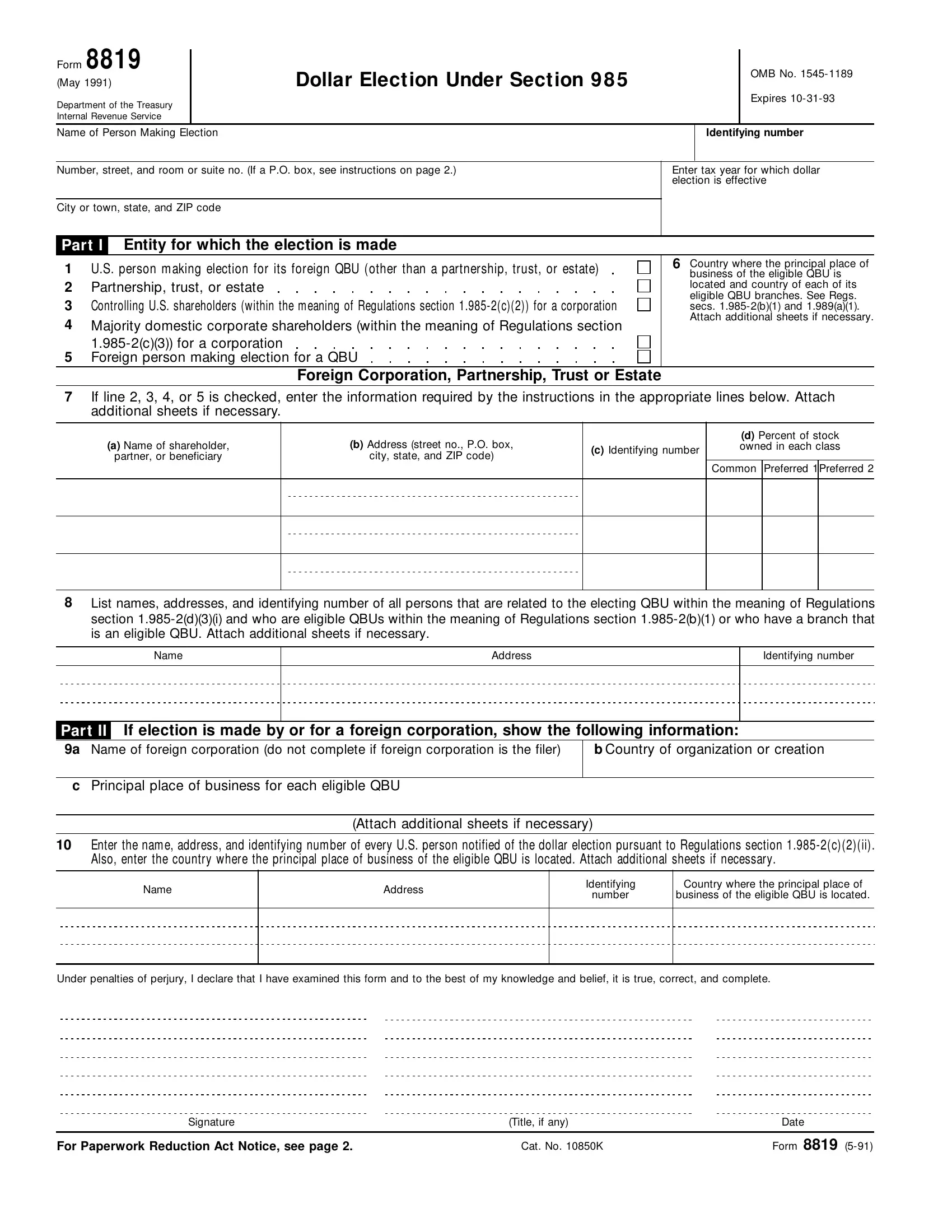

In navigating the complexities of international taxation, entities often encounter the challenge of currency fluctuations, which can significantly impact financial reporting and tax obligations. Form 8819, developed by the Department of the Treasury's Internal Revenue Service, serves as a vital tool in this context by allowing a U.S. person or entity to elect the U.S. dollar as the functional currency for a qualified business unit (QBU) operating in foreign jurisdictions. This election, permissible under Section 985 of the Internal Revenue Code, is particularly relevant for U.S. businesses with operations overseas, as well as for foreign corporations and partnerships with business activities in the United States. By filing Form 8819, these entities can stabilize their financial reporting and tax calculations, mitigating the risk posed by exchange rate volatility. The form caters to various filers, including U.S. persons making elections for their foreign QBUs, partnerships, trusts, estates, and foreign corporations, each with specific filing requirements and deadlines. Detailed instructions provided with the form guide filers through the process, ensuring compliance with U.S. tax laws while enabling a more predictable financial environment for international operations.

| Question | Answer |

|---|---|

| Form Name | Form 8819 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | f8819 1991 form 8819 irs |