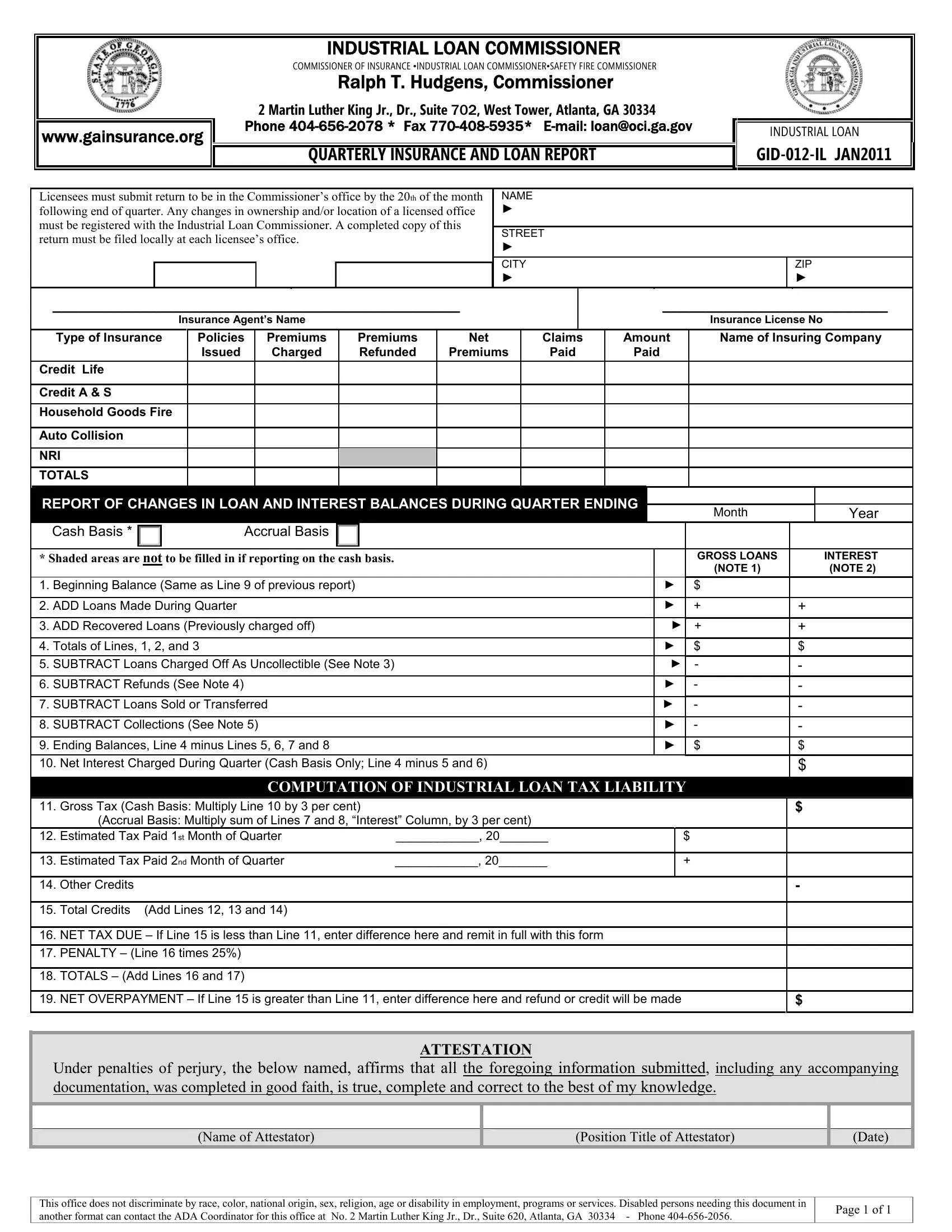

Within the structured framework of financial and insurance regulations, the GID-012-IL form serves as a critical quarterly report for licensees under the oversight of the Industrial Loan Commissioner and the Commissioner of Insurance, currently Ralph T. Hudgens. Operating from the bustling offices on Martin Luther King Jr. Drive in Atlanta, Georgia, these entities mandate the meticulous documentation of insurance and loan activities conducted by licensed operatives within the state. The form not only demands up-to-date information on any changes pertaining to ownership or office location but also encompasses detailed records spanning from insurance policies underwritten to the nuanced computations of industrial loan taxes. Equally important is the attestation section, underscoring the gravity of truth and accuracy in the submission under the penalties of perjury. Furthermore, it’s worth noting the inclusive and non-discriminatory policy echoed in the document's accessibility options, reflecting a broader commitment to equality and support for individuals with disabilities, ensuring no one is left behind in compliance processes. The form embodies a bridge between regulatory oversight and business operation, highlighting the intricate balance of transparency, accountability, and operational integrity crucial to the financial and insurance sectors.

| Question | Answer |

|---|---|

| Form Name | Form Gid 012 Il |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | GID 012 IL gid 12a il gainsurance form |