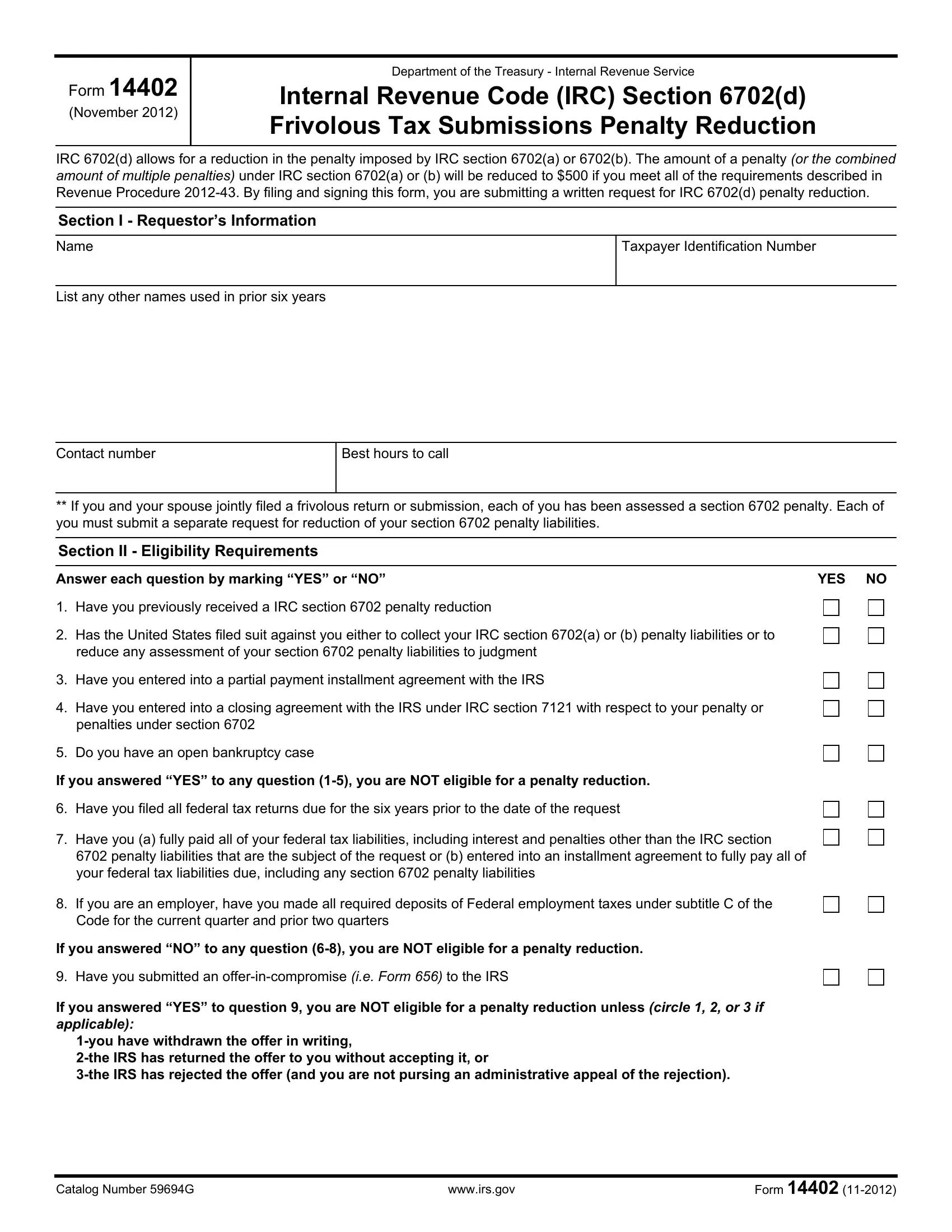

The Internal Revenue Service (IRS) Form 14402 is a crucial document for individuals seeking a reduction in penalties imposed for frivolous tax submissions under Internal Revenue Code (IRC) Section 6702(a) or (b). Introduced in November 2012, this form allows for a penalty reduction to $500 if specific requirements outlined in Revenue Procedure 2012-43 are met. Individuals must submit a written request by signing and filing Form 14402 to qualify for this reduction. The form comprises several sections, including Requestor's Information, Eligibility Requirements, Payment Information, and a Declaration Under Penalties of Perjury, encapsulating comprehensive details about the taxpayer, their eligibility based on past actions and current financial commitments, the minimum payment information, and a solemn declaration about the truthfulness of the information provided. Particularly, the eligibility criteria outlined demand a thorough review of the taxpayer's past six years' filing history, any existing agreements with the IRS, and current financial obligations towards federal taxes. By filing Form 14402, individuals assert under penalty of perjury that they have fulfilled all federal tax obligations excluding the IRC Section 6702 penalties in question. This form not only serves as a pathway for penalty reduction but also enforces strict compliance with federal tax laws, thereby promoting a fair and efficient tax administration system.

| Question | Answer |

|---|---|

| Form Name | Irs Form 14402 |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | 59694G, irs form 14402, 3-the, SSN |