Navigating the complexities of tax obligations after the repossession of tangible personal property is a crucial task for businesses to ensure they are in compliance with state regulations and to safeguard their financial interests. The Dr 95B form plays a pivotal role in this process, serving as a detailed schedule for claiming tax credits or refunds on such repossessed properties in Florida. This form is specifically designed to assist businesses in calculating the due amount of tax credit or refund based on the sales tax and any applicable discretionary sales surtax previously paid to the Florida Department of Revenue. Required to be filed within 12 months following the repossession of the property, the form mandates accurate documentation of the customer's information, property description, the taxes paid, and the financial arrangement details leading up to the repossession. Its structured approach helps clarify the obligations of businesses that sell tangible personal property under various financing contracts and subsequently repossess it due to default. Moreover, it outlines the steps for claiming the tax credit or refund, whether through a Sales and Use Tax Return or an Application for Refund – Sales and Use Tax, thereby providing a clear procedural pathway. Insight into this form is not just about adhering to the legal framework; it’s about understanding the lifeline it offers to businesses in recouping some of their losses from defaulted agreements.

| Question | Answer |

|---|---|

| Form Name | Form Dr 95B |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | dr 95b, use tax claimed, florida schedule sales, form dr 95b |

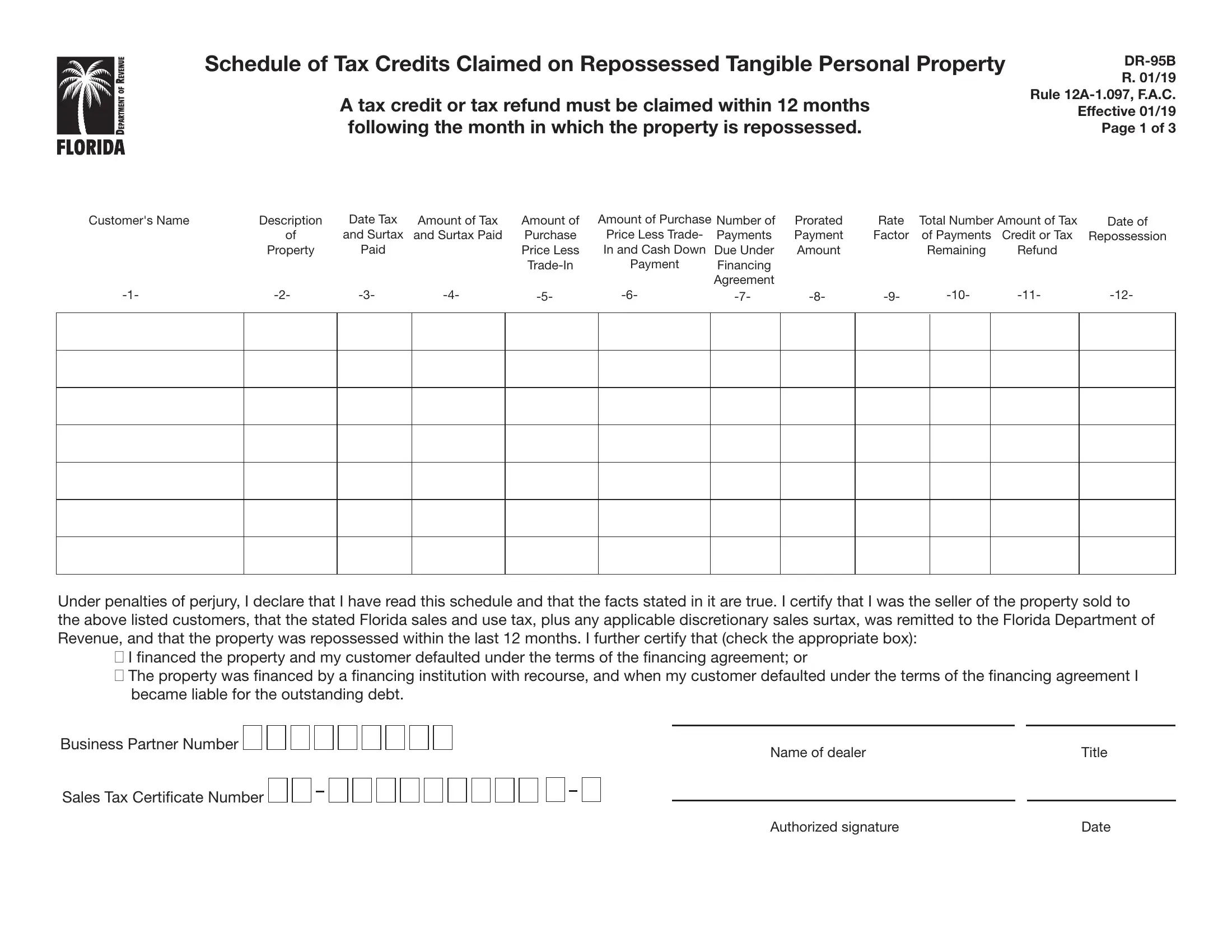

Schedule of Tax Credits Claimed on Repossessed Tangible Personal Property

A tax credit or tax refund must be claimed within 12 months following the month in which the property is repossessed.

R. 01/19

Rule

Effective 01/19

Page 1 of 3

Customer's Name |

Description |

Date Tax |

Amount of Tax |

Amount of |

Amount of Purchase Number of |

Prorated |

Rate |

Total Number Amount of Tax |

Date of |

||||

|

of |

and Surtax |

and Surtax Paid |

Purchase |

Price Less Trade- |

Payments |

Payment |

Factor |

of Payments |

Credit or Tax |

Repossession |

||

|

Property |

Paid |

|

Price Less |

In and Cash Down |

Due Under |

Amount |

|

Remaining |

Refund |

|

||

|

|

|

|

Payment |

Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Agreement |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have read this schedule and that the facts stated in it are true. I certify that I was the seller of the property sold to the above listed customers, that the stated Florida sales and use tax, plus any applicable discretionary sales surtax, was remitted to the Florida Department of Revenue, and that the property was repossessed within the last 12 months. I further certify that (check the appropriate box):

I financed the property and my customer defaulted under the terms of the financing agreement; or

The property was financed by a financing institution with recourse, and when my customer defaulted under the terms of the financing agreement I became liable for the outstanding debt.

Business Partner Number |

Name of dealer |

Title |

|

Sales Tax Certificate Number

Authorized signature |

Date |

Instructions

R.01/19 Page 2 of 3

Any business registered with the Florida Department of Revenue as a sales and use tax dealer may use Form

•sells tangible personal property under a retail installment, title loan, conditional sale, contract with a retention of title provision, or similar financing contract;

•retains a security interest in the property that was sold (through a financing agreement entered into directly with the purchaser or, when financed by a financing institution, the business becomes liable for the outstanding debt at the time of repossession);

•paid sales tax, plus applicable discretionary sales surtax, on the sales price of the property to the Florida Department of Revenue; and

•repossesses the financed property.

The amount of tax credit or tax refund due is based on the ratio that the total tax has in relation to the unpaid balance of the sales price, excluding finance or other nontaxable charges. A tax credit or tax refund must be claimed within 12 months following the month in which the property is repossessed.

The registered business that paid the tax and applicable surtax to the Department may claim a credit on a Sales and Use Tax Return (Form

Column by Column Instructions

Column 1. Customer’s Name

Enter the name of each customer from whom financed tangible personal property was repossessed.

Column 2. Description of Property

Enter a description of each item of tangible personal titled property listed. For motor vehicles, boats, and aircraft, include the year, make, model number, and the VIN, serial, or hull number.

Column 3. Date Tax and Surtax Paid

Enter the date the sales and use tax, plus any applicable discretionary sales surtax, was paid to the Florida Department of Revenue on each item of property listed.

Column 4. Amount of Tax and Surtax Paid

Enter the amount of sales tax and surtax paid on each

item listed. Do not include any amount contributed by the purchaser of a motor vehicle to a participating nonprofit

Column 5. Amount of Purchase Price Less

Enter the sales price of each item listed, less any trade- in credit taken at the time of sale. Include all charges subject to sales and use tax, plus any applicable discretionary sales surtax, at the time of sales. Do not include nontaxable charges, such as interest or penalty charges.

Column 6. Amount of Purchase Price Less

For each item listed, enter the sales price less the amount of any

Column 7. Number of Payments Due Under Financing

Agreement

For each item listed, enter the total number of payments due under the retail installment, title loan, conditional sale, contract with a retention of title provision, or similar financing contract for the item purchased.

Column 8. Prorated Payment Amount

For each item listed, divide the amount in Column 6 by the amount in Column 7 to calculate the prorated payment for the item. Enter the result in Column 8.

Column 9. Rate Factor

For each item listed, divide the amount in Column 4 by the amount in Column 5 to calculate the sales and use tax and surtax rate at time of purchase. Enter the calculated rate in Column 9.

Column 10. Total Number of Payments Remaining

For each item listed, subtract any late penalties paid on the account from the total amount paid on the account. Divide the result by the amount of the monthly payment due under the financing contract (amount due when paid timely). Subtract the calculated number from the total number of payments due under the financing agreement to calculate the number of payments remaining due. Enter the result in Column 10.

Column 11. Amount of Tax Credit or Tax Refund

For each item listed, multiply the number in Column 8 by Column 9 by Column 10 and enter the result in Column

11.This amount is the amount of tax credit or tax refund due on the repossessed item.

Column 12. Date of Repossession

For each item listed, enter the date (day, month, and year) the property was repossessed.

R. 01/19

Page 3 of 3

CONTACT US

Information, forms, and tutorials are available on the Department’s website at floridarevenue.com .

To speak with a Department representative, call Taxpayer Services at

To find a taxpayer service center near you, visit floridarevenue.com/taxes/servicecenters .

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Updates by Email from the Department. Subscribe to receive an email for due date reminders, Tax Information Publications, or proposed rules. Subscribe today at floridarevenue.com/dor/subscribe .

REFERENCES

The following documents were mentioned in this form and are incorporated by reference in the rules indicated below.

The forms are available online at floridarevenue.com/forms.

Form |

Sales and Use Tax Return |

Rule |

Form |

Application for Refund – Sales and Use Tax |

Rule |