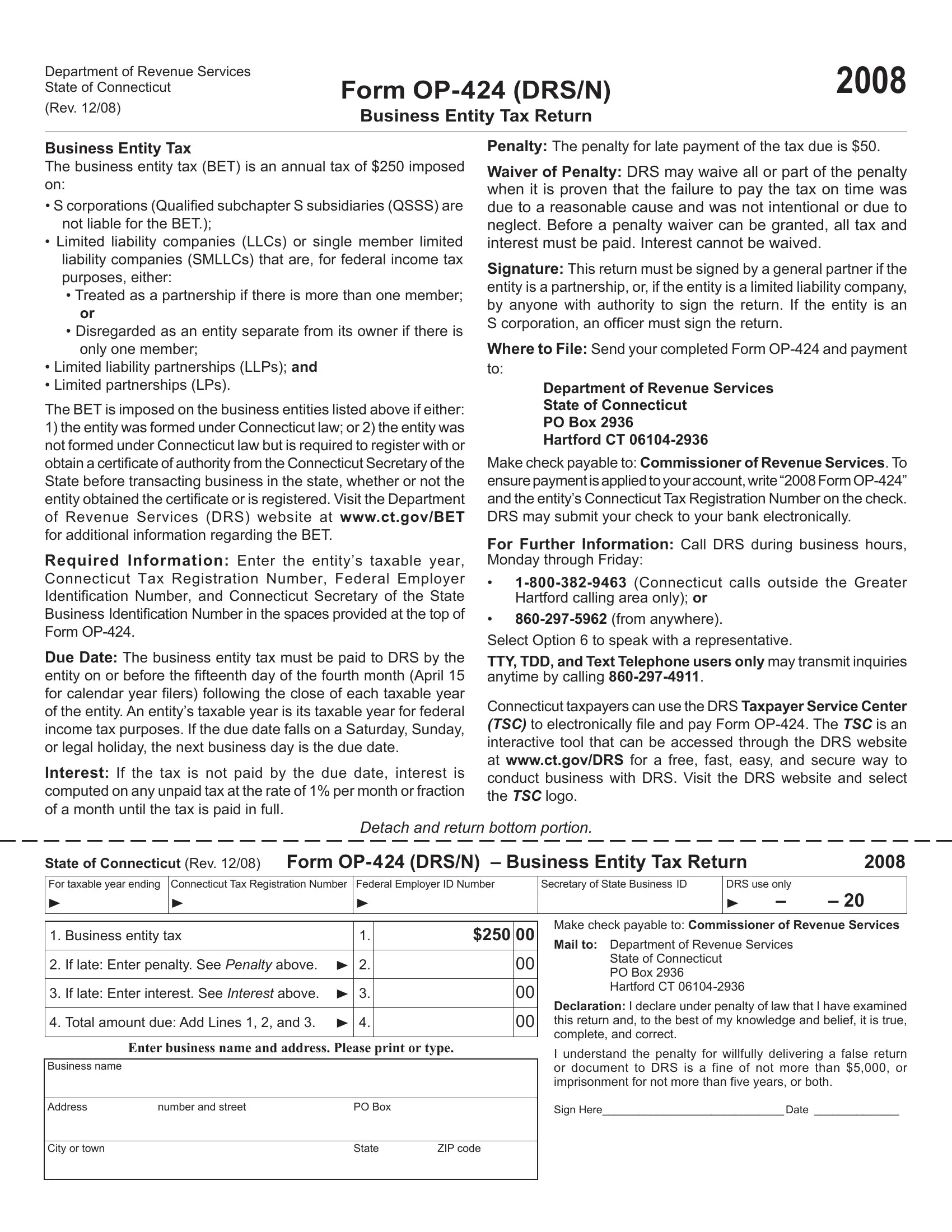

The Form OP-424, issued by the Connecticut Department of Revenue Services, serves as a cornerstone for entities operating within the state to comply with the annual Business Entity Tax (BET) requirement. This tax, set at $250, casts a wide net, encompassing S corporations, Limited Liability Companies (LLCs), including single member LLCs, Limited Liability Partnerships (LLPs), and Limited Partnerships (LPs), provided they meet specific criteria related to their formation under Connecticut law or their necessity to register for conducting business in the state. The delineation of entities liable for this tax reflects the state's approach to ensure a broad spectrum of business structures contribute to the fiscal responsibilities tied to their operations within Connecticut. Entities looking to navigate the compliance landscape must furnish detailed information including their taxable year, Connecticut Tax Registration Number, Federal Employer Identification Number, and Connecticut Secretary of the State Business Identification Number. The mechanism for enforcing this compliance includes a penalty for late payment and provisions for a waiver under circumstances deemed reasonable. Moreover, the form must be duly signed by an authorized individual, which varies depending on the nature of the entity. With deadlines firmly set and specific instructions for where and how to file, including electronic filing options through the Taxpayer Service Center (TSC), the form provides a structured framework for entities to affirm their fiscal commitments to the state. Additionally, guidance and support resources are made available, emphasizing the state's initiative to facilitate compliance while upholding the integrity of the taxation process.

| Question | Answer |

|---|---|

| Form Name | Op 424 Form |

| Form Length | 1 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 15 sec |

| Other names | form op 424 business entity tax return, file ct op 424 online, form op 424 ct, form op 424 connecticut 2018 |

Department of Revenue Services State of Connecticut

(Rev. 12/08)

Form |

2008 |

Business Entity Tax Return |

|

Business Entity Tax

The business entity tax (BET) is an annual tax of $250 imposed on:

•S corporations (Qualified subchapter S subsidiaries (QSSS) are not liable for the BET.);

•Limited liability companies (LLCs) or single member limited liability companies (SMLLCs) that are, for federal income tax purposes, either:

•Treated as a partnership if there is more than one member; or

•Disregarded as an entity separate from its owner if there is only one member;

•Limited liability partnerships (LLPs); and

•Limited partnerships (LPs).

The BET is imposed on the business entities listed above if either:

1)the entity was formed under Connecticut law; or 2) the entity was not formed under Connecticut law but is required to register with or obtain a certificate of authority from the Connecticut Secretary of the State before transacting business in the state, whether or not the entity obtained the certificate or is registered. Visit the Department of Revenue Services (DRS) website at www.ct.gov/BET for additional information regarding the BET.

Required Information: Enter the entity’s taxable year, Connecticut Tax Registration Number, Federal Employer Identification Number, and Connecticut Secretary of the State Business Identification Number in the spaces provided at the top of Form

Penalty: The penalty for late payment of the tax due is $50.

Waiver of Penalty: DRS may waive all or part of the penalty when it is proven that the failure to pay the tax on time was due to a reasonable cause and was not intentional or due to neglect. Before a penalty waiver can be granted, all tax and interest must be paid. Interest cannot be waived.

Signature: This return must be signed by a general partner if the entity is a partnership, or, if the entity is a limited liability company, by anyone with authority to sign the return. If the entity is an S corporation, an offi cer must sign the return.

Where to File: Send your completed Form

Department of Revenue Services

State of Connecticut

PO Box 2936

Hartford CT

Make check payable to: Commissioner of Revenue Services. To

For Further Information: Call DRS during business hours, Monday through Friday:

•

•

Select Option 6 to speak with a representative.

Due Date: The business entity tax must be paid to DRS by the entity on or before the fifteenth day of the fourth month (April 15 for calendar year filers) following the close of each taxable year of the entity. An entity’s taxable year is its taxable year for federal income tax purposes. If the due date falls on a Saturday, Sunday, or legal holiday, the next business day is the due date.

Interest: If the tax is not paid by the due date, interest is computed on any unpaid tax at the rate of 1% per month or fraction of a month until the tax is paid in full.

TTY, TDD, and Text Telephone users only may transmit inquiries anytime by calling

Connecticut taxpayers can use the DRS Taxpayer Service Center (TSC) to electronically file and pay Form

Detach and return bottom portion.

State of Connecticut (Rev. 12/08) Form |

2008 |

For taxable year ending Connecticut Tax Registration Number Federal Employer ID Number

Secretary of State Business ID

DRS use only

–– 20

1. |

Business entity tax |

1. |

$250 |

00 |

|

|

|

|

|

2. |

If late: Enter penalty. See Penalty above. |

2. |

|

00 |

|

|

|

|

|

3. |

If late: Enter interest. See Interest above. |

3. |

|

00 |

|

|

|

|

|

4. |

Total amount due: Add Lines 1, 2, and 3. |

4. |

|

00 |

|

|

|

|

|

Enter business name and address. Please print or type.

Business name

Address |

number and street |

PO Box |

|

|

|

|

|

City or town |

|

State |

ZIP code |

Make check payable to: Commissioner of Revenue Services

Mail to: Department of Revenue Services

State of Connecticut

PO Box 2936

Hartford CT

Declaration: I declare under penalty of law that I have examined this return and, to the best of my knowledge and belief, it is true, complete, and correct.

I understand the penalty for willfully delivering a false return or document to DRS is a fine of not more than $5,000, or imprisonment for not more than fi ve years, or both.

Sign Here______________________________ Date ______________