nThis is a generic form that may be used to file a Petition for Reassessment for any tax. For purposes of these instructions, all assessment notices are covered by the term “assessment,” regardless of their technical title.

nIMPORTANT: Because different taxes have different filing deadlines, you may safely file this form NO LATER THAN 60 DAYS from the date found on the assessment and you will be timely regardless of the type of tax assessed.

nLaws relating to particular types of assessments are located in Title 57 of the Ohio Revised Code. You are responsible for complying with all of the requirements of the law. (The on-line link to the Revised

Code is available at tax.ohio.gov. Go to the “Tax Professionals” tab, then to the heading “Laws/Rules/Rulings.”)

Section-by-Section Instructions

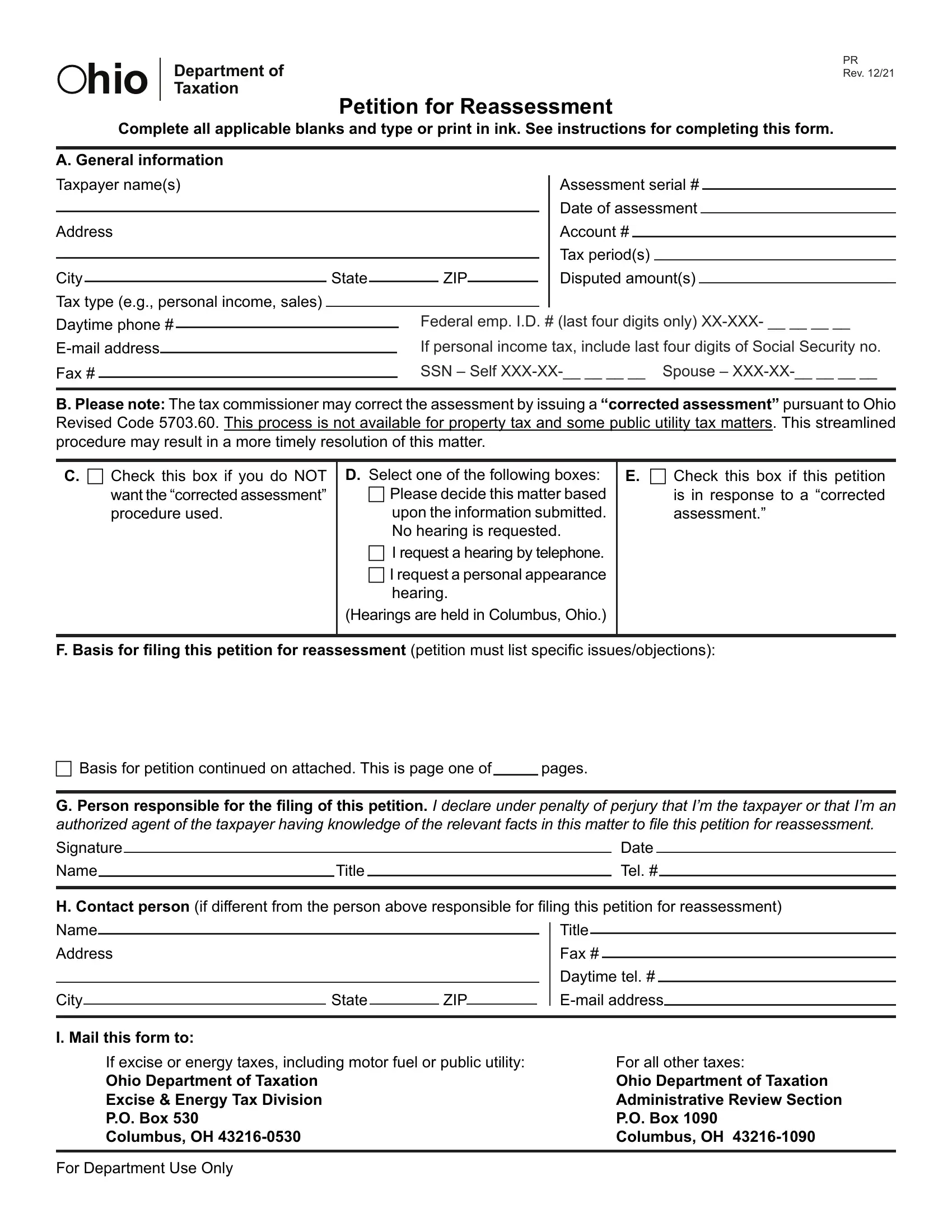

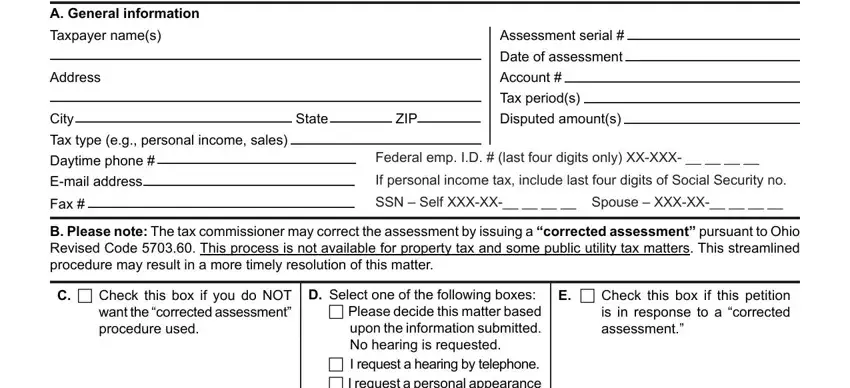

A.General Information

nMost of the information that you need to complete this section can be found on the assessment. Please use it as a reference.

nDaytime phone: Please provide the number where you can be reached during business hours.

nE-mail address: Providing your e-mail address will allow us to communicate with you efficiently and discreetly.

nAssessment serial number: This number is listed on the assessment. It is not applicable for personal property, dealer intangibles or public utility tax assessments.

nDate of assessment: The date found on the assessment document.

nTax period(s): List the periods or the tax year(s) assessed.

nDisputed amount: The portion of the assessment that you are

protesting. Usually, this amount does not need to be paid before this petition is filed. However, there are exceptions. For example, when only the penalty or interest is being protested in the corporate franchise tax or personal income tax, payment of tax and interest (but not penalty) is required.

B. Corrected Assessment is NOT available for property and public

utility assessments (except in R.C. 5727.26 and R.C. 5727.89).

nWhat is a “corrected assessment”? According to R.C. 5703.60, when a petition for reassessment has been properly filed, the Tax

Commissioner may respond by issuing a “corrected assessment.”

This is a more streamlined response to the petition than a final determination and it may both simplify and expedite resolution of the

matter. The Notice of Corrected Assessment does not contain the legal analysis of the tax commissioner. Only a final determination

(not a corrected assessment) can be appealed to the Board of Tax Appeals or Ohio courts.

nWhat if the taxpayer disagrees with the “corrected assessment”?

If a corrected assessment is issued and the taxpayer disagrees with the result, the taxpayer still has the option of filing a new petition

for reassessment protesting the “corrected assessment.” This same form is used to file a petition in response to a corrected assessment.

In response to this new petition, the Tax Commissioner will issue a final determination.

nWhat if the taxpayer fails to file a NEW petition for reassessment

after receiving a “corrected assessment”? According to R.C.

5703.60, the issuance of a corrected assessment nullifies the original petition for reassessment and the original petition is not subject to

further administrative review or appeal. Therefore, the corrected assessment becomes final.

C. In Order to Request That the “Corrected Assessment” Procedure NOT Be Used CHECK THE BOX

nIf this box is checked, a final determination will be issued and the streamlined procedure will not be used.

D. Select a Box (If a corrected assessment is issued, THERE WILL BE NO HEARING, even if you requested one.)

nNo hearing: All of your information will be carefully reviewed and considered, but you will not have to participate in a hearing.

nHearing by telephone: This is an informal discussion to gather facts and listen to the taxpayer’s (or representative’s) legal arguments.

You may submit information. Please number your pages and retain a duplicate for yourself so that specific documentation can be reviewed and discussed during the hearing. You may use a conference call to include your representative or anyone else you choose.

nPersonal appearance hearing: This is an informal face-to-face meeting centered on gathering facts and listening to the taxpayer’s (or representative’s) legal arguments. This is also the taxpayer’s opportunity to present any documentation for review and discussion.

E.Petition in Response to a “Corrected Assessment”

nIf you have already received a “corrected assessment” and you are filing this petition because you disagree with the adjusted amount on the “corrected assessment,” CHECK THE BOX.

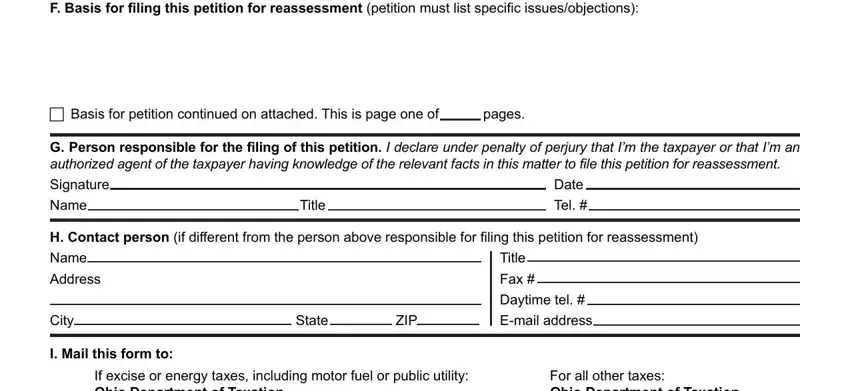

F.Basis for Filing this Petition for Reassessment

nPlease list all of the reasons that you think the Ohio Department

of Taxation erred when it issued the assessment or the corrected assessment. You must be specific with your objections. However,

you are free to present your case in the manner of your choice.

You may make legal arguments. You may cite specific sections of

the Ohio Revised Code or the Ohio Administrative Code. You may reference and attach specific court or Board of Tax Appeals cases.

You may attach photographs or include any other documentation. You are not limited. You may attach additional pages, but please CHECK THE BOX and list the total.

G. Person Responsible for Filing this Petition

nName/title: This is the individual vouching for the accuracy of the information presented. This person should be familiar with all of the facts and issues related to this matter. This may be the individual

petitioner, an employee or owner of the business, or the person designated as the representative. Whoever is responsible for filing this request must provide their signature, name, title, date and phone number.

H. Contact Person (Information required ONLY if different from the “Person Responsible for Filing this Petition.”)

nThis may be the individual petitioner, an employee or owner of the business, or a separate person chosen to be the representative. A representative does not need to be an attorney or an accountant, but the petitioner must authorize them.

nIf the contact person is the taxpayer’s representative, the taxpayer needs to complete form TBOR 1 and return it along with this petition. Form TBOR 1 authorizes the contact person to represent the claimant and allows the Ohio Department of Taxation to talk to this person. (An on-line link is available at tax.ohio.gov. Go to the “Tax Professionals” tab, then to the heading “Taxpayer Representation.”)

I.Mail This Form To:

nDifferent taxes must be mailed to different addresses. If in doubt use the address provided for “all other taxes.”

nThe petition may be hand delivered to:

– 4485 Northland Ridge Blvd., Columbus, OH 43229