Last month, the IRS released a draft of Form RV 066, which taxpayers would use to claim the new "residence credit" for qualified home expenses. The form is not yet final, and the IRS is currently accepting comments on it. This article will discuss the proposed form and how taxpayers can take advantage of the new residence credit. The IRS has recently released a draft of Form RV 066, which taxpayers would use to claim the new "residence credit" for qualified home expenses. The form is not yet final, so taxpayers are invited to provide feedback to the IRS during this comment period. This article will discuss the proposed form and how taxpayers can benefit from taking advantage of this new residence credit. Stay tuned for updates as we learn more about this exciting development!

| Question | Answer |

|---|---|

| Form Name | Form Rv 066 |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | ResaleCertifica te SDc sd resale certificate form |

Revised 07/03

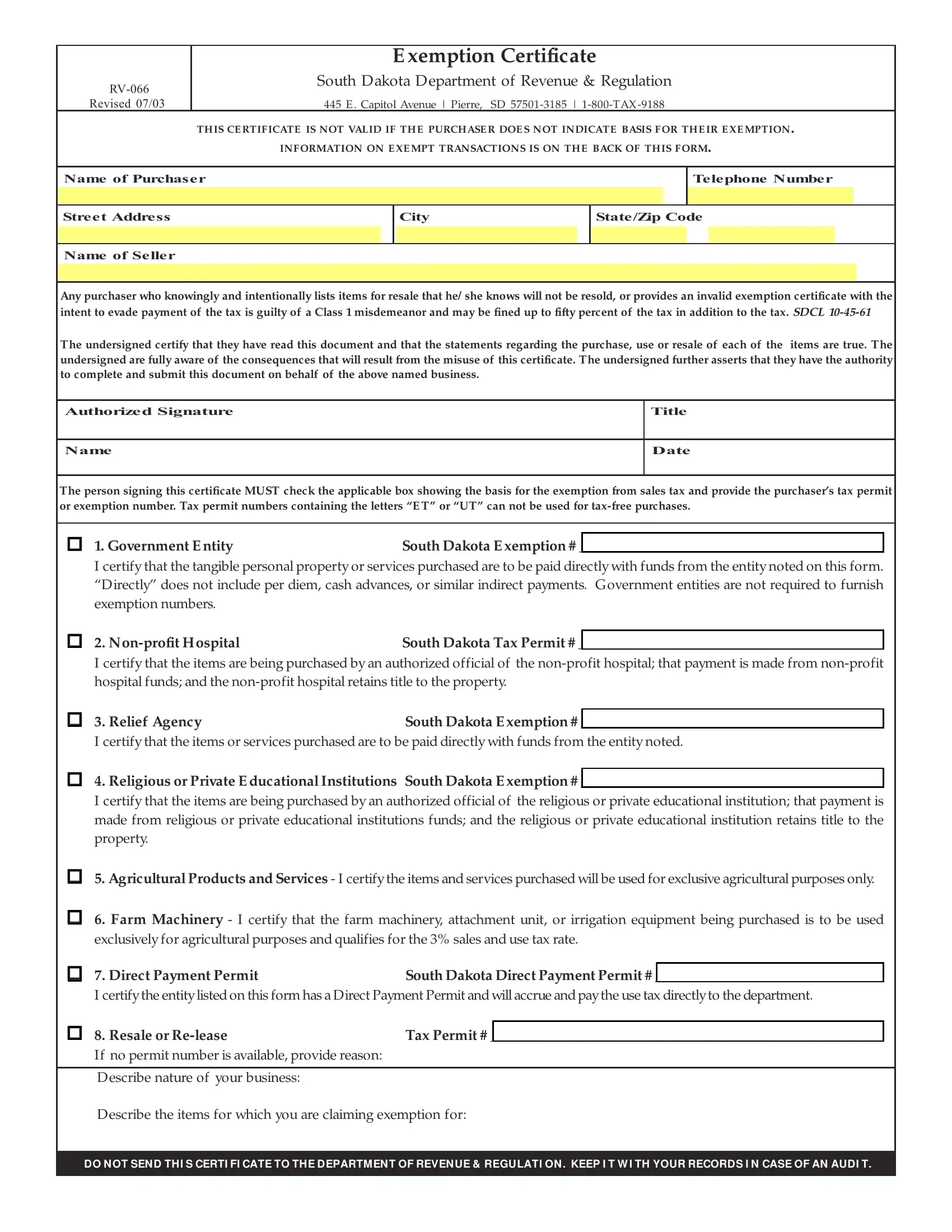

E xemption Certificate

South D akota D epartment of Revenue & Regulation

445 E . Capitol Avenue | Pierre, SD

TH IS CE RTIF ICATE IS NOT VALID IF TH E PURCH ASE R DOE S NOT INDICATE BASIS F OR TH E IR E XE MPTION.

INF ORMATION ON E XE MPT TRANSACTIONS IS ON TH E BACK OF TH IS F ORM.

Name of Purchaser

Telephone Number

Street Address

City

State/Zip Code

Name of Seller

Any purchaser who knowingly and intentionally lists items for resale that he/ she knows will not be resold, or provides an invalid exemption certificate with the intent to evade payment of the tax is guilty of a Class 1 misdemeanor and may be fined up to fifty percent of the tax in addition to the tax. SDCL

The undersigned certify that they have read this document and that the statements regarding the purchase, use or resale of each of the items are true. The undersigned are fully aware of the consequences that will result from the misuse of this certificate. The undersigned further asserts that they have the authority to complete and submit this document on behalf of the above named business.

Authorized Signature

Title

Name

Date

The person signing this certificate MUST check the applicable box showing the basis for the exemption from sales tax and provide the purchaser’s tax permit or exemption number. Tax permit numbers containing the letters “E T” or “UT” can not be used for

! 1. Government E ntity |

South Dakota E xemption # |

_____ - ______ - ____________ - _____ - ______ |

Icertify that the tangible personal property or services purchased are to be paid directly with funds from the entity noted on this form. “D irectly” does not include per diem, cash advances, or similar indirect payments. G overnment entities are not required to furnish exemption numbers.

! 2. |

South Dakota Tax Permit # |

_____ - ______ - ____________ - _____ - ______ |

Icertify that the items are being purchased by an authorized official of the

! 3. Relief Agency |

South Dakota E xemption # |

_____ - ______ - ____________ - _____ - ______ |

I certify that the items or services purchased are to be paid directly with funds from the entity noted.

! 4. Religious or Private E ducational Institutions South Dakota E xemption # _____ - ______ - ____________ - _____ - ______

Icertify that the items are being purchased by an authorized official of the religious or private educational institution; that payment is made from religious or private educational institutions funds; and the religious or private educational institution retains title to the property.

! 5. Agricultural Products and Services - I certify the items and services purchased will be used for exclusive agricultural purposes only.

! 6. Farm Machinery - I certify that the farm machinery, attachment unit, or irrigation equipment being purchased is to be used exclusively for agricultural purposes and qualifies for the 3% sales and use tax rate.

! 7. Direct Payment Permit |

South Dakota Direct Payment Permit # |

______________________________ |

|

|

|

I certify the entity listed on this form has a Direct Payment Permit and will accrue and pay the use tax directly to the department.

! 8. Resale or |

Tax Permit # |

___________________________________________________ |

If no permit number is available, provide reason:

D escribe nature of your business:

D escribe the items for which you are claiming exemption for:

DO N OT SEN D THI S CERTI FI CATE TO THE DEPARTMEN T OF REVEN UE & REGULATI ON . KEEP I T W I TH YOUR RECORDS I N CASE OF AN AUDI T.

The department recommends this certificate be reviewed annually.

1. Government - The sale of products and services to the following governmental entities is exempt from South Dakota sales and use tax: Indian Tribes; United States government agencies; State of South Dakota; Public or municipal corporations of the State of South Dakota; Municipal or volunteer fire or ambulance departments; Public schools, including

The governments from other states or the District of Columbia are exempt from sales tax if the law in that state provides a similar exemption for South Dakota governments. Governments providing a similar exemption are Colorado, Indiana, Iowa (motels and hotels are not exempt), Minnesota (motels and hotels are not exempt), Ohio, and West Virginia. The governments from states without a sales tax are exempt from South Dakota sales tax. These states are Alaska, Delaware, Montana, New Hampshire, and Oregon.

Documentation Required: Government entities must provide an exemption certificate to the vendor or the vendor must keep documentation to show the purchase was paid from government funds. Documentation may include a purchase order or a check stub. Government entities are not required to list an exemption number on the exemption certificate. The department issues some government entities exemption numbers. These agencies will include their exemption number on the exemption certificate. The exemption number for public schools contains the letters “RS”. The exemption number for other governments contains the letters “RG”.

2.

Documentation Required:

3.Relief Agencies - The sale of products and services to relief agencies is exempt from South Dakota sales and use tax. Relief agencies are

Documentation Required: In order to be exempt from sales and use tax, relief agencies must have a permit from the Department of Revenue & Regulation. The permit number contains the letters “RA”. Relief agencies must provide an exemption certificate to purchase products and services exempt from sales and use tax.

4.Religious and Private Schools - Churches are NOT exempt from South Dakota sales or use tax. The sale of products and services to religious or private educational institutions is exempt from South Dakota sales and use tax if the following three criteria are met: An authorized official of the religious or private educational institution makes the purchase; Payment is made from the religious or private educational institution’s funds; The religious or private educational institution retains title to the property.

To be exempt from sales and use tax, a private educational institution must: be an institution currently recognized as exempt under section 501(c)(3) of the Internal Revenue Code as in effect on January 1, 1995; Maintain a campus physically located within this state; and be accredited by the South Dakota Department of Education and Cultural Affairs or the North Central Association of Colleges and Schools.

Documentation Required: Religious or private educational institutions must have a permit from the Department of Revenue & Regulation to be exempt from sales or use tax. The permit contains the letters “RS” or “RE”. Religious or private educational institutions must provide an exemption certificate to purchase products and services exempt from sales and use tax.

Employee Purchases - The exemption from sales and use tax for governments,

5.Agricultural Products - Purchasers of products and services that are exempt when used exclusively by the purchaser for agricultural purposes must complete an exemption certificate if there is doubt as to the intended usage. Repair parts and services are subject to sales tax.

6.Farm Machinery, attachment units, and irrigation equipment used exclusively for agricultural purposes are subject to the 3% state sales tax. All- terrain vehicles of three or more wheels used exclusively by the purchaser for agricultural purposes on agricultural land are subject to the 3% state sales tax. Purchasers of farm machinery, attachment units, and irrigation equipment purchased for agricultural purposes must complete an exemption certificate if there is doubt as to the intended usage.

7.Direct Payment Permit - The Direct Payment Permit holder may provide an exemption certificate or provide a copy of their Direct Payment Permit to the vendor to purchase tangible personal property or services without sales tax. The following items may not be purchased using a Direct Payment Permit. These transactions are subject to the 4% state sales tax, plus applicable municipal tax at the time of purchase.

•purchases of taxable meals or beverages;

•purchases of taxable lodging or services related thereto;

•purchases of admissions to places of amusement, entertainment or athletic events, or the privilege of use of amusement devices;

•purchases of motor vehicles, or other tangible personal property required to be licensed or titled with a taxing authority, taxed under Title 32; or

•purchases of telecommunications services and utilities (gas, electricity, and heating fuel).

8.Resale or

To: |

HRE |

|

From: |

|

|

|

|

Fax: |

(509) |

Pages: |

|

|

|

|

|

Phone:(509) |

Date: |

||

|

|

|

|

Re: |

TAX EXPEMPT CERTIFICATE |

CC: |

|

|

|

|

|

NOTES: