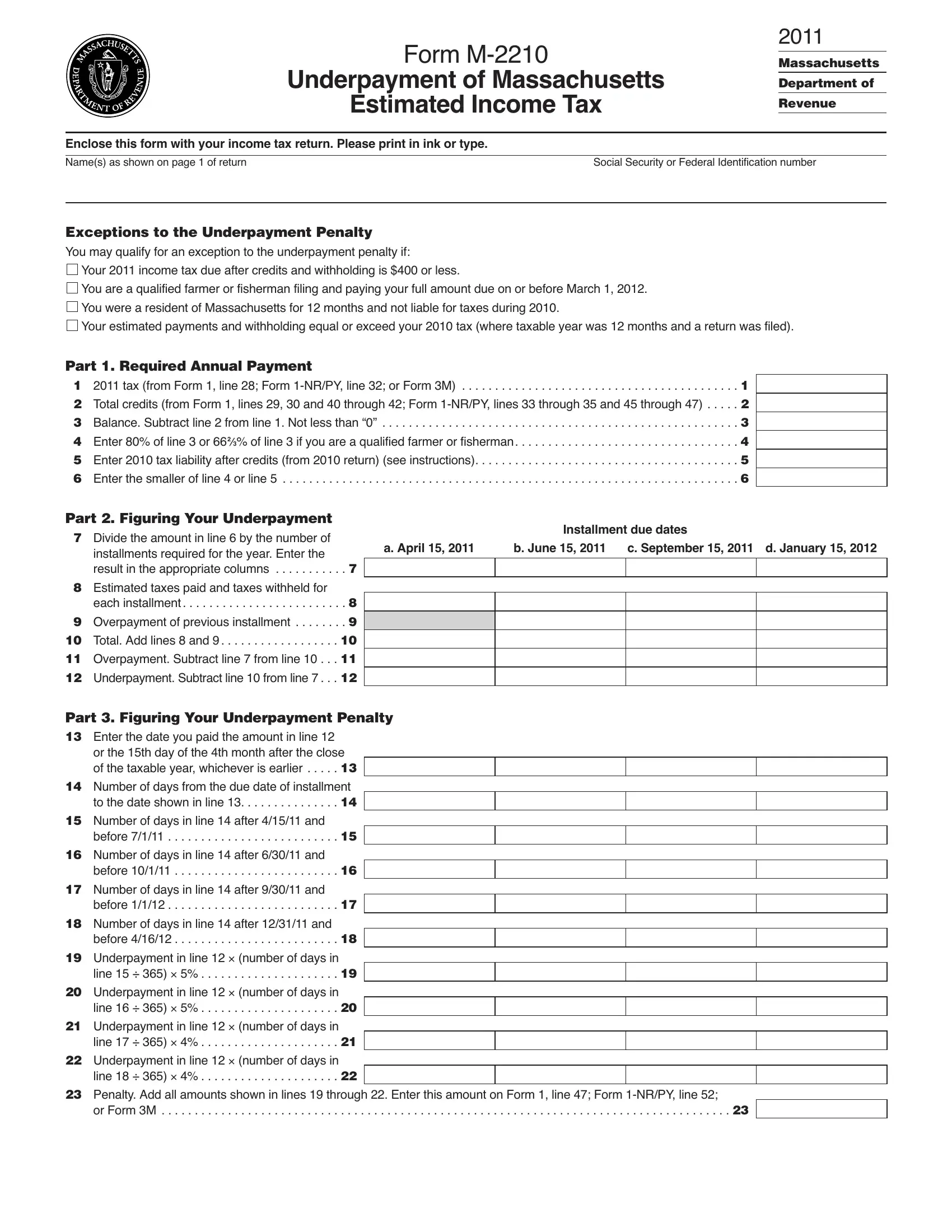

In the realm of tax compliance, navigating the intricacies of estimated payments can prove daunting for many taxpayers. The Massachusetts Department of Revenue provides Form M-2210, a crucial document designed to address the issue of underpayment of Massachusetts Estimated Income Tax for the year 2011. This form not only facilitates taxpayers in calculating any potential underpayment penalty but also outlines specific exceptions that might exempt them from such penalties. Among the noteworthy aspects of this form are the criteria defining who should use it—essentially individuals or entities taxed as individuals who have not made sufficient estimated tax payments through withholdings or direct payments. The form meticulously walks through the process, including the calculation of required annual payments, determination of underpayment, and the consequent penalty if applicable. Exemptions play a significant role, freeing certain taxpayers from penalties if conditions such as having a tax due after credits and withholding of $400 or less or being a qualified farmer or fisherman are met. Additionally, waivers might be available under circumstances like casualty, disaster, or significant life changes such as retirement or becoming disabled. For taxpayers with uneven income throughout the year, the form offers the option to adjust installment amounts using the Annualized Income Installment method, potentially mitigating or eliminating penalties. It is notable that fiscal year filers are instructed to attach a separate statement, ensuring their unique timelines are appropriately considered. This initial overview of Form M-2210 underscores its pivotal role in aiding Massachusetts taxpayers in adhering to tax payment regulations while potentially minimizing or avoiding penalties for underpayment of estimated taxes.

| Question | Answer |

|---|---|

| Form Name | Form M 2210 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | tax, massachusetts form m 2210 instructions, massachusetts form m 2210, site:mass.gov |

Form

UnderpaymentofMassachusetts

EstimatedIncomeTax

2011

Massachusetts

Department of

Revenue

Enclose this form with your income tax return. Please print in ink or type.

Name(s) as shown on page 1 of return |

Social Security or Federal Identification number |

Exceptions to the Underpayment Penalty

You may qualify for an exception to the underpayment penalty if:

Your 2011 income tax due after credits and withholding is $400 or less.

You are a qualified farmer or fisherman filing and paying your full amount due on or before March 1, 2012.

You were a resident of Massachusetts for 12 months and not liable for taxes during 2010.

Your estimated payments and withholding equal or exceed your 2010 tax (where taxable year was 12 months and a return was filed).

Part 1. Required Annual Payment

1 2011 tax (from Form 1, line 28; Form

Part 2. Figuring Your Underpayment

7 |

Divide the amount in line 6 by the number of |

|

|

Installment due dates |

||

|

a. April 15, 2011 |

b. June 15, 2011 |

c. September 15, 2011 d. January 15, 2012 |

|||

|

installments required for the year. Enter the |

|

||||

|

|

|

|

|

|

|

|

result in the appropriate columns . . . . . . . . . . . 7 |

|

|

|

|

|

8 |

Estimated taxes paid and taxes withheld for |

|

|

|

|

|

|

.each installment |

. 8 |

|

|

|

|

9 |

.Overpayment of previous installment |

. 9 |

|

|

|

|

10 |

.Total. Add lines 8 and 9 |

10 |

|

|

|

|

11 |

.Overpayment. Subtract line 7 from line 10 . . |

11 |

|

|

|

|

12 |

.Underpayment. Subtract line 10 from line 7 . . |

12 |

|

|

|

|

Part 3. Figuring Your Underpayment Penalty

13Enter the date you paid the amount in line 12 or the 15th day of the 4th month after the close

of the taxable year, whichever is earlier . . . . . 13

14Number of days from the due date of installment

to the date shown in line 13. . . . . . . . . . . . . . . 14

15Number of days in line 14 after 4/15/11 and

before 7/1/11 . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16Number of days in line 14 after 6/30/11 and

before 10/1/11 . . . . . . . . . . . . . . . . . . . . . . . . . 16

17Number of days in line 14 after 9/30/11 and

before 1/1/12 . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18Number of days in line 14 after 12/31/11 and

before 4/16/12 . . . . . . . . . . . . . . . . . . . . . . . . . 18

19Underpayment in line 12 × (number of days in

line 15 ÷ 365) × 5% . . . . . . . . . . . . . . . . . . . . . 19

20Underpayment in line 12 × (number of days in

line 16 ÷ 365) × 5% . . . . . . . . . . . . . . . . . . . . . 20

21Underpayment in line 12 × (number of days in

line 17 ÷ 365) × 4% . . . . . . . . . . . . . . . . . . . . . 21

22Underpayment in line 12 × (number of days in

line 18 ÷ 365) × 4% . . . . . . . . . . . . . . . . . . . . . 22

23Penalty. Add all amounts shown in lines 19 through 22. Enter this amount on Form 1, line 47; Form

or Form 3M . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Form

General Information

Who should use this form. If you are an individual, or a tax- payer taxed as an individual, you should use Form

Filing estimated tax vouchers. You are required to file esti- mated tax vouchers if you reasonably expect to pay more than $400 in Massachusetts income tax on income which is not covered by withholding. For further information regarding estimated taxes, see the instructions for Form

Exceptions which avoid the penalty. No underpayment penalty

will be imposed if:

1.Your 2011 tax due after credits and withholding is $400 or less.

2.You were a qualified farmer or fisherman who filed and paid in full with your return by March 1, 2012. To qualify, your gross in- come from farming or fishing must be at least

3.You were a resident of Massachusetts for the full 12 months of the previous taxable year and were not liable for taxes.

4.Your 2011 estimated payments and withholding (line 8) made on or before each installment due date in the taxable year equal or exceed the tax shown on your 2010 return divided among the four installment due dates provided that such return was for a full

If you qualify for an exception, do not complete lines 13 through

23.Instead, check the appropriate box on the front of this form and fill in the “EX” oval on the back of Form 1 or Form

Waiver of underpayment penalty. A waiver of underpayment penalty for one or more installments may be granted if:

1.Your underpayment was by reason of casualty, disaster or un- usual circumstance; or

2.You retired in 2010 or 2011 after reaching age 62, or you be- came disabled and your underpayment was due to reasonable cause and not willful neglect.

If you qualify for the waiver, complete lines 7 through 12 for the installment(s) for which you are claiming a waiver, and write “WAIVER” in the appropriate box(es) in line 13. Fill in the “EX” oval on the back of Form 1 or Form

Figuring your underpayment and penalty. To determine the underpayment amount, complete lines 1 through 12, in order of installment due dates, taking care to complete all four columns for lines 7 through 12.

Line 5

•If you filed a return for 2010 and it was for a full 12 months, enter your 2010 tax liability after credits.

•If you were a resident of Massachusetts for 12 months in 2010 and you were not liable for taxes, enter “0.”

•If you did not file a return for 2010, or if your 2010 tax year was less than 12 months, do not complete line 5. Instead, enter the amount from line 4 in line 6.

Line 8

If more than one payment is made for a given installment, attach a separate penalty computation for each payment.

If you had any taxes withheld during the year, you may apply an equal part of those taxes as payment on each required install- ment(s). If you can establish the actual dates and amounts of your withholding, you may consider those amounts as payments on the dates they were actually withheld.

Line 11

If line 11 shows an overpayment, that overpayment may be used as payment of any existing underpayment amount. Overpayments used as payments of prior underpayment amounts do not de- crease the actual underpayment amount but serve to reduce instead the period of underpayment subject to penalty. If there are no existing underpayment amounts, the overpayment is applied as a credit against the next installment.

Line 12

If line 12 shows an underpayment, see the General Information section to determine whether you qualify for an exception to, or waiver of, the underpayment penalty. If you do not qualify, con- tinue on through line 23 to determine your underpayment penalty.

Annualized income installment method. If you do not receive taxable income evenly throughout the year, you may wish to annualize your income to adjust your required installment amount(s). Enter any adjusted installment amount in the appro- priate column in line 7 and calculate any underpayment penalty from those figures. Write “ANNUALIZED” under the column in line 23. For more information on using the Annualized Income Installment method, please refer to the Massachusetts Depart- ment of Revenue’s Annualized Income Installment Worksheet, Form

Fiscal year taxpayers. If you file on a fiscal year basis and are subject to an underpayment penalty, attach a separate statement to calculate the penalty due based on the interest rate(s) in effect for the period(s) of the underpayment(s).