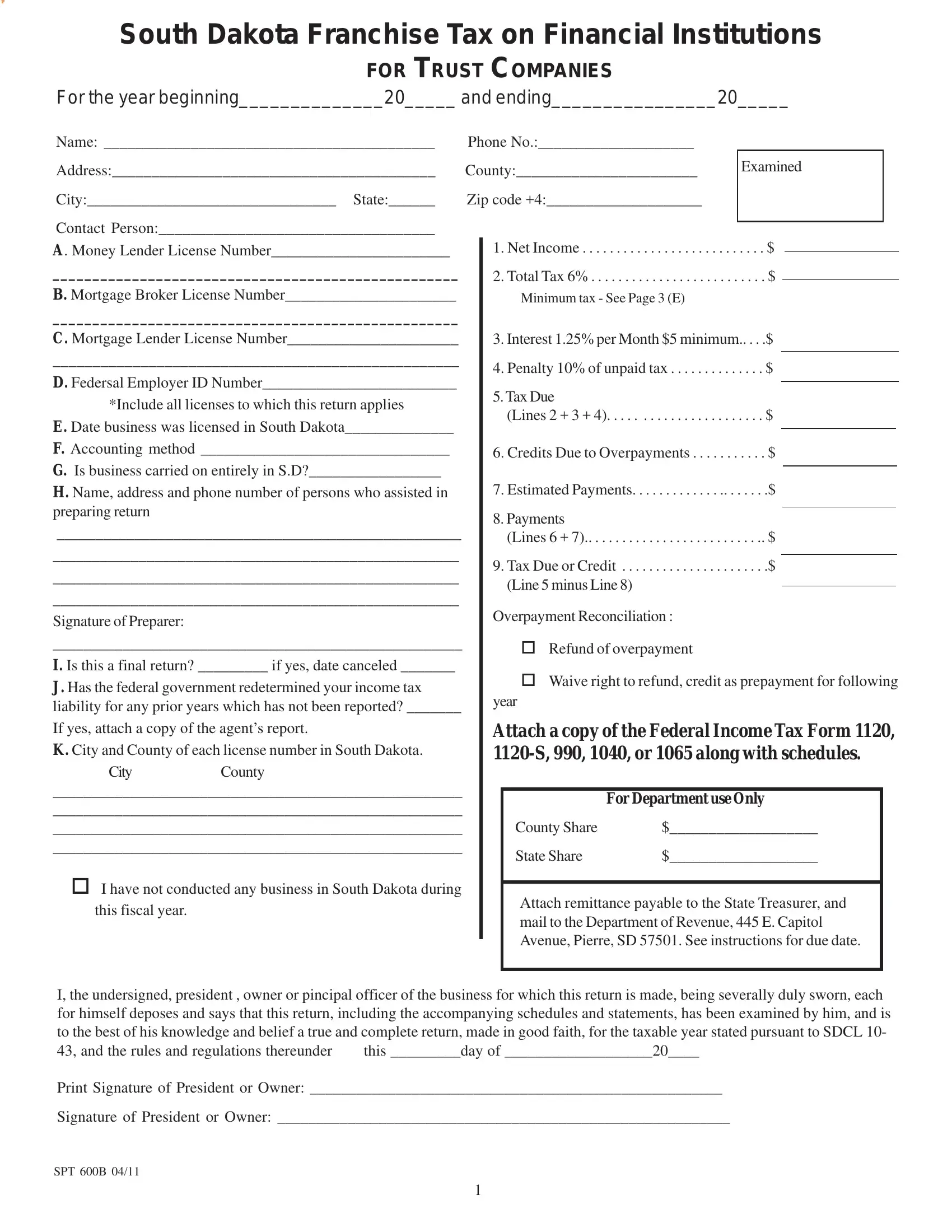

The SPT 600B form plays a crucial role for trust companies operating within South Dakota, as it pertains to the Franchise Tax on Financial Institutions. This comprehensive form addresses essential details for the tax year, including the period of operation, company name, address, contact information, and various license numbers pertinent to money lending, mortgage brokerage, and more. Furthermore, it requires the reporting of the Federal Employer ID Number, the date the business was licensed in South Dakota, the accounting method employed, and whether the business operations are confined within the state. The form also probes into whether this is the final return due to business cessation, any adjustments in federal income tax liability not yet reported, and specifics regarding the location of each license number across South Dakota. Beyond the mere collection of data, the SPT 600B form delves into financial intricacies such as net income, applicable taxes, penalties, and estimated payments, alongside directives for attaching the Federal Income Tax Form (1120, 1120-S, 990, 1040, or 1065) with schedules. Accurate completion ensures compliance with state tax obligations, reflecting the dual importance of precision in reporting and the role of this form in fulfilling fiscal responsibilities towards the state of South Dakota.

| Question | Answer |

|---|---|

| Form Name | Spt 600B Form |

| Form Length | 6 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min 30 sec |

| Other names | south dakota bank franchise tax form, 15th, M-1, SDCL |