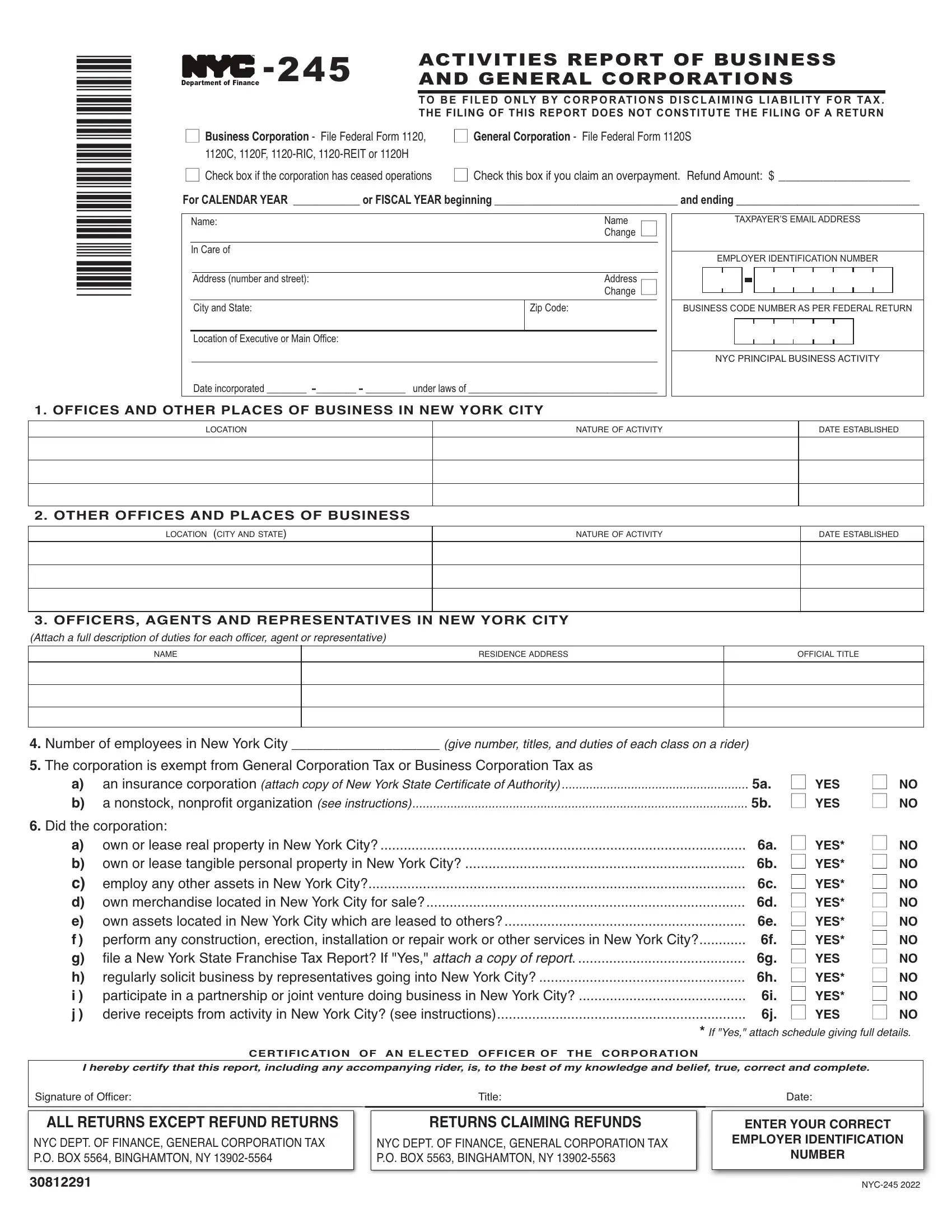

In the complex landscape of New York City's tax obligations for corporations, understanding and navigating through forms like the NYC-245 becomes crucial. The NYC-245, also known as the Activities Report of Business and General Corporations, serves a specific function. It is designed exclusively for corporations that assert they are not liable for the New York City General Corporation Tax or Business Corporation Tax. This form acts as a declaration by corporations disclaiming tax liability rather than a tax return. It requires detailed information about the corporation's activities, places of business within New York City, and various aspects of its operations that could influence its tax status. The form takes into account factors such as the presence of officers, agents, representatives, and employees in the city, the lease of tangible property, and the maintenance of assets within the city that could imply a liability for city taxes. Additionally, the NYC-245 investigates whether the corporation conducts sales, leases, or business operations within New York City in ways that might subject it to tax obligations. Its filing does not start the clock on the statute of limitations for tax assessments, highlighting the need for proper filing of actual tax returns to gain that protection. The instructions stipulate that corporations enjoying certain tax exemptions or those who merely maintain minimal connections with the city without substantive business activities might not need to file this report. This form and its accompanying instructions delineate the boundaries between being subject to New York City's corporate taxes and being exempt, making it an essential tool for corporations navigating their fiscal responsibilities within the city.

| Question | Answer |

|---|---|

| Form Name | Nyc 245 Form |

| Form Length | 3 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 45 sec |

| Other names | Get the free Form NYC-245 "Activities Report of ... |

*30812191*

ACTIVITIES REPORT OF BUSINESS |

|

|

AND GENERAL CORPORATIONS |

|

TO B E F I L E D O N LY B Y C O R P O R AT I O N S D I S C L A I M I N G L I A B I L I T Y F O R TA X . |

|

THE FILING OF THIS REPORT DOES NOT CONSTITUTE THE FILING OF A RETURN |

■ BusinessCorporationileeelo |

■ GeneralCorporationileeelo |

|

To |

|

|

■ eboifteotionasaseoetions |

■ etisboifyoaimanoayment |

Refnnt$ |

For CALENDAR YEAR ____________ or FISCAL YEAR beginning _________________________________ and ending _________________________________

Name: |

|

Name |

■ |

|

|

|

|

Change |

|

|

|

|

|

|

In Care of |

|

|

|

|

|

|

|

|

|

|

Address (number and street): |

|

Address |

■ |

|

|

|

Change |

|

|

|

|

|

|

|

City and State: |

|

Zip Code: |

|

|

|

|

|

|

|

Location of Executive or Main Office: |

|

|

|

|

|

|

|

|

|

Date incorporated ________ |

under laws of ______________________________________ |

||

TAXPAYER’S EMAIL ADDRESS

EMPLOYER IDENTIFICATION NUMBER

BUSINESS CODE NUMBER AS PER FEDERAL RETURN

TVT

1. OFFICES AND OTHER PLACES OF BUSINESS IN NEW YORK CITY

T |

TR |

TVT |

T |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

OTHER OFFICES AND PLACES OF BUSINESS |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

T |

T |

T |

|

|

TR |

TVT |

T |

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

OFFICERS, AGENTS AND REPRESENTATIVES IN NEW YORK CITY |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R |

R |

|

|

TT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.mbeofemloyeesineoity |

|

( |

|

|

|

5.TeotionisemtfmenelootionTaosiness |

ootionTaas |

|

|

||

a) |

aninsnotion |

(w |

5a. |

■ YES |

■ NO |

b) |

anonstononfitoanition |

( |

5b. |

■ YES |

■ NO |

6.iteotion

a) |

onoleasealeyineoity |

|

6a. |

■ YES* |

■ NO |

b) |

onoleasetangibleenaleyineoity |

|

6b. |

■ YES* |

■ NO |

c) |

emloyanyoteassetsineoity |

|

6c. |

■ YES* |

■ NO |

d) |

onmeaniseloteineoityfosale |

|

6d. |

■ YES* |

■ NO |

e) |

onassetsloteineoityialeasetoote |

|

6e. |

■ YES* |

■ NO |

f) |

eoanynstioneioninstallationoaioo |

otesesineoity |

6f. |

■ YES* |

■ NO |

g) |

fileaeoateniseTaReofes |

|

6g. |

■ YES |

■ NO |

h) |

fileaeoateitiesReoT fes |

|

6h. |

■ YES |

■ NO |

i) |

glaysolitbsinessbysentatisgoingintoeo |

ity |

6i. |

■ YES* |

■ NO |

j) |

aiateinaaneiojointntoingbsinessi |

neoity |

6j. |

■ YES* |

■ NO |

|

|

|

* |

|

|

CERTIFICATION OF AN ELECTED OFFICER OF THE CORPORATION

I hereby certify that this report, including any accompanying rider, is, to the best of my knowledge and belief, true, correct and complete.

gnatofffi

ALLRETURNSEXCEPTREFUND RETURNS

RRTT

30812191

Title

RETURNSCLAIMINGREFUNDS

RRTT

ate

ENTER YOUR CORRECT

EMPLOYER IDENTIFICATION

NUMBER

Instructionsfor Form |

Page 2 |

|

|

This report must be filed by any corporation that has an officer, employee, agent, or rep- resentative in the City and claims not to be subject to the New York City General Cor- poration Tax or Business Corporation Tax. For taxable years beginning in 1996 and thereafter,entitiestaxableascorporationsfor federal income tax purposes under IRC §7701(a)(3) and §7704 are considered cor- porationsforpurposesoftheGeneralCorpo- ration Tax. A corporation subject to

GeneralCorporationTaxorBusinessCor- porationTaxcannotusethisform;it must file a General Corporation Tax return, Form

A corporation is not required to file this re- port if it falls under one of the following:

1)the corporation is exempt from the Gen- eral Corporation Tax under Section 11- 603.4 or the Business Corporation Tax under Section

2)thecorporationhasreceivedaletterfrom the Department of Finance exempting it from tax as a nonstock, nonprofit corpo- ration(seeinstructionsforline5bbelow), provided there has been no change in its character, activities or federal tax status since the date of that letter;

3)the corporation’sonlytiewithNewYork City is that one or more of the corpora- tion’s officers, employees, agents or rep- resentatives reside in the City or come into the City infrequently in connection withisolatedtransactionsofthecorpora- tion;

4)thecorporationisaRealEstateMortgage Investment Conduit (REMIC); or

5)the corporation is exempt from Federal income tax under IRC section 501(c)(2) or (25).

WHENTOFILE

Any S corporation required to file this report mustdosoannually,onorbeforeMarch15th if it reports on a calendar year basis for fed- eral income tax purposes, or on or before the 15thdayofthe3rdmonthfollowingtheclose of its fiscal year if it reports on a fiscal year basis.

AnyCcorporationrequiredtofilethisreport must do so annually, on or beforeApril 15th if it reports on a calendar year basis for fed- eral income tax purposes, or on or before the 15thdayofthe4thmonthfollowingtheclose of its fiscal year if it reports on a fiscal year basis.

LINE5b

Every corporation claiming exemption from GeneralCorporationTaxorBusinessCorpo- ration Tax as a nonstock, nonprofit corpora- tion (except for corporations exempt from federal income tax under IRC Section 501(c)(2) and (25)) must apply for an ex- emption from the Department of Finance by submittinganapplicationforexemptioncon- taininganaffidavitsettingforththefollowing information about the corporation:

1)the type of organization;

2)the purposes for which it is organized;

3)a description of its actual activities;

4)the source and disposition of its income;

5)whether any of its income is credited to surplusormayinuretoanyprivatestock- holder or individual; and

6)such other facts that may affect its right to exemption.

The affidavit must be supplemented by: a copy of the articles of incorporation or arti- cles of association, a copy of the bylaws, copies of statements showing the corpora- tion's assets and liabilities and receipts and disbursements for the most recent year, a photostatic copy of a letter from the United StatesTreasuryDepartmentgrantingthecor-

poration an exemption from federal income taxationandphotocopiesoffederal,stateand local tax returns filed by the organization for the three most recent preceding years.

All of the above information should be sent to:

NYCDepartmentofFinance ExemptionProcessingUnit 59MaidenLane,20thFloor NewYork,NY 10038

There is no prescribed application form and no application fee.

LINE6

If you answer "yes" to any question other than 6h, the corporation may be subject to GeneralCorporationTaxorBusinessCorpo- ration Tax. See "Corporations Subject to Tax" for more information. Corporations subject to tax cannot use this form.

LINE6g

Iftheanswertoquestion6gis“yes,”stateon a rider what activities take place elsewhere in NewYork State that do not also take place in New York City, or other reasons for filing a State Franchise Tax Report.

LINE6i

If the answer is "yes," see section 11- 04(b)(11) of Title 19 of the Rules of the City of New York for information regarding the application of P.L.

CORPORATIONSSUBJECTTOTAX

A corporation subject to General Corpo- ration Tax or Business Corporation Tax cannotusethisform;itmustfileeitherForm

1)doing business in New York City;

2)employing capital in New York City;

3)owning or leasing property in New York City,inacorporateororganizedcapacity; or

4)maintaining an office in New York City.

Instructionsfor Form |

Page 3 |

|

|

The term “doing business” is used in a com- prehensive sense and includes all activities that occupy the time or labor of people for profit. Regardless of the nature of its activi- ties, every corporation organized for profit andcarryingoutanyofthepurposesofitsor- ganization is deemed to be “doing business” for the purpose of the tax. In determining whether a corporation is doing business, it is immaterial whether its activities actually re- sult in a profit or a loss.

UndertheBusinessCorporationTaxapplica- ble to federal C Corporations for tax years beginning on or after January 1, 2015, a cor- poration is doing business in the city if:

(1)it has issued credit cards to one thousand or more customers who have a mailing address within the city as of the last day of its taxable year;

(2)it has merchant customer contracts with merchants and the total number of loca- tions covered by those contracts equals onethousandormorelocationsinthecity to whom the corporation remitted pay- ments for credit card transactions during the taxable year; or

(3)the sum of the number of customers de- scribed in item #1 plus the number of lo- cationscoveredbyitscontractsdescribed in item #2 equals one thousand or more.

For purpose of these provisions, the term “creditcard”includesbank,credit,traveland entertainmentcards.SeeAdministrativeCode Section

The term “employing capital” includes any of a large variety of uses, which may overlap other categories and give rise to taxable sta- tus. In general, the use of assets instrumen- tal in maintaining or aiding the corporate enterprise or activity in the City will create liability. Employing capital includes activi- ties such as:

a)maintaining stockpiles of raw materials or inventories; and

b)maintaining securities in the City for trading purposes.

Under Sections

taining an office in NewYork City by reason of:

a)the maintenance of cash balances with banks or trust companies or brokers in the City;

b)the ownership of shares of stock or secu- ritieskeptintheCity,ifkeptinasafede- posit box, safe, vault or other receptacle rented for the purpose, or if pledged as collateral security, or if deposited with oneor more banksor trust companies, or brokers who are members of a recog- nized security exchange, in safekeeping or custody accounts;

c)thetakingofanyactionbyanysuchbank or trust company or broker which is in- cidental to the rendering of safekeeping or custodial service to the corporation;

d)the maintenance of an office in the City by one or more officers or directors of the corporation who are not employees of the corporation as long as the corpo- ration is not otherwise doing business or employing capital in the City and does not own or lease property in the City;

e)the keeping of books or records of a cor- poration in the City if the books or records are not kept by employees of the corporation and the corporation is not otherwise doing business or employing capital in the City and does not own or lease property in the City; or

f)anycombinationoftheforegoingactivities.

In addition, a corporation will not be subject to the General Corporation Tax or Business Corporation Tax if its sole connection with New York City is:

(i)the maintenance of a statutory office at the address of its registered agent or the maintenance of a mailing address; or

(ii)the mere ownership of shares of stock of corporations doing business in the City.

Under Administrative Code Section 11-

meaning of the Internal Revenue Code §864(b)(2)(A) or §864(b)(2)(B).

For purposes of the Business Corporation Tax, an alien corporation that under any pro- vision of the Internal Revenue Code is not treatedasa“domesticcorporation”asdefined in IRC §7701 and has no effectively con- nected income for the taxable year pursuant toclause(iii)oftheopeningparagraphofAd-

NOTE: For additional guidance concerning what activities constitute "doing business," "employing capital," "owning or leasing property," and "maintaining an office" in New York City, see Sections

REFUNDS: If a corporation has previously paid tax or made estimated tax payments for the taxable year and is filing this form dis- claiming liability for those taxes, the corpo- ration should file a refund claim and attach this form to that claim.