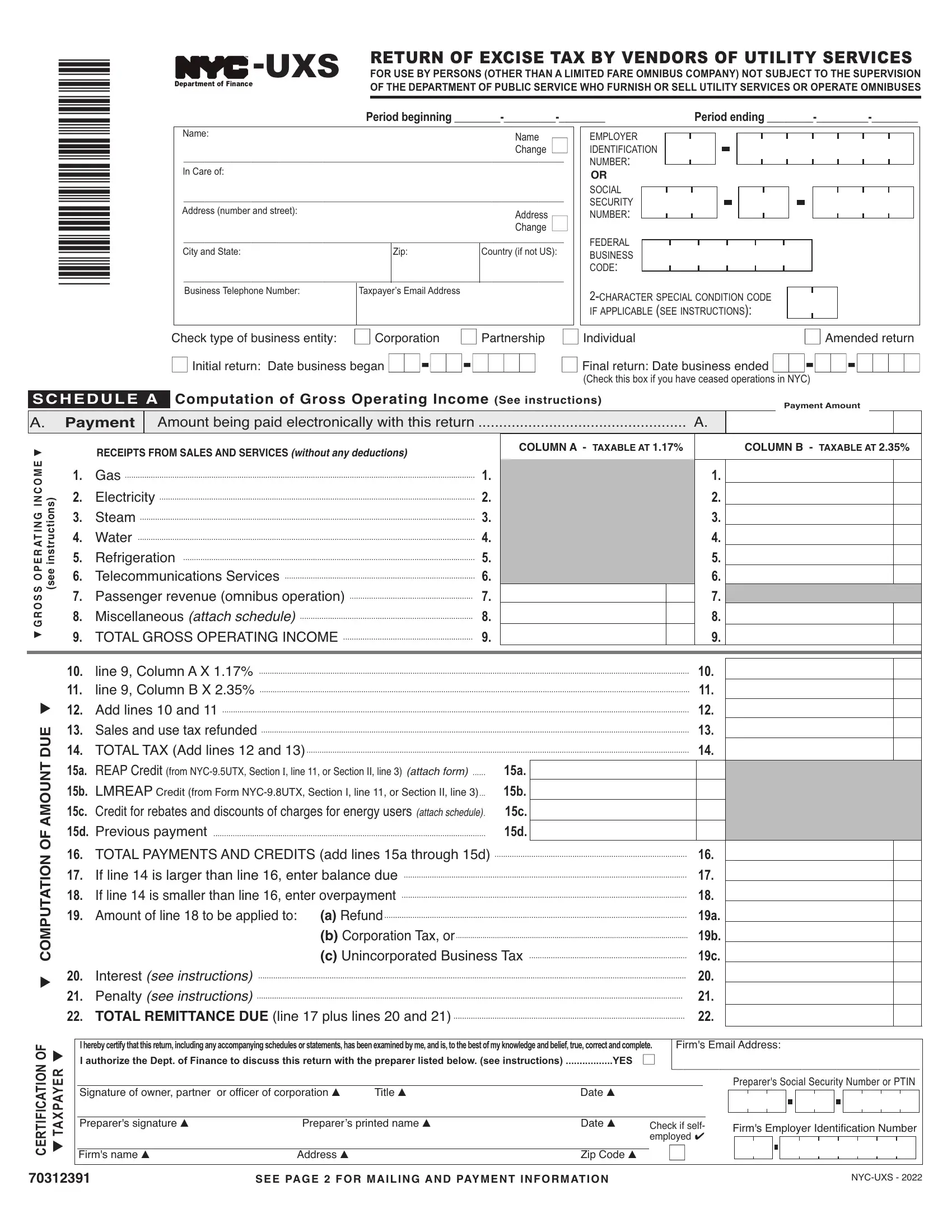

The New York City Utility Excise Tax (NYC UXS) form serves a crucial role in the regulatory landscape of utility services in NYC, primarily targeting vendors not under the Department of Public Service's supervision. This comprehensive form covers the excise tax imposed on vendors offering various utility services such as gas, electricity, steam, water, refrigeration, and telecommunications, excluding limited fare omnibus companies from its purview. The reporting period is clearly demarcated, allowing for precise tax calculations based on gross operating income derived from sales and services without any deductions. Depending on the nature of the business—be it a corporation, partnership, or individual entity—vendors must indicate the appropriate business type while also highlighting specific details such as any changes in address or ownership, and the completion of either an initial, amended, or final return. The inclusion of schedules for computing gross operating income and subsequent taxes due underscores the meticulous financial accountability required from vendors. The form also facilitates deductions, such as the REAP and LMREAP credits, reflecting a layered approach to utility tax computation. Importantly, it incorporates sections for certifying taxpayer information and delineates the payment process, emphasizing electronic payment options for efficiency. By consolidating these varied components, the NYC UXS form epitomizes the city's effort to streamline tax collection from utility vendors, ensuring a structured approach to fiscal governance within this sector.

| Question | Answer |

|---|---|

| Form Name | Form Nyc Uxs |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | Fillable Online TM UXS RETURN OF EXCISE TAX BY VENDORS OF ... |