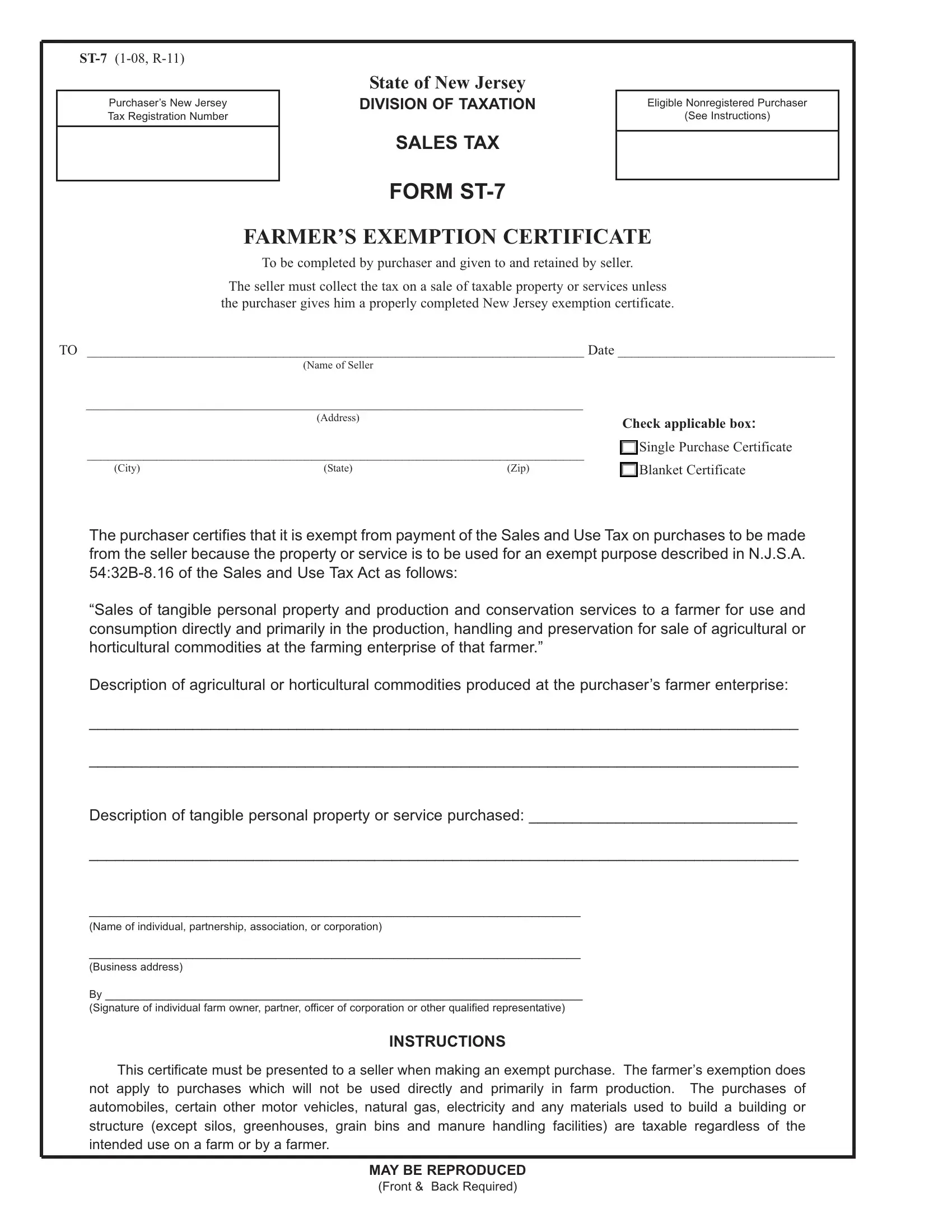

ST-7 (1-08, R-11)

Purchaser’s New Jersey Tax Registration Number

State of New Jersey

DIVISION OF TAXATION

SALES TAX

FORM ST-7

Eligible Nonregistered Purchaser

(See Instructions)

FARMER’S EXEMPTION CERTIFICATE

To be completed by purchaser and given to and retained by seller.

The seller must collect the tax on a sale of taxable property or services unless the purchaser gives him a properly completed New Jersey exemption certificate.

TO _______________________________________________________________________ Date _______________________________

(Name of Seller

_______________________________________________________________________

|

(Address) |

|

Check applicable box: |

|

|

|

_______________________________________________________________________ |

|

Single Purchase Certificate |

|

|

|

(City) |

(State) |

(Zip) |

|

Blanket Certificate |

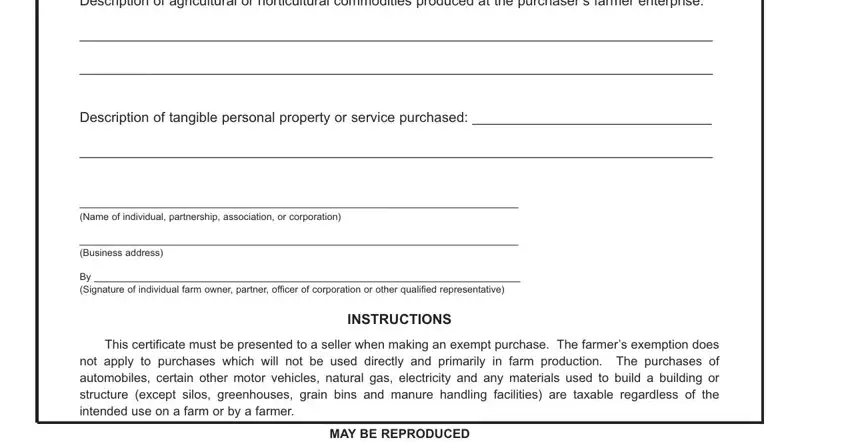

ThepurchasercertifiesthatitisexemptfrompaymentoftheSalesandUseTaxonpurchasestobemade from the seller because the property or service is to be used for an exempt purpose described in N.J.S.A. 54:32B-8.16 of the Sales and Use Tax Act as follows:

“Sales of tangible personal property and production and conservation services to a farmer for use and consumption directly and primarily in the production, handling and preservation for sale of agricultural or horticultural commodities at the farming enterprise of that farmer.”

Description of agricultural or horticultural commodities produced at the purchaser’s farmer enterprise:

__________________________________________________________________________________

__________________________________________________________________________________

Description of tangible personal property or service purchased: _______________________________

__________________________________________________________________________________

_______________________________________________________________________

(Name of individual, partnership, association, or corporation)

_______________________________________________________________________

(Business address)

By _____________________________________________________________________

(Signature of individual farm owner, partner, officer of corporation or other qualified representative)

INSTRUCTIONS

This certificate must be presented to a seller when making an exempt purchase. The farmer’s exemption does not apply to purchases which will not be used directly and primarily in farm production. The purchases of automobiles, certain other motor vehicles, natural gas, electricity and any materials used to build a building or structure (except silos, greenhouses, grain bins and manure handling facilities) are taxable regardless of the intended use on a farm or by a farmer.

MAYBE REPRODUCED

INSTRUCTIONS FOR USE OFFARMER’S EXEMPTION CERTIFICATE (ST-7)

1.ScopeofFarmer’sExemption-This certificate may be usedonlyby businesses that are treated as“farmingenterprises” under N.J.S.A. 54:32B-8.16 of the Sales and Use TaxAct. A“farming enterprise” means an enterprise using land to raise agricultural or horticultural commoditiesforsale. Farmingenterprisesinclude,butarenotlimitedto,enterprisesproducingdairyproducts,poultry,feedcrops,fruit, vegetables, livestock, fur animals, timber, ornamental plants, bees and apiary products.

NOTE: For sales and use tax purposes, a “farming enterprise” does not include an enterprise that is primarily engaged in boarding or training horses or in selling agricultural or horticultural products produced by others.

The farmer’s exemption applies only to sales of tangible personal property or services which will be used directly and primarily in agricultural or horticultural production. It does not apply to sales of: motor vehicles, natural gas, electricity, or property to be used to construct a building or structure (with the exception of silos, greenhouses, grain bins, or manure handling facilities).

NOTE: Whenpurchasingatruckortrucktractorwithagrossvehicleweightratingofmorethan18,000poundswhichisregisteredwith the New Jersey Division of Motor Vehicles as a farm vehicle or a commercial over-the-road truck with a gross vehicle weight rating over 26,000 pounds which is registered in New Jersey, the purchaser must use an Exempt Use Certificate (ST-4) rather than a Farmer’s Exemption Certificate. See N.J.S.A. 54:32B-8.43.

2.Good Faith- To act in good faith means to act in accordance with standards of honesty. In general, registered sellers who accept exemption certificates in good faith are relieved of liability for the collection and payment of sales tax on the transaction covered by the exemption certificate.

In order for good faith to be established, the following conditions must be met:

(a)Certificate must contain no statement or entry which the seller knows is false or misleading;

(b)Certificate must be an official form or a proper and substantive reproduction, including electronic;

(c)Certificate must be filled out completely;

(d)Certificate must be dated and include the purchaser’s New Jersey tax identification number or, for a purchaser that is not registered in New Jersey, the Federal employer identification number or out-of-State registration number. Individual purchasers must include their driver’s license number; and

(e)Certificate or required data must be provided within 90 days of the sale.

The seller may, therefore, accept this certificate in good faith as a basis for exempting sales to the signatory purchaser and is relieved of liability even if it is determined that the purchaser improperly claimed the exemption.

3.Blanket Certificates - Aseller may permit a purchaser to file a blanket Farmer’s Exemption Certificate to cover future purchases of similar items of tangible personal property. However, each subsequent sales slip or purchase invoice based on such blanket certificate must be clearly marked with the purchaser’s name, address, and identification number.

4.Eligible Nonregistered Purchaser - If the purchaser is not required to be registered with the New Jersey Division ofTaxation and does not have a New Jersey Tax Registration Number, the purchaser is required to place either his Federal Identification Number or, if a sole proprietor, the last three digits of his Social Security Number in the box at the top, right corner of the form marked “Eligible NonregisteredPurchaser.” Note: AnyNewJerseyfarmerwhoisnotasoleproprietor,orwhosellsanygoodsorservicessubjecttosales tax, or who is an employer, must be registered with the New Jersey Division of Taxation and therefore cannot be an “eligible nonregistered purchaser”.

5.ImproperCertificate-Salestransactionswhicharenotsupportedbyproperlyexecutedexemptioncertificatesaredeemed tobetaxableretailsales. Inthissituation,theburdenofproofthatthetaxwasnotrequiredtobecollectedisupontheseller.

6.Retention of Certificates - Certificates must be retained by the seller for a period of not less than four years from the date of the sale covered by the certificate.

REPRODUCTION OFFARMER’S EXEMPTION CERTIFICATES:

Private reproduction of both sides of these certificates may be made without the prior permission of the Division of Taxation

FOR MORE INFORMATION:

Call the Customer Service Center (609) 292-6400. Send an e-mail to nj.taxation@treas.state.nj.us. Write to: New Jersey Division of Taxation, Information and Publications Branch, PO Box 281, Trenton, NJ 08695-0281.