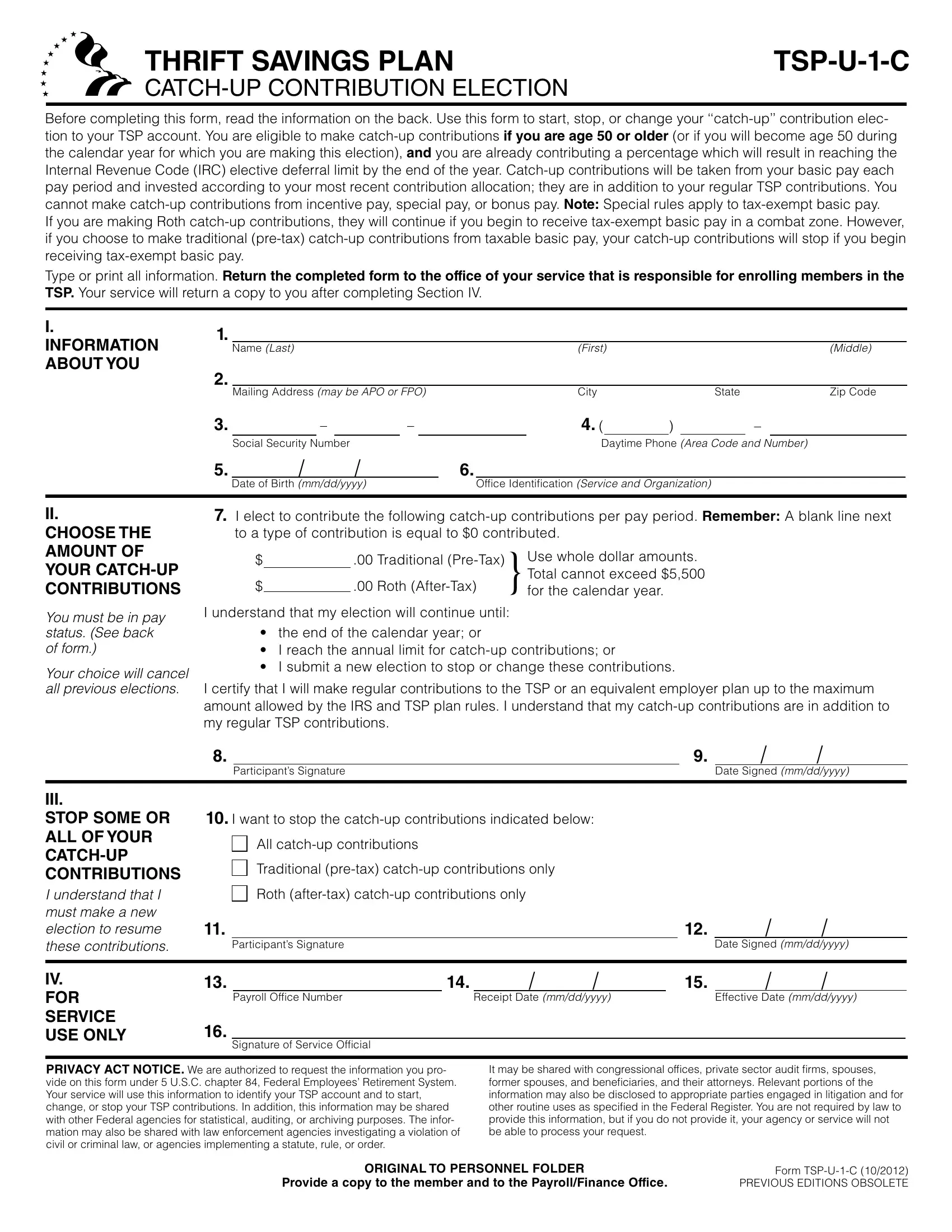

Understanding the nuances of optimizing retirement savings is essential for federal employees, and the Thrift Savings Plan (TSP) U-1-C Catch-Up Contribution Election form serves as a vital tool in this endeavor. Designed for individuals who are 50 years of age or older, or who will reach 50 during the calendar year, this form facilitates the start, stop, or modification of catch-up contributions to their TSP account. These contributions are over and above the regular TSP contributions, specifically targeting those already on course to max out their standard annual contributions under the Internal Revenue Code (IRC) elective deferral limits. It's crucial to recognize that catch-up contributions, focusing on basic pay, exclude incentive, special, or bonus pays, with distinct stipulations applied to tax-exempt basic pay in combat zones, especially concerning Roth contributions. The completion and submission of this form to the appropriate service office kick-start the processing, which, upon approval, aids in bolstering one's retirement savings, aligning with the most recent contribution allocation choices. This process underlines the importance of meticulous planning and elections regarding traditional (pre-tax) and Roth (after-tax) catch-up contributions, emphasizing the resilience and adaptability required to navigate through the intricacies of retirement savings enhancement.

| Question | Answer |

|---|---|

| Form Name | Tsp U 1 C Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | tsp u 1 c vs tsp u 1, tsp u 1 fillable form, tsp u 1 c, tsp u 1 c 2020 fillable |

THRIFT SAVINGS PLAN |

Before completing this form, read the information on the back. Use this form to start, stop, or change your

If you are making Roth

Type or print all information. Return the completed form to the office of your service that is responsible for enrolling members in the TSP. Your service will return a copy to you after completing Section IV.

I. |

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (Last) |

|

|

|

|

|

(First) |

|

|

|

(Middle) |

|||||

ABOUT YOU |

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mailing Address (may be APO or FPO) |

|

|

City |

|

State |

|

Zip Code |

|||||||

|

3. |

|

– |

|

|

– |

|

|

4. ( |

|

) |

|

– |

|

||

|

|

Social Security Number |

|

|

|

|

|

Daytime Phone (Area Code and Number) |

||||||||

|

5. |

/ |

|

|

/ |

|

|

6. |

|

|

|

|

|

|

|

|

|

|

Date of Birth (mm/dd/yyyy) |

|

Office Identification (Service and Organization) |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

II.

CHOOSE THE

AMOUNT OF YOUR

You must be in pay status. (See back of form.)

Your choice will cancel all previous elections.

7.I elect to contribute the following

$ |

.00 |

Traditional |

Use whole dollar amounts. |

|

|

|

|

|

Total cannot exceed $5,500 |

$ |

|

.00 |

Roth |

}for the calendar year. |

|

||||

I understand that my election will continue until:

•the end of the calendar year; or

•I reach the annual limit for

•I submit a new election to stop or change these contributions.

I certify that I will make regular contributions to the TSP or an equivalent employer plan up to the maximum amount allowed by the IRS and TSP plan rules. I understand that my

8. |

|

9. |

/ |

/ |

|

Participant’s Signature |

|

Date Signed (mm/dd/yyyy) |

|

|

|

|

|

|

III.

STOP SOME OR ALL OF YOUR

I understand that I must make a new election to resume these contributions.

10.I want to stop the

All

Traditional

Roth

11. |

|

12. |

/ |

/ |

|

Participant’s Signature |

|

Date Signed (mm/dd/yyyy) |

|

IV. |

13. |

|

14. |

/ |

/ |

15. |

/ |

/ |

|

FOR |

|

Payroll Office Number |

|

Receipt Date (mm/dd/yyyy) |

|

Effective Date (mm/dd/yyyy) |

|

||

SERVICE |

16. |

|

|

|

|

|

|

|

|

USE ONLY |

|

|

|

|

|

|

|

|

|

Signature of Service Official |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PRIVACY ACT NOTICE. We are authorized to request the information you pro- vide on this form under 5 U.S.C. chapter 84, Federal Employees’ Retirement System. Your service will use this information to identify your TSP account and to start, change, or stop your TSP contributions. In addition, this information may be shared with other Federal agencies for statistical, auditing, or archiving purposes. The infor- mation may also be shared with law enforcement agencies investigating a violation of civil or criminal law, or agencies implementing a statute, rule, or order.

It may be shared with congressional offices, private sector audit firms, spouses, former spouses, and beneficiaries, and their attorneys. Relevant portions of the information may also be disclosed to appropriate parties engaged in litigation and for other routine uses as specified in the Federal Register. You are not required by law to provide this information, but if you do not provide it, your agency or service will not be able to process your request.

ORIGINAL TO PERSONNEL FOLDER |

Form |

Provide a copy to the member and to the Payroll/Finance Office. |

PREVIOUS EDITIONS OBSOLETE |

GENERAL INFORMATION

You may start, stop, or change your

Your

SECTION I |

Complete all items in this section. In Item 4, provide your daytime telephone number. |

|

|

SECTION II

Your choice will cancel all previous elections.

Your contribution election. You can elect to make traditional

Contribution limits. The Internal Revenue Code (IRC) limit for

Deductions will be made from your basic pay in the dollar amount you indicate. However:

(1)

(2)The

(3)Your traditional

(4)Your

You are not eligible to make

You may stop your

You must sign this section. If you do not, your request to start or change your

SECTION III |

If you choose to stop all or just one type of your |

|

Your election should be effective the first pay period after your service receives it. You can restart your |

|

contributions at any time, subject to the conditions above. |

|

|

SECTION IV

(To be completed by service official)

The Receipt Date (Item 14) is the date that a properly completed form is received by the office processing the request. If the form has not been properly completed, it should be returned to the service member.

The Effective Date (Item 15) must be no later than the first full pay period after receipt of a properly completed form.

You should provide the participant with a copy of this completed election for his or her records.

Form

PREVIOUS EDITIONS OBSOLETE