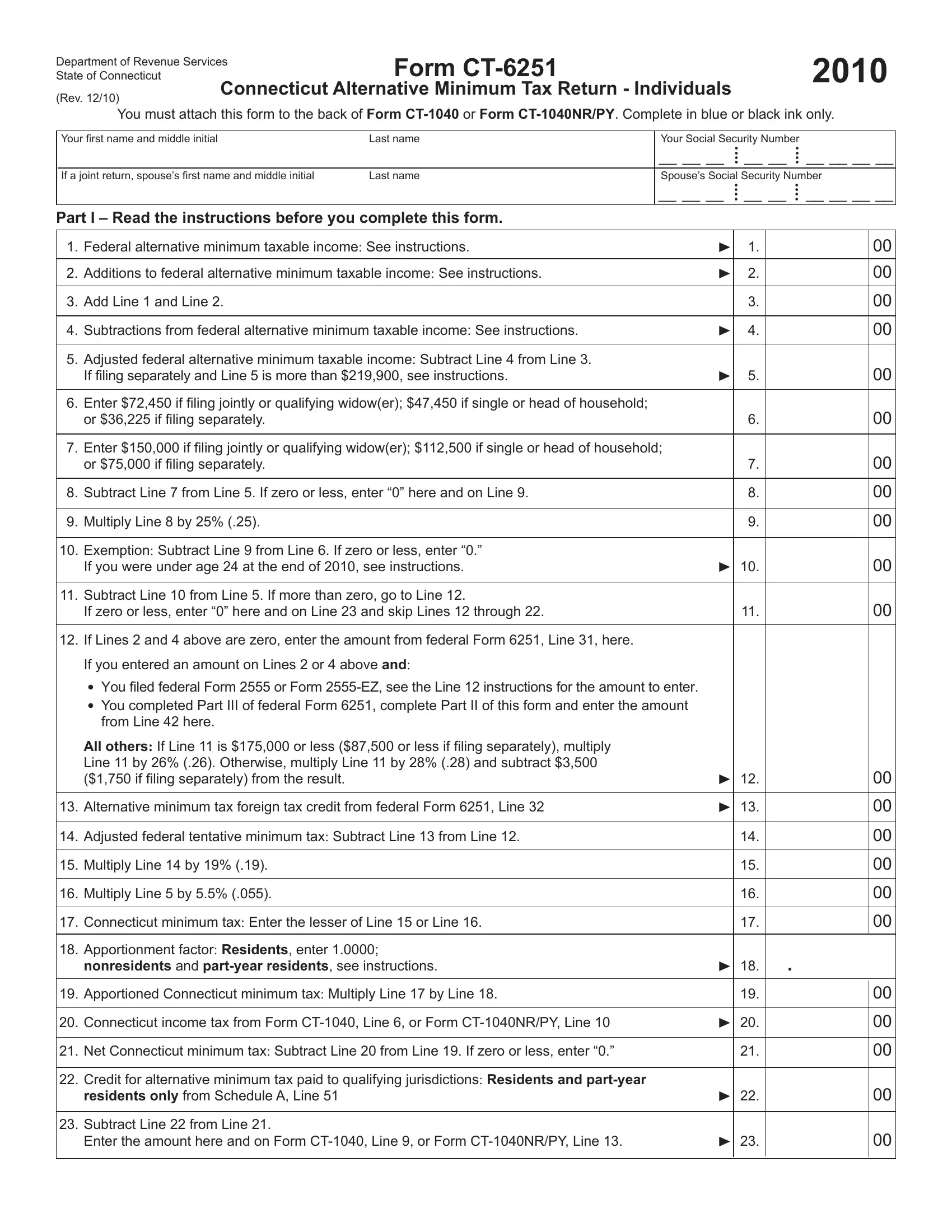

The Form CT-6251, known as the Connecticut Alternative Minimum Tax Return for Individuals, serves a vital role in ensuring that taxpayers with certain types of income and deductions pay at least a minimum amount of state tax, thereby promoting tax equity. Drafted by the Department of Revenue Services for the State of Connecticut, this document is designed for integration with either Form CT-1040 or Form CT-1040NR/PY, necessitating its attachment to the back of one's standard tax return. It emphasizes thorough instructions for recalculating federal alternative minimum taxable income with adjustments specific to Connecticut, accounting for additions and subtractions not captured by federal tax calculations. The form is meticulously structured into parts where taxpayers first determine their federal alternative minimum taxable income and then make necessary state-specific adjustments. These adjustments include various additions to or subtractions from the federal amount to arrive at the adjusted federal alternative minimum taxable income, the cornerstone for computing the Connecticut alternative minimum tax. Eligibility criteria necessitate that individuals with a federal alternative minimum tax liability, whether residents, part-year residents, or nonresidents earning within Connecticut, must file this form. Furthermore, the document outlines detailed directives on calculating apportionment for nonresidents and part-year residents, along with specifying credits available for taxes paid to other jurisdictions. This paper not only elucidates the mechanics of the Connecticut alternative minimum tax calculation but also guides taxpayers through the complexities of aligning federal alternative minimum taxable income with Connecticut’s specific adjustments, emphasizing the state’s unique considerations.

| Question | Answer |

|---|---|

| Form Name | Form Ct 6251 |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | 2555-EZ, CT-6251, CT-1040, 2018 form ct 6251 |

Department of Revenue Services |

Form |

2010 |

|

State of Connecticut |

|

||

(Rev. 12/10) |

Connecticut Alternative Minimum Tax Return - Individuals |

|

|

|

|

|

|

You must attach this form to the back of Form

Your fi rst name and middle initial |

Last name |

Your Social Security Number |

|

|||

|

|

__ __ __ |

• |

__ __ |

• |

__ __ __ __ |

|

|

••• |

••• |

|||

If a joint return, spouse’s fi rst name and middle initial |

Last name |

Spouse’s Social Security Number |

||||

|

|

__ __ __ |

• |

__ __ |

• |

__ __ __ __ |

|

|

••• |

••• |

|||

Part I – Read the instructions before you complete this form.

1. |

Federal alternative minimum taxable income: See instructions. |

|

1. |

|

00 |

|

|

|

|

|

|

2. |

Additions to federal alternative minimum taxable income: See instructions. |

|

2. |

|

00 |

|

|

|

|

|

|

3. |

Add Line 1 and Line 2. |

|

3. |

|

00 |

|

|

|

|

|

|

4. |

Subtractions from federal alternative minimum taxable income: See instructions. |

|

4. |

|

00 |

|

|

|

|

|

|

5. |

Adjusted federal alternative minimum taxable income: Subtract Line 4 from Line 3. |

|

|

|

|

|

If filing separately and Line 5 is more than $219,900, see instructions. |

|

5. |

|

00 |

|

|

|

|

|

|

6. |

Enter $72,450 if fi ling jointly or qualifying widow(er); $47,450 if single or head of household; |

|

|

|

|

|

or $36,225 if fi ling separately. |

|

6. |

|

00 |

|

|

|

|

|

|

7. |

Enter $150,000 if fi ling jointly or qualifying widow(er); $112,500 if single or head of household; |

|

|

|

|

|

or $75,000 if fi ling separately. |

|

7. |

|

00 |

|

|

|

|

|

|

8. |

Subtract Line 7 from Line 5. If zero or less, enter “0” here and on Line 9. |

|

8. |

|

00 |

|

|

|

|

|

|

9. |

Multiply Line 8 by 25% (.25). |

|

9. |

|

00 |

|

|

|

|

|

|

10. Exemption: Subtract Line 9 from Line 6. If zero or less, enter “0.” |

|

|

|

|

|

|

If you were under age 24 at the end of 2010, see instructions. |

10. |

|

00 |

|

|

|

|

|

|

|

11. |

Subtract Line 10 from Line 5. If more than zero, go to Line 12. |

|

|

|

|

|

If zero or less, enter “0” here and on Line 23 and skip Lines 12 through 22. |

|

11. |

|

00 |

|

|

|

|

|

|

12. |

If Lines 2 and 4 above are zero, enter the amount from federal Form 6251, Line 31, here. |

|

|

|

|

|

If you entered an amount on Lines 2 or 4 above and: |

|

|

|

|

|

You filed federal Form 2555 or Form |

|

|

|

|

|

You completed Part III of federal Form 6251, complete Part II of this form and enter the amount |

|

|

|

|

|

from Line 42 here. |

|

|

|

|

|

All others: If Line 11 is $175,000 or less ($87,500 or less if fi ling separately), multiply |

|

|

|

|

|

Line 11 by 26% (.26). Otherwise, multiply Line 11 by 28% (.28) and subtract $3,500 |

|

|

|

|

|

($1,750 if fi ling separately) from the result. |

12. |

|

00 |

|

|

|

|

|

|

|

13. Alternative minimum tax foreign tax credit from federal Form 6251, Line 32 |

13. |

|

00 |

||

|

|

|

|

|

|

14. Adjusted federal tentative minimum tax: Subtract Line 13 from Line 12. |

|

14. |

|

00 |

|

|

|

|

|

|

|

15. Multiply Line 14 by 19% (.19). |

|

15. |

|

00 |

|

|

|

|

|

|

|

16. Multiply Line 5 by 5.5% (.055). |

|

16. |

|

00 |

|

|

|

|

|

|

|

17. Connecticut minimum tax: Enter the lesser of Line 15 or Line 16. |

|

17. |

|

00 |

|

|

|

|

|

|

|

18. Apportionment factor: Residents, enter 1.0000; |

|

|

. |

|

|

|

nonresidents and |

18. |

|

||

|

|

|

|

||

19. Apportioned Connecticut minimum tax: Multiply Line 17 by Line 18. |

|

19. |

|

00 |

|

|

|

|

|

|

|

20. Connecticut income tax from Form |

20. |

|

00 |

||

|

|

|

|

|

|

21. Net Connecticut minimum tax: Subtract Line 20 from Line 19. If zero or less, enter “0.” |

|

21. |

|

00 |

|

|

|

|

|

|

|

22. Credit for alternative minimum tax paid to qualifying jurisdictions: Residents and |

|

|

|

|

|

|

residents only from Schedule A, Line 51 |

22. |

|

00 |

|

|

|

|

|

|

|

23. Subtract Line 22 from Line 21. |

|

|

|

|

|

|

Enter the amount here and on Form |

23. |

|

00 |

|

|

|

|

|

|

|

Part II

24. |

Enter the amount from Line 11. If you are fi ling federal Form 2555 or Form |

|

|

|

|

|||

|

from Line 3 of the Connecticut Foreign Earned Income Tax Worksheet on Page 4. |

|

|

|

|

24. |

|

00 |

|

|

|

|

|

|

|

|

|

25. |

Enter the amount from federal Form 6251, Line 37. See instructions. |

|

25. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

26. |

Enter the amount from federal Form 6251, Line 38. See instructions. |

|

26. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

27. |

Enter the amount from federal Form 6251, Line 39. See instructions. |

|

27. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

28. |

Enter the smaller of Line 24 or Line 27. |

|

|

|

|

28. |

|

00 |

|

|

|

|

|

|

|

|

|

29. |

Subtract Line 28 from Line 24. |

|

|

|

|

29. |

|

00 |

|

|

|

|

|

|

|

|

|

30. |

If Line 29 is $175,000 or less ($87,500 or less if fi ling separately), multiply Line 29 by 26% (.26). |

|

|

|

|

|||

|

Otherwise, multiply Line 29 by 28% (.28) and subtract $3,500 ($1,750 if fi ling separately) from the result. |

|

30. |

|

00 |

|||

|

|

|

|

|

|

|

|

|

31. |

Enter: |

|

|

|

|

|

|

|

|

$68,000, if fi ling jointly or qualifying widow(er); |

|

|

|

|

|

|

|

|

$34,000, if single or filing separately; or |

|

|

|

|

|

|

|

|

$45,550, if head of household. |

|

31. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

32. |

Enter the amount from federal Form 6251, Line 44. See instructions. |

|

32. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

33. |

Subtract Line 32 from Line 31. If zero or less, enter “0.” |

|

33. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

34. |

Enter the smaller of Line 24 or Line 25. |

|

34. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

35. |

Enter the smaller of Line 33 or Line 34. |

|

35. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

36. |

Subtract Line 35 from Line 34. |

|

36. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

37. |

Multiply Line 36 by 15% (.15). |

|

|

|

|

|

|

|

|

If Line 26 is zero or blank, skip Lines 38 and 39 and go to Line 40. Otherwise, go to Line 38. |

|

37. |

|

00 |

|||

|

|

|

|

|

|

|

|

|

38. |

Subtract Line 34 from Line 28. |

|

38. |

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

39. |

Multiply Line 38 by 25% (.25). |

|

|

|

|

39. |

|

00 |

|

|

|

|

|

|

|

|

|

40. |

Add Lines 30, 37 and 39. |

|

|

|

|

40. |

|

00 |

|

|

|

|

|

|

|

||

41. |

If Line 24 is $175,000 or less ($87,500 or less if fi ling separately), multiply Line 24 by 26% (.26). |

|

|

|

|

|||

|

Otherwise, multiply Line 24 by 28% (.28) and subtract $3,500 ($1,750 if fi ling separately) from the result. |

|

41. |

|

00 |

|||

|

|

|

|

|

|

|||

42. |

Enter the smaller of Line 40 or Line 41 here and on Line 12. If you are fi ling federal Form 2555 or Form |

|

|

|

||||

|

do not enter this amount on Line 12. Enter it on Line 4 of the Connecticut Foreign Earned Income Worksheet |

|

|

|

|

|||

|

on Page 4 of the instructions. |

|

|

|

|

42. |

|

00 |

|

|

|

|

|

|

|

|

|

Form |

Page 2 of 6 |

General Instructions

Purpose

Taxpayers who are subject to and required to pay the federal alternative minimum tax are subject to the Connecticut alternative minimum tax. Use this form to calculate your Connecticut alternative minimum tax liability and attach it directly behind your Connecticut income tax return.

Taxpayers who do not have a federal alternative minimum tax liability are not required to complete this form.

Who Must File This Form

You are required to file Form

You were a Connecticut resident or

You were a Connecticut nonresident with a federal alternative minimum tax liability and you had

If you meet one of the requirements above, you must file Form

What Is the Connecticut Alternative Minimum Tax

The Connecticut alternative minimum tax is a tax imposed on certain individuals, trusts, and estates in addition to their regular income tax. The tax is computed on the lesser of 19% of the adjusted federal tentative minimum tax or 5.5% of the adjusted federal alternative minimum taxable income.

What Is the Adjusted Federal Tentative Minimum Tax

The adjusted federal tentative minimum tax is your federal tentative minimum tax with certain Connecticut modifications.

Connecticut

Credits

Connecticut residents and

You may be able to claim a credit against your Connecticut income tax for Connecticut alternative minimum tax paid in a prior year. See the instructions to Form

Filing Status

Your filing status on Form

Any reference in these instructions to filing jointly includes filing jointly for federal and Connecticut and filing jointly for Connecticut only. Likewise, filing separately includes filing separately for federal and Connecticut and fi ling separately for Connecticut only.

Generally, your filing status for Connecticut income tax purposes must match your federal income tax filing status for the year. However, if you are a civil union partner or a spouse in a marriage recognized under Public Act

For more information, see Spouses With Different Residency Status in the instructions to Form

If you and your spouse are filing a joint federal income tax return and you file separate Connecticut income tax returns, either because you qualify and elect to do so or because you are required to do so, the federal rules for allocating income apply. You must recalculate your federal alternative minimum tax liability as if your filing status for federal income tax purposes was single. If upon your recalculation you would have had a federal alternative minimum tax liability, you are subject to Connecticut alternative minimum tax and you are required to calculate Form

Where the calculation of any individual federal items are subject to limitations (for example, alternative tax net operating loss deduction); the items may have to be recalculated if Connecticut modifications apply.

Line Instructions

Name and Social Security Number

Enter your name and Social Security Number (SSN) as it appears on your Connecticut income tax return in the space provided at the top of the form. If you are filing a joint return, also enter your spouse’s name and SSN.

Part I

Line 1

Residents,

If your filing status is filing separately for Connecticut only, recalculate your federal 6251 using only your share of Lines 1 through 27 from federal Form 6251 and enter the result here. This amount may differ from the amount entered on federal Form 6251, Line 28.

Line 2

To compute the additions to federal alternative minimum taxable income, use the amount entered on Form

•Any modification for a taxable

•Any interest or dividend income on U.S. government obligations or securities exempt from federal income tax, but taxable for Connecticut income tax purposes, to the extent included on Form

Exclude from Line 2 the amount of federally

Form |

Page 3 of 6 |

Line 4

To compute the subtractions from federal alternative minimum taxable income, use the total amount entered on Form

Any modification for refunds of state and local income taxes entered on Form

Any modification for Tier 1 Railroad Retirement Benefits and Supplemental Annuities, as entered on Form

Any modification for the amount of any distributions you received from the Connecticut Higher Education Trust (CHET) as a designated beneficiary to the extent included in your federal adjusted gross income, and to the extent included on Form

Any modification for the amount of interest earned on contributions established for a designated beneficiary under the Connecticut Homecare Option Program for the Elderly to the extent the interest is includable in the federal adjusted gross income of the designated beneficiary and to the extent included on Form

Any modification for the amount of income received from the U.S. government as retirement pay for a retired member of the Armed Forces of the United States or the National Guard to the extent included on Form

Include on Line 4 the amount of federally

Line 5

If your filing status is filing separately and Line 5 is more than $219,900, you must include an additional amount on Line 5 calculated as follows. If Line 5 is $364,800 or more, include an additional $36,225 on Line 5. Otherwise, include 25% of the excess of the amount on Line 5 over $219,900.

Example: If the amount on Line 5 is $239,900, multiply the amount in excess of $219,900 ($20,000) by 25% (.25). The result is $5,000. Add the $5,000 to $239,900 and enter $244,900 on Line 5.

Line 10

If you were under age 24 at the end of 2010, follow the instructions to federal Form 6251, Line 29, to calculate the exemption amount.

Line 12

If Line 2 or Line 4 of Form

Line 18

Residents: Must enter 1.0000.

Nonresidents and

To determine the total items of income, gain, loss, or deduction from Connecticut sources, you must net out certain modifications that may have been included in the amount shown on Form

You must further adjust the amount from Form

Part II

If you completed Part III of federal Form 6251, complete Part II and enter the amount from Form

Lines 25, 26, 27, and 32

When entering an amount on Lines 25, 26, 27, and 32, you must include the Schedule 1 modification for the gain or loss on the sale of Connecticut state and local government bonds from Form

Connecticut Foreign Earned Income Tax Worksheet

1. |

Enter the amount from Form |

1. _____________ |

2. |

Enter the amount from your (and your spouse’s if filing jointly) |

|

|

federal Form 2555, Lines 45 and 50, or federal Form |

2. _____________ |

3. |

Add Line 1 and Line 2 |

3. _____________ |

4. |

Tax amount on Line 3. |

|

|

• If you completed Part III of federal Form 6251, you must complete Part II of Form |

|

|

Line 3 of this worksheet on Part II, Line 24, of Form |

|

|

enter the amount from Line 42 here. |

|

|

• All others: If line 3 is $175,000 or less ($87,500 or less if fi ling separately), multiply Line 3 by 26% (.26). |

|

|

Otherwise, multiply Line 3 by 28% (.28) and subtract $3,500 ($1,750, if fi ling separately) from the result |

4. _____________ |

5. |

Tax on amount on Line 2. If Line 2 is $175,000 or less ($87,500 or less if fi ling separately), multiply Line 2 by 26% (.26). |

|

|

Otherwise, multiply Line 2 by 28% (.28) and subtract $3,500 ($1,750, if fi ling separately) from the result |

5. _____________ |

6. |

Subtract Line 5 from Line 4. Enter here and on Form |

6. _____________ |

|

|

|

Form |

Page 4 of 6 |

Schedule A

Credit for Alternative Minimum Tax Paid to Qualifying Jurisdictions

Connecticut Residents and

Residents

Use Schedule A to claim a credit against the net Connecticut minimum tax liability for alternative minimum tax paid during the taxable year to a qualifying jurisdiction. Credit may be claimed only if the income on which taxes were paid was derived from or connected with sources within the qualifying jurisdiction.

Use Schedule A to claim a credit against the net Connecticut minimum tax liability for alternative minimum tax paid to a qualifying jurisdiction on items of income, gain, loss, or deduction attributable to that jurisdiction during the period of Connecticut residency.

A qualifying jurisdiction includes another state of the United States, a local government within another state, or the District of Columbia. A qualifying jurisdiction does not include the State of Connecticut, the United States, or a foreign country or its provinces (for example, Canada and Canadian provinces).

No credit is allowed for any of the following:

Alternative minimum tax paid to a qualifying jurisdiction on income not derived from or connected with sources within the qualifying jurisdiction;

Alternative minimum tax paid to a jurisdiction that is not a qualifying jurisdiction;

Alternative minimum tax paid to a qualifying jurisdiction, if you claimed credit for alternative minimum tax paid to Connecticut on that qualifying jurisdiction’s alternative minimum tax return or income tax return; or

Payments of alternative minimum tax made to a qualifying jurisdiction on income not subject to the Connecticut alternative minimum tax.

No credit is allowed for tax paid on dividends or interest income unless derived from property employed in a business or trade carried on in that jurisdiction. However, credit is allowed for tax paid on wages earned for services performed in a qualifying jurisdiction.

The allowed credit must be separately computed for each qualifying jurisdiction. Use separate columns for each qualifying jurisdiction for which you are claiming a credit. Attach a copy of all alternative minimum tax returns filed with qualifying jurisdictions directly following Form

Schedule A provides two columns, A and B, to compute the credit for two qualifying jurisdictions. If you need more than two columns, create a worksheet identical to Schedule A and attach it to the back of your Form

If you are claiming credit for alternative minimum tax paid to a qualifying jurisdiction and to one of its political subdivisions, follow these rules to determine your credit.

A.If the same amount of adjusted alternative minimum taxable income is taxed by both the city and the state:

1.Use only one column of Schedule A to calculate your credit;

2.Enter the same amount of adjusted alternative minimum taxable income taxed by both city and state in that column on Form

3.Combine the amounts of alternative minimum tax paid to the city and the state and enter the total on Line 51 of that column.

B.If the amounts of adjusted alternative minimum taxable income taxed by both the city and state are not the same:

1.Use two columns on Form

2.Include only the same amount of adjusted alternative minimum taxable income taxed by both jurisdictions in the first column; and

3.Include the excess amount of adjusted alternative minimum taxable income taxed by only one of the jurisdictions in the next column.

Attach a copy of the alternative minimum tax return fi led with each qualifying jurisdiction to the back of your Form

Form |

Page 5 of 6 |

Form

Schedule A - Credit for Alternative Minimum Tax Paid to Qualifying Jurisdictions

You must attach a copy of your return fi led with the qualifying jurisdiction(s) or your credit will be disallowed.

43. Modified adjusted federal alternative minimum taxable income: See instructions.

43.

00

|

|

Column A |

|

|

Column B |

|

|

For each column, enter the following: |

|

Name |

Code |

Name |

Code |

||

44. Enter qualifying jurisdiction’s name and |

44. |

|

|

|

|

|

|

45. Enter the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

minimum taxable income included on Line 43 which is |

|

|

|

00 |

|

|

00 |

subject to a qualifying jurisdiction’s alternative minimum tax. |

45. |

|

|

|

|

||

|

|

|

|

|

|

|

|

46. Divide Line 45 by Line 43. Round to four decimal places. |

46. |

• |

|

|

• |

|

|

47. Enter the net Connecticut minimum tax (from Form |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

00 |

|

Line 21). |

47. |

|

|

|

|

||

48. Multiply Line 46 by Line 47. |

48. |

|

|

00 |

|

|

00 |

49. Alternative minimum tax paid to a qualifying jurisdiction: See instructions. |

49. |

|

|

00 |

|

|

00 |

50. Enter the lesser of Line 48 or Line 49. |

50. |

|

|

00 |

|

|

00 |

|

|

|

|

|

|

|

|

51. Total credit: Add Line 50, all columns. Enter amount here and on Line 22 on the front of this form. |

51. |

|

|

00 |

|||

If you claim credit for alternative minimum tax paid to another state of the United States, a political subdivision within another state, or the District of Columbia, enter the appropriate

Line Instructions

Line 43

Residents: Enter the amount of adjusted federal alternative minimum taxable income from Form

Line 44

Enter the name and the

Line 45

Enter the amount of the adjusted federal alternative minimum taxable income included on Line 43 subject to a qualifying jurisdiction’s alternative minimum tax.

Line 48

Multiply the percentage arrived at on Line 46 by the amount reported on Line 47.

Line 49

Residents: Enter the total amount of alternative minimum tax paid to a qualifying jurisdiction.

If the alternative minimum tax paid to that jurisdiction was also based on income earned during the nonresidency portion of your taxable year, you must prorate the amount of tax for which you are claiming credit. The proration is based upon the relationship that the income earned in that jurisdiction during your Connecticut residency bears to the total amount of income that you earned in that jurisdiction in the taxable year.

Alternative minimum tax paid means the lesser of your tax liability to the qualifying jurisdiction or the tax you paid to that jurisdiction as reported on a return filed with that jurisdiction, but not any penalty or interest.

Line 46

Divide the amount on Line 45 by the amount on Line 43. The result may not exceed 1.0000. Round to four decimal places.

Line 47

Residents: Enter the amount from Form

Line 50

Enter the lesser of the amounts reported on Line 48 or Line 49.

Line 51

Add the amounts from Lines 50A, 50B, and 50 of any additional worksheets. The amount on Line 51 cannot exceed the total of Line 48. Enter the total on Line 51 and on Line 22.

Form |

Page 6 of 6 |