenue Service, plays a pivotal role for issuers of publicly offered debt instruments that carry an original issue discount (OID). This form, with its roots dating back to a revision in June 1992 and carrying an OMB number of 1545-0887, serves as an information return that these issuers are required to file. Detailed within are sections that cover various aspects of the debt instrument, including the issuer's identification, details about the representative for further correspondence, the instrument's CUSIP number, issue and maturity dates, type of instrument, issue price, stated interest rate, and importantly, the amount of OID for the entire issue. Other vital sections pertain to yield to maturity, the stated redemption price at maturity for the entire issue, and a comprehensive description of the debt instruments involved. Additional requirements include a declaration under penalties of perjury that attests to the truthfulness, correctness, and completeness of the return. The form comes with a notice relevant to the Paperwork Reduction Act, emphasizing the importance of timely and accurate submission of this information to adhere to the Internal Revenue laws of the United States. This form must be filed within 30 days of the issuance of an OID instrument, marking a critical step for issuers in ensuring compliance with federal tax regulations and contributing to the smooth execution of financial transactions in public markets.

| Question | Answer |

|---|---|

| Form Name | Form 8281 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | form 8281, tax form 8281, form 8281 pdf, 8281 form 2020 |