The State 10068 form, officially known as the Business Tangible Personal Property Return, serves as a critical document for business owners across various sectors. Designed by the Department of Local Government Finance and known by its form number 104, it plays an essential role in the tax assessment process, ensuring that all tangible personal property owned, held, or used in a business is accounted for appropriately. This form is not confidential and stands open for public inspection, emphasizing transparency in the declaration of assets. Filing this form, which must occur annually by May 15 or by a later date if a written extension is granted, requires meticulous attention to detail. Businesses must declare all tangible personal property, with adjustments made by assessors and possibly by the County Board, leading to the final assessed value which forms the basis for the calculation of property taxes. In addition to the main form, attachments like Form 102 or Form 103 are necessary, providing a comprehensive overview of the property held. Penalties for non-compliance or inaccuracies are steep, underlining the importance of a thorough and accurate filing process. The form also accommodates changes or improvements made to real estate, ensuring that all relevant fiscal responsibilities are up-to-date. With its crucial role in the financial and regulatory landscape, understanding and accurately completing the State 10068 form is indispensable for businesses aiming to fulfill their property tax obligations effectively.

| Question | Answer |

|---|---|

| Form Name | State Form 10068 |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | indiana form 104 2019, 103-CTP, business tangible personal property return form 104, preparer |

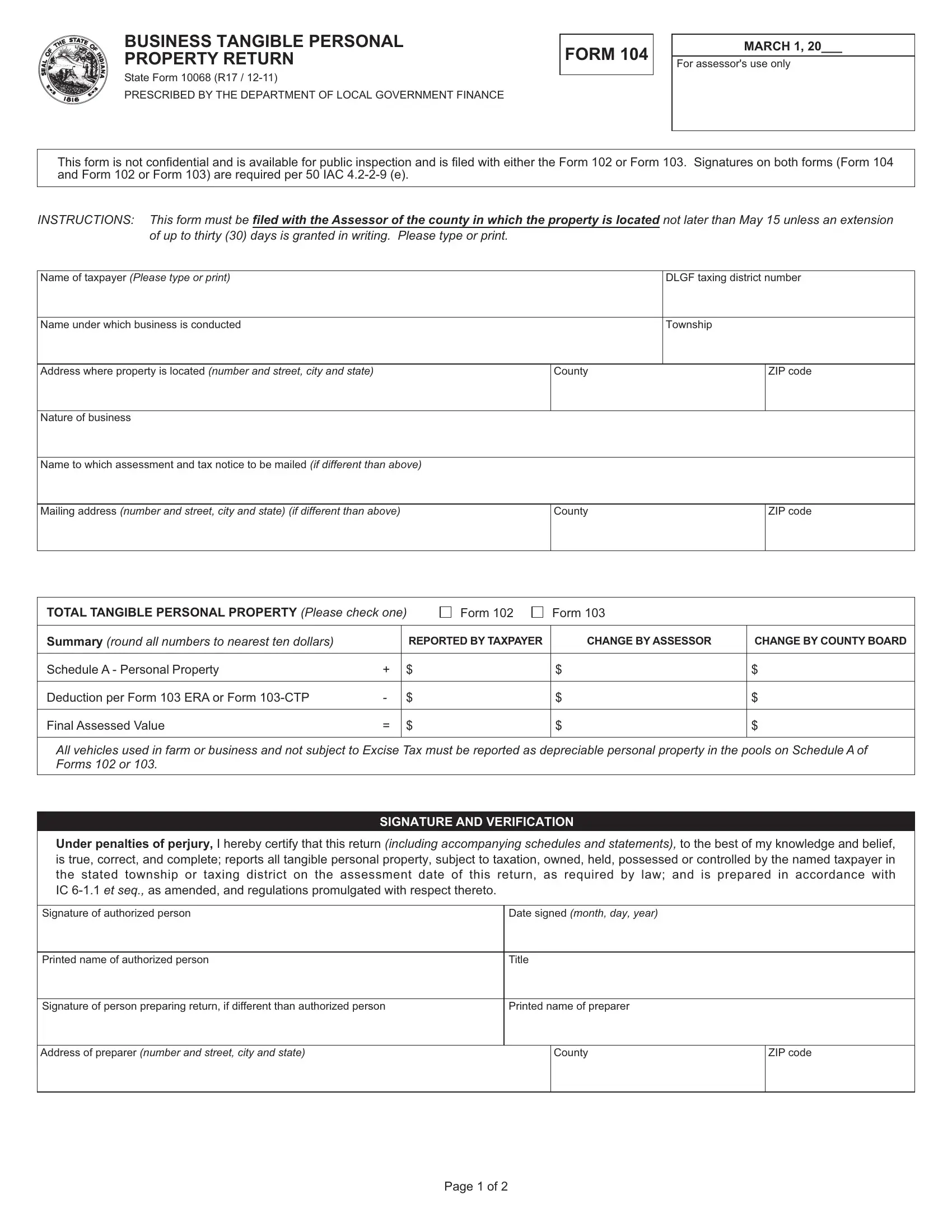

BUSINESS TANGIBLE PERSONAL

PROPERTY RETURN

State Form 10068 (R17 /

PRESCRIBED BY THE DEPARTMENT OF LOCAL GOVERNMENT FINANCE

FORM 104

MARCH 1, 20___

For assessor's use only

This form is not confidential and is available for public inspection and is filed with either the Form 102 or Form 103. Signatures on both forms (Form 104 and Form 102 or Form 103) are required per 50 IAC

INSTRUCTIONS: This form must be filed with the Assessor of the county in which the property is located not later than May 15 unless an extension of up to thirty (30) days is granted in writing. Please type or print.

Name of taxpayer (Please type or print) |

|

DLGF taxing district number |

|

|

|

|

|

Name under which business is conducted |

|

Township |

|

|

|

|

|

Address where property is located (number and street, city and state) |

County |

|

ZIP code |

|

|

|

|

Nature of business |

|

|

|

|

|

|

|

Name to which assessment and tax notice to be mailed (if different than above) |

|

|

|

|

|

|

|

Mailing address (number and street, city and state) (if different than above) |

County |

|

ZIP code |

|

|

|

|

TOTAL TANGIBLE PERSONAL PROPERTY (Please check one) |

Form 102 |

Form 103 |

|

||

|

|

|

|

|

|

Summary (round all numbers to nearest ten dollars) |

|

REPORTED BY TAXPAYER |

CHANGE BY ASSESSOR |

CHANGE BY COUNTY BOARD |

|

|

|

|

|

|

|

Schedule A - Personal Property |

+ |

$ |

|

$ |

$ |

|

|

|

|

|

|

Deduction per Form 103 ERA or Form |

- |

$ |

|

$ |

$ |

|

|

|

|

|

|

Final Assessed Value |

= |

$ |

|

$ |

$ |

|

|

|

|

|

|

All vehicles used in farm or business and not subject to Excise Tax must be reported as depreciable personal property in the pools on Schedule A of Forms 102 or 103.

SIGNATURE AND VERIFICATION

Under penalties of perjury, I hereby certify that this return (including accompanying schedules and statements), to the best of my knowledge and belief, is true, correct, and complete; reports all tangible personal property, subject to taxation, owned, held, possessed or controlled by the named taxpayer in the stated township or taxing district on the assessment date of this return, as required by law; and is prepared in accordance with IC

Signature of authorized person |

Date signed (month, day, year) |

|

|

|

|

|

|

Printed name of authorized person |

Title |

|

|

|

|

|

|

Signature of person preparing return, if different than authorized person |

Printed name of preparer |

|

|

|

|

|

|

Address of preparer (number and street, city and state) |

|

County |

ZIP code |

|

|

|

|

Page 1 of 2

FILING REQUIREMENTS

Property in more than one Taxing District - Due to varying tax rates, a taxpayer who has property in two or more taxing districts within the same township must file separate returns in each district covering only property located in that district. [IC

Duplicate Return Requirement - Every taxpayer whose total combined assessed value of business personal property within a single taxing district is $150,000 or more must file each return in duplicate including the confidential returns and schedule attached thereto. See 50 IAC

Total assessed value of business personal property filed in this taxing district is: |

$150,000 or more |

Less than $150,000 |

Were expenditures made since March 1 of last year for improvements on any real estate owned, held, possessed, controlled or occupied by the taxpayer

in the township wherein this return is filed? |

Yes |

No |

If Yes, attach a statement setting forth: Name of owner, location of real estate and explaining nature, cost, date construction of improvements was begun and date construction was completed. If not completed as of March 1, state the percentage completed at that time. (IC

PENALTIES FOR FAILURE TO FILE COMPLETE AND ACCURATE FORMS

Failure to file a return on or before the date, as required by law, will result in the imposition of a

If the total assessed value that a person reports on a personal property return is less than the total assessed value that the person is required by law to report and if the amount of the undervaluation exceeds five percent (5%) of the value that should have been reported on the return, then the county auditor shall add a penalty of twenty percent (20%) of the additional taxes finally determined to be due as a result of the undervaluation.

In completing a personal property return for a year, a taxpayer must make a complete disclosure of all information relating to the value, nature or location of personal property owned, held, possessed or controlled on the assessment date [IC

The above penalties are due on the property tax installment next due for the return, whether or not an appeal is filed with the Indiana Tax Court with respect to the tax due on that installment. [IC

Page 2 of 2