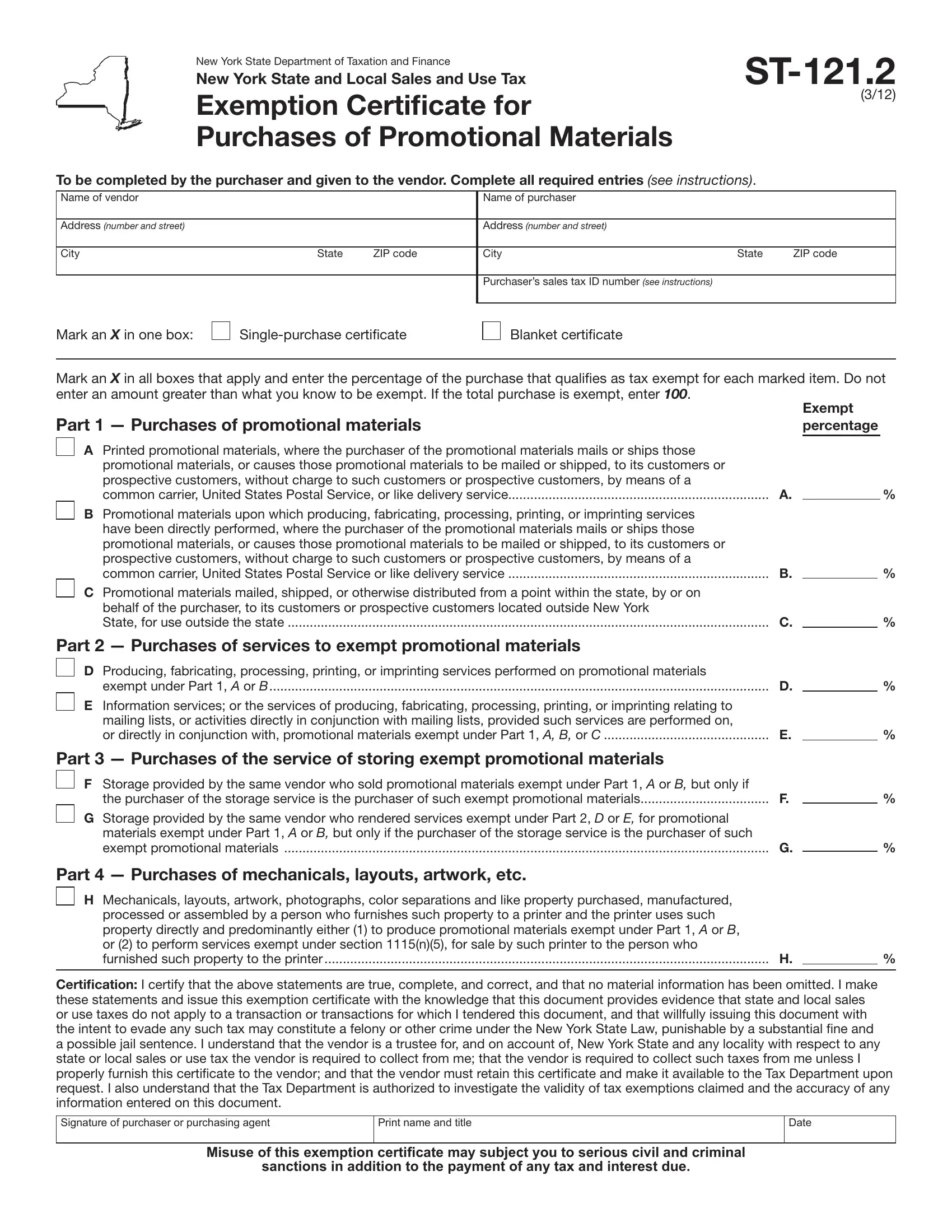

In the realm of business operations within New York State, understanding and utilizing specific tax forms is essential for compliance and optimal financial management. Among these, the ST-121.2 form plays a critical role for entities dealing with promotional materials. Issued by the New York State Department of Taxation and Finance, this Exemption Certificate for Purchases of Promotional Materials facilitates a streamlined process for organizations to certify that their purchases of promotional materials, or associated services, qualify for tax exemption. The form encompasses various sections, including details about the purchaser and vendor, a categorization of the promotional materials or services purchased, and explicit instructions for both parties involved. It distinguishes between single-purchase and blanket certificates, requires a clear indication of the tax-exempt percentage of the purchase, and covers specific exemptions for stored promotional materials, services related to the production of said materials, and other essential items like mechanicals and artwork used in their creation. With provisions for certifying the accuracy and truthfulness of the information provided, the ST-121.2 form underscores the importance of honest communication between buyers and vendors in the intricate ecosystem of New York State's sales and use tax regulations. It also outlines the serious implications for misuse, including potential civil and criminal sanctions, thus ensuring that all parties approach the exemption with the gravity it warrants. This extensive guide serves not only as a transactional document but also as a valuable resource for understanding the nuances of tax-exempt purchases related to marketing and promotional efforts in New York State.

| Question | Answer |

|---|---|

| Form Name | Form St 121 2 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | st121_2_fill_in st 1212 form |