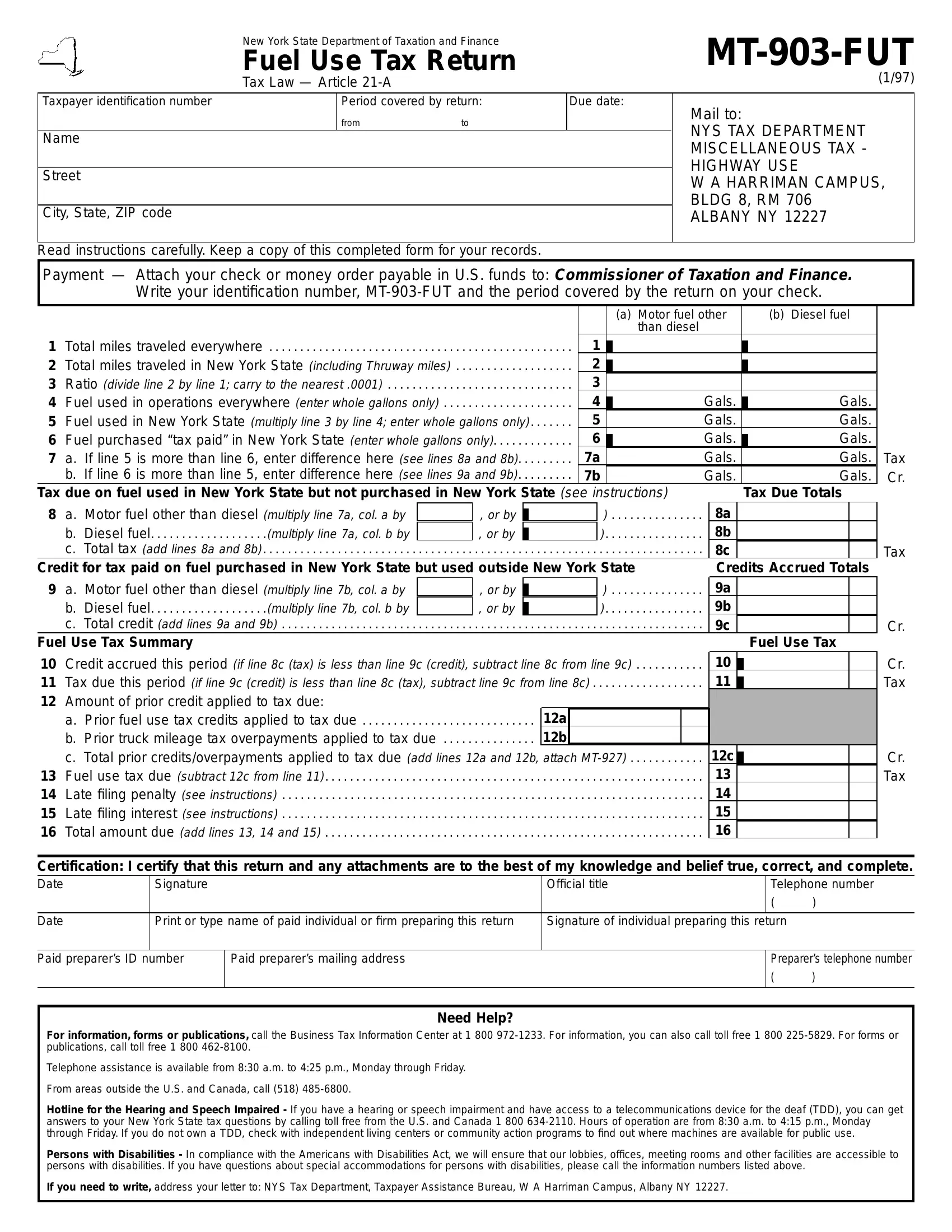

Understanding the intricacies of the Mt 903 Fut form, an essential document for those navigating New York State's taxation landscape, is invaluable for carriers operating vehicles subject to fuel use taxation. Issued by the New York State Department of Taxation and Finance, this Fuel Use Tax Return, adhering to Tax Law Article 21-A, plays a critical role in ensuring compliance with state tax obligations. Designed for a precise period, and with a strict deadline for submission, it requires detailed information about the taxpayer and the operational metrics of vehicles, including total miles traveled and fuel used both within and outside New York State. It demands meticulous record-keeping and an accurate calculation of the tax payable or credit due, factoring in fuel purchases that have already been taxed. Instructions are provided to aid in the accurate completion of the form, highlighting the importance of keeping a copy for records, the need for accurate figures regarding fuel consumption, and the possibility of facing penalties for late submissions or inaccurate filings. The form also opens up avenues for credits or refunds under certain conditions, emphasizing the state's acknowledgment of fair taxation practices. Carriers must therefore approach this form with diligence, ensuring that all required information is accurately reported to avoid penalties and to capitalize on potential credits.

| Question | Answer |

|---|---|

| Form Name | Mt 903 Fut Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | instruction for mt 903 ny, form mt 903 instructions, mt 903 1 form, mt 903 fut form |

|

|

New York State Department of Taxation and Finance |

|

|

|

|

|

||||||

|

|

Fuel Use Tax Return |

|

|

|

|

|

||||||

|

|

Tax Law — Article |

|

|

|

|

|

|

|

|

|

(1/97) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

||

Taxpayer identification number |

|

Period covered by return: |

Due date: |

Mail to: |

|

|

|

||||||

|

|

|

from |

to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NYS TAX DEPARTMENT |

|

||||

Name |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

MISCELLANEOUS TAX - |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

HIGHWAY USE |

|

||

Street |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

W A HARRIMAN CAMPUS, |

|||||

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

BLDG 8, RM 706 |

|

||

City, State, ZIP code |

|

|

|

|

|

|

|

|

ALBANY NY 12227 |

|

|||

|

|

|

|

|

|

|

|

|

|

||||

Read instructions carefully. Keep a copy of this completed form for your records. |

|

|

|

|

|

|

|

|

|

||||

Payment — Attach your check or money order payable in U.S. funds to: Commissioner of Taxation and Finance. |

|

||||||||||||

|

Write your identification number, |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

(a) Motor fuel other |

|

(b) Diesel fuel |

|

||

|

|

|

|

|

|

|

|

than diesel |

|

|

|

||

1 |

Total miles traveled everywhere |

|

|

1 |

|

|

|

|

|

|

|

||

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

||||||

2 |

Total miles traveled in New York State (including Thruway miles) |

|

|

2 |

|

|

|

|

|

|

|

||

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

|

|

||||||

3 |

. . . . . . . . . . . .Ratio (divide line 2 by line 1; carry to the nearest .0001) |

. . . . . . . . . . . . . . . . . |

. |

3 |

|

|

|

|

|

|

|

||

4 |

Fuel used in operations everywhere (enter whole gallons only) |

|

|

4 |

|

|

|

Gals. |

|

Gals. |

|

||

. . . . . . . . . . . . . . . . . |

|

|

|

|

|

||||||||

5 |

Fuel used in New York State (multiply line 3 by line 4; enter whole gallons only) |

. |

5 |

|

|

|

Gals. |

|

Gals. |

|

|||

6 |

Fuel purchased ‘‘tax paid’’ in New York State (enter whole gallons only) |

|

6 |

|

|

|

Gals. |

|

Gals. |

|

|||

|

|

|

|

|

|||||||||

7 |

a. If line 5 is more than line 6, enter difference here (see lines 8a and 8b) |

. |

7a |

|

|

|

Gals. |

|

Gals. |

Tax |

|||

|

. . . . . . . .b. If line 6 is more than line 5, enter difference here (see lines 9a and 9b) |

. |

7b |

|

|

|

Gals. |

|

Gals. |

Cr. |

|||

Tax due on fuel used in New York State but not purchased in New York State (see instructions) |

|

Tax Due Totals |

|||||||||

8 |

a. Motor fuel other than diesel (multiply line 7a, col. a by |

|

, or by |

|

|

) |

8a |

|

|

|

|

|

|||||||||||

|

b. Diesel fuel |

(multiply line 7a, col. b by |

|

, or by |

|

|

) |

8b |

|

|

|

|

|

|

|

|

|

|

|||||

|

c. Total tax (add lines 8a and 8b) |

. . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . |

. . . . . . . . |

. |

. . . . . . . . . . . |

. . . . . . . . . . . . . . . . . |

8c |

|

|

|

Credit for tax paid on fuel purchased in New York State but used outside New York State |

Credits Accrued Totals |

||||||||||

9 |

a. Motor fuel other than diesel (multiply line 7b, col. a by |

|

, or by |

|

|

) |

9a |

|

|

|

|

|

|

||||||||||

|

b. Diesel fuel |

(multiply line 7b, col. b by |

|

, or by |

|

|

) |

9b |

|

|

|

|

|

|

|

|

|

|

|||||

|

. . . . . . . . . . . . . . . . . . . . . .c. Total credit (add lines 9a and 9b) |

. . . . . . . . . |

. . . . . . . . |

. |

. . . . . . . . . . . |

. . . . . . . . . . . . . . . . . |

9c |

|

|

|

|

Fuel Use Tax Summary |

|

|

|

|

|

|

|

|

Fuel Use Tax |

||

10 |

Credit accrued this period (if line 8c (tax) is less than line 9c (credit), subtract line 8c from line 9c) |

10 |

|

|

|

||||||

|

|

|

|||||||||

11 |

Tax due this period (if line 9c (credit) is less than line 8c (tax), subtract line 9c from line 8c) |

|

11 |

|

|

|

|||||

. . . . . . . . . . . . . . . . . |

|

|

|

||||||||

12Amount of prior credit applied to tax due:

|

a. Prior fuel use tax credits applied to tax due |

12a |

|

|

b. Prior truck mileage tax overpayments applied to tax due |

12b |

|

|

c. Total prior credits/overpayments applied to tax due (add lines 12a and 12b, attach |

12c |

|

13 |

Fuel use tax due (subtract 12c from line 11) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

13 |

14 |

Late filing penalty(see instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

14 |

15 |

Late filing interest(see instructions) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

15 |

16 |

Total amount due (add lines 13, 14 and 15) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

16 |

Tax

Cr.

Cr. Tax

Cr. Tax

Certification: I certify that this return and any attachments are to the best of my knowledge and belief true, correct, and complete.

Date

Date

Signature |

Official title |

|

Telephone number |

|

|

( |

) |

Print or type name of paid individual or firm preparing this return |

Signature of individual preparing this return |

||

|

|

|

|

Paid preparer’s ID number

Paid preparer’s mailing address

Preparer’s telephone number

( )

Need Help?

For information, forms or publications, call the Business Tax Information Center at 1 800

Telephone assistance is available from 8:30 a.m. to 4:25 p.m., Monday through Friday.

From areas outside the U.S. and Canada, call (518)

Hotline for the Hearing and Speech Impaired - If you have a hearing or speech impairment and have access to a telecommunications device for the deaf (TDD), you can get answers to your New York State tax questions by calling toll free from the U.S. and Canada 1 800

Persons with Disabilities - In compliance with the Americans with Disabilities Act, we will ensure that our lobbies, offices, meeting rooms and other facilities are accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, please call the information numbers listed above.

If you need to write, address your letter to: NYS Tax Department, Taxpayer Assistance Bureau, W A Harriman Campus, Albany NY 12227.

Instructions for Completing

General Information — Carriers must report vehicles that are subject to the New York fuel use tax either on Form

–motor vehicles that have two axles and a gross vehicle weight or registered gross vehicle weight exceeding 26,000 pounds; or

–motor vehicles that have three or more axles regardless of weight; or

–motor vehicles that are used in combination, when the weight of such combination exceeds 26,000 pounds gross vehicle weight.

See Publication 538, Guide to Highway Use Taxes and Other New York State Taxes for Carriers, for a list of the vehicles exempt in New York State from the fuel use tax.

A carrier that operates a vehicle subject to the fuel use tax, but not subject to IFTA, must report the vehicle on Form

A carrier that operates a vehicle in two or more IFTA jurisdictions must get an IFTA license if the vehicle is subject to the fuel use tax in any of the IFTA jurisdictions in which the vehicle operates. A carrier that operates a vehicle under an IFTA license should report the vehicle on its base jurisdiction’s IFTA tax return.

Line Instructions

Line 1 – Enter the total miles traveled both in and outside New York State by vehicles that entered the state during the reporting period. Include mileage traveled by tractors with no trailers. Use whole miles.

Line 2 – Enter the total miles traveled in New York State by vehicles during the reporting period. Include mileage traveled by tractors with no trailers, and mileage on the New York State Thruway. Use whole miles.

Line 3 – Divide line 2 by line 1, and enter the decimal ratio. Carry to the nearest four decimal places (e.g., .0001).

Line 4 – Enter the total gallons of fuel used in operations both in and outside New York State by vehicles that entered the state during the reporting period. Use whole gallons.

Line 5 – Multiply the number of gallons on line 4 by the ratio on line 3, and enter the result. This is the number of gallons used in operations in New York State. Use whole gallons.

Line 6 – Enter the total number of gallons of fuel purchased tax paid (fuel upon which New York State sales and fuel taxes have been paid) in New York State during the reporting period for use in operations both in and outside this state.

Line 7a – If line 5 is greater than line 6, subtract line 6 from line 5. If line 6 is equal to or more than line 5, enter ‘‘0’’.

Line 7b – If line 6 is greater than line 5, subtract line 5 from line 6. If line 5 is equal to or more than line 6, enter ‘‘0’’.

The rates used for lines 8a, 8b, 9a and 9b are established by the Commissioner of Taxation and Finance for each period. To get the rates for any particular filing period, call the Business Tax Information Center at 1 800

If you maintain substantiating records, see Calculating Alternative Rates for lines 8a, 8b, 9a, and 9b.

Line 8a – Multiply line 7a, column (a), by the tax rate provided by the Business Tax Information Center, and enter the result.

Line 8b – Multiply line 7a, column (b), by the tax rate provided by the Business Tax Information Center, and enter the result.

Line 8c – Add lines 8a and 8b.

Line 9a – Multiply line 7b, column (a), by the tax rate provided by the Business Tax Information Center, and enter the result.

Line 9b – Multiply line 7b, column (b), by the tax rate provided by the Business Tax Information Center, and enter the result.

Line 9c – Add lines 9a and 9b.

Line 10 – If line 8c is less than line 9c, subtract line 8c from line 9c. The balance is the credit accrued this reporting period, and may be carried forward and applied against any fuel use tax liability accrued within the following two years. You may apply for a refund of this credit by filing Form

Line 11 – If line 9c is less than line 8c, subtract line 9c from line 8c. This is the tax due this period.

Line 12a – If you have prior fuel use tax credit, enter the amount needed to satisfy any fuel use tax liability shown on line 11. Include only fuel use tax credits for which you have not filed a claim for refund. Fuel use tax credits may be applied against any fuel use tax liability on returns covering a period that falls wholly within the following two years.

Line 12b – If you have a prior unused truck mileage tax overpayment, enter the amount needed to satisfy any fuel liability shown on line 11 less the amount of prior fuel use tax credits entered on line 12a. Truck mileage tax overpayments made after December 31, 1993, expire four years from the date of the overpayment.

Line 12c – Add lines 12a and 12b.

Line 13 – Subtract line 12c from line 11. This is the amount of fuel use tax due. If there is no fuel use tax due, enter ‘‘0’’ on this line.

Line 14 – Any tax due shown on line 13 that remains unpaid after the due date of the return is subject to a penalty of $50 or 10% of the unpaid portion of the line 13 amount, whichever is greater.

In addition, failure to file returns and pay any tax due may result in criminal penalties under Article 37 of the Tax Law.

Line 15 – Any tax due shown on line 13 that remains unpaid after the due date of the return is subject to interest computed at the rate of 1% per month or any part of a month from such due date until the date the tax is paid.

Certification

Sign and date the return and enter your official title and telephone number. Only the taxpayer or an authorized agent may sign the return.

Additionally, if anyone other than an employee, owner, partner or officer of the business is paid to prepare the return, he or she is required to sign and date the return and provide his or her mailing address and telephone number.

Calculating Alternative Rates

If you maintain substantiating records, you may compute the sales tax components for diesel and other motor fuel based on the average price per gallon of these fuels used during the reporting period, instead of using the prevailing price sales tax component included in the tax and credit rates provided by the Business Tax Information Center. To compute the sales tax components separately for diesel and other motor fuel:

1.Determine the total cost of fuel used during the reporting period, including federal, state and local taxes, but not including state or local sales taxes or any other taxes upon which state and any local sales tax is not computed. For example, in New York State the diesel motor fuel tax and the motor fuel tax are not included in the total cost of fuel.

2.Divide this amount by the total number of gallons of fuel you used in your operations (either in or outside New York State) to arrive at the average price per gallon.

3.Compute the sales tax component by multiplying the average price per gallon by 7% (rounding to the nearest tenth of a cent; e.g., .08753 5 .088).

4.Subtract the sales tax component included in the tax/credit rate provided by the Business Tax Information Center, and add the sales tax component that you computed.

If the rates you calculated are different from the rates provided by the Business Tax Information Center, indicate your rates in the boxes on the corresponding line, and use them in computing your fuel use tax liabilities and credits.

Privacy Notification

The right of the Commissioner of Taxation and Finance and the Department of Taxation and Finance to collect and maintain personal information, including mandatory disclosure of social security numbers in the manner required by tax regulations, instructions, and forms, is found in Articles 8,

The Tax Department will use this information primarily to determine and administer the gas and diesel motor fuel, petroleum, highway use, and fuel use taxes under Articles

Failure to provide the required information may result in civil or criminal penalties, or both, under the Tax Law. In some cases, failure to provide the required information may result in denial, cancellation, or suspension of a registration as a distributor of motor fuel or of a license as a terminal operator or importing/exporting transporter.

This information will be maintained by the Director of the Registration and Data Services Bureau, NYS Tax Department, Building 8 Room 924, W A Harriman Campus, Albany NY 12227; telephone 1 800