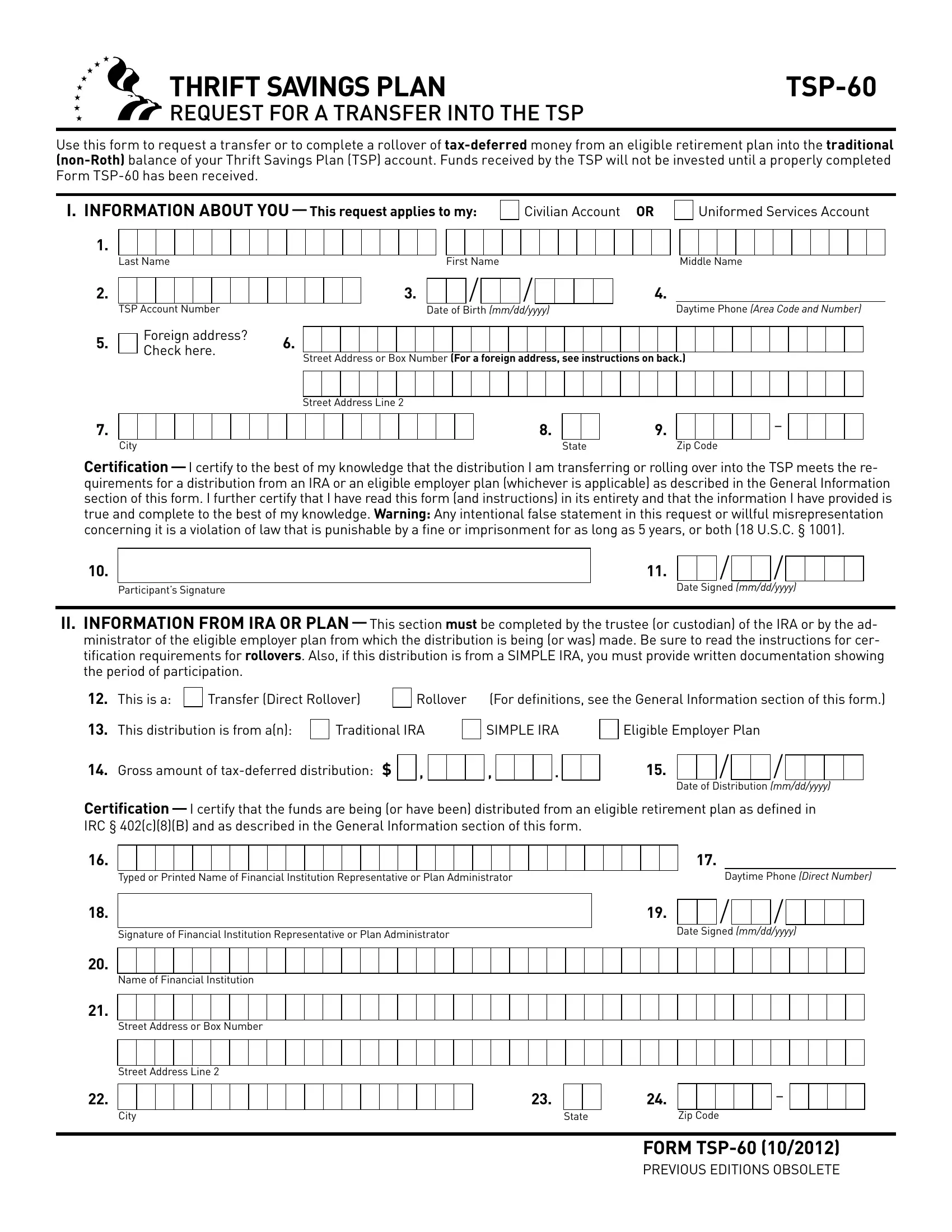

The Thrift Savings Plan (TSP) offers a form known as the TSP-60, which plays a crucial role for participants looking to transfer or roll over tax-deferred money from an eligible retirement plan into the traditional balance of their TSP account. This procedure allows individuals to move funds from various retirement plans, including traditional IRAs, SIMPLE IRAs, and eligible employer plans, into the TSP without facing immediate tax penalties, thus preserving the tax-deferred status of their savings. Highlighting the importance of a correctly completed Form TSP-60, it specifies that the funds will not be invested until the form is properly filled out and submitted, indicating the precision and care required when handling such transfers. The form is divided into two sections: the first gathering information about the participant, including identifying data and certification of eligibility, and the second to be completed by the trustee or administrator of the IRA or plan from which funds are being transferred, ensuring that the rollover meets all necessary legal and regulatory standards. The TSP-60 form outlines the differences between direct rollovers and rollovers, the specifics of what distributions can be moved, and the mechanism by which these funds are incorporated into the participant's TSP account, all of which underscore the complexity and potential benefits of managing one's retirement savings effectively. Additionally, the form and accompanying instructions provide a clear path for individuals to consolidate their retirement savings, potentially simplifying their management and focusing their investment strategy within the TSP framework.

| Question | Answer |

|---|---|

| Form Name | Tsp60 Form |

| Form Length | 4 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 1 min |

| Other names | tsp 60 tsp60 form |

THRIFT SAVINGS PLAN |

Request foR a tRansfeR into the tsp

Use this form to request a transfer or to complete a rollover of

I.INFORMATION ABOUT

Civilian Account OR

Uniformed Services Account

1.

Last Name |

First Name |

Middle Name |

2.

5.

TSP Account Number

Foreign address? Check here.

3. |

|

|

/ |

|

|

/ |

|

|

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime Phone (Area Code and Number) |

|

Date of Birth (mm/dd/yyyy) |

|

|

|

|

|||||||

6.

Street Address or Box Number (For a foreign address, see instructions on back.)

Street Address Line 2

7.

City

8.

State

9.

Zip Code

–

10.

Participant’s Signature

11.//

Date Signed (mm/dd/yyyy)

II.INFORMATION FROM IRA OR

12. |

This is a: |

|

Transfer (Direct Rollover) |

|

|

|

Rollover |

|

||||||

13. |

This distribution is from a(n): |

|

Traditional IRA |

|

|

|

||||||||

|

|

|

|

|||||||||||

14. |

Gross amount of |

|

|

|

|

|

|

|

|

|||||

|

|

, |

|

|

|

|

|

|||||||

(For definitions, see the General Information section of this form.)

SIMPLE IRA |

|

Eligible Employer Plan |

, |

|

|

|

. |

|

|

15. |

|

|

/ |

|

|

/ |

Date of Distribution (mm/dd/yyyy)

Certiication

16.

18.

20.

21.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime Phone (Direct Number) |

||||||||

Typed or Printed Name of Financial Institution Representative or Plan Administrator |

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

|

|

/ |

|

|

|

|

|

|

19. |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||

Signature of Financial Institution Representative or Plan Administrator |

|

|

|

|

Date Signed (mm/dd/yyyy) |

|||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Financial Institution |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street Address or Box Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street Address Line 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

22.

City

23. |

|

|

24. |

|

|

|

|

|

– |

|

State |

Zip Code |

|||||||

FORM

PREVIOUS EDITIONS OBSOLETE

FORM

Use this form to request a transfer or to complete a rollover of

The TSP is a retirement savings and investment plan for Federal employees and members of the uniformed services. Congress established the TSP in the Federal Employees’ Retirement Sys- tem Act of 1986. The TSP is to be treated as a trust described in 26 U.S.C. § 401(a), which is exempt from taxation under 26 U.S.C. § 501(a). TSP regulations are published in title 5 of the Code of Federal Regulations, Parts

You must complete Section I of this form, then provide the entire package to your IRA trustee or plan administrator to complete Section II. If necessary, have your IRA trustee or plan administra- tor return the form to you. In order for your request to be pro- cessed, it must include a completed Form

Note: If you intend to make a full withdrawal, please wait until you receive confirmation that your transfer or rollover has been completed before requesting the withdrawal.

SECTION I. Complete Items

The address on this form cannot be used to update your TSP record.

If you have a foreign address, check the box in Item 5 and enter the foreign address as follows in Items

First address line: Enter the street address or post office box number, and any apartment number.

Second address line: Enter the city or town name, other princi- pal subdivision (e.g., province, state, county), and postal code, if known. (The postal code may precede the city or town.)

City/State/Zip Code fields: Enter the entire country name in the City field; leave the State and Zip Code fields blank.

Read the General Information section of this form, and sign and date Items 10 and 11 if the information is correct. If you cannot certify that your transfer or rollover meets all of the require- ments described, you cannot transfer or roll over your distribu- tion into the TSP.

If you have questions, call the ThriftLine toll free at

Either mail the check and form to:

|

TSP Rollover and Transfer Processing Unit |

|

P.O. Box 385200 |

|

Birmingham, AL |

Or fax to: |

|

|

If you fax this form, please send your check immediately to the TSP.

SECTION II. The instructions for Section II are intended for the IRA or plan representative.

If you are unwilling to complete this section, submit an IRS Letter of Determination or a letter on the organization’s letterhead con- firming that the funds are being transferred (or rolled over) from a qualified plan. Otherwise, we cannot deposit the funds into the participant’s account.

If the distribution is being transferred directly to the TSP, you must mail the completed Form

If the distribution is being rolled over, you must submit a letter (on the organization’s letterhead) or a distribution statement that shows the date and the gross amount of the

Item 12. Check the “Transfer (Direct Rollover)” box if the funds are being transferred directly to the TSP. Check the “Rollover” box if the distribution has been paid to the participant, and he or she is sending a check in the amount of the distribution to the TSP.

Item 13. Check the appropriate box to indicate whether the distri- bution is from a traditional IRA, SIMPLE IRA, or eligible employer plan. Complete this information whether the distribution is be- ing transferred or rolled over. Note: If this distribution is from a SIMPLE IRA, you must provide written documentation showing the period of participation.

Item 14. Indicate the total gross amount of the

Item 15. If this request is for a rollover, provide the date that the distribution was made to the participant.

Items

Form

PREVIOUS EDITIONS OBSOLETE

FORM

Form

If the TSP does not receive a Form

If the TSP receives a check with appropriate identification, but without Form

Be sure to read all of the General Information and Instructions before you complete this form.

What

The TSP will accept both transfers and rollovers of

Before submitting this form, a TSP participant who would like to transfer or roll over money into the TSP should check with a representative of his or her IRA or plan to determine what portion of a distribution (if any) meets the applicable requirements, as described below.

Note: Participants are required to certify in Section I of this form that the distribution they are seeking to transfer or roll over into the TSP meets the applicable requirements. If a par- ticipant cannot sign the certification, the TSP cannot accept the transfer or rollover.

Traditional IRA. This is an individual retirement account de- scribed in IRC § 408(a) or an individual retirement annuity de- scribed in IRC § 408(b). The traditional IRA category does not include a Roth IRA, an inherited IRA, or a Coverdell Education Savings Account (formerly known as an education IRA); distribu- tions from these types of IRAs will not be accepted by the TSP.

The TSP will accept all or a portion of a distribution from a tradi- tional IRA except a distribution that:

•is a minimum distribution required by IRC § 401(a)(9); or

•consists of

SIMPLE IRA. This is a Savings Incentive Match Plan for Employ- ers, an employer sponsored retirement plan available to small businesses. A TSP participant can transfer an amount from a SIMPLE IRA to the TSP, as long as he or she participated in the SIMPLE IRA for at least 2 years. Note: The TSP must receive written documentation showing the period of participation in a

SIMPLE IRA.

Eligible Employer Plan. This is a plan qualified under IRC

§401(a) (including a § 401(k) plan,

To be accepted into the TSP, the distribution from an eligible em- ployer plan must be an “eligible rollover distribution.”

An eligible rollover distribution is a distribution to a participant of all or a portion of his or her account. However, it cannot be:

•one of a series of substantially equal periodic payments made over the life expectancy of the employee (or the joint lives of the employee and designated beneficiary, if appli- cable), or for a period of 10 years or more;

•a minimum distribution required by IRC § 401(a)(9);

•a hardship distribution;

•a plan loan that is deemed to be a taxable distribution be- cause of default; or

•a return of excess elective deferrals.

Examples of eligible rollover distributions include: a lump sum distribution after terminating employment; an

All of the money transferred into the TSP must be money that would have been included in the participant’s gross income for the tax year in which the transfer was made, had the money been distributed without being transferred or rolled over.

What is the difference between a “transfer” and a “rollover”?

A transfer (also known as a “direct rollover”) occurs when the participant instructs the distributing plan to send all or part of his or her eligible rollover distribution directly to the TSP instead of issuing it to the participant.

A rollover occurs when the distributing plan makes a payment to the participant (after withholding the applicable Federal in- come tax) and the participant deposits all or any part of the gross amount of the payment into the TSP within 60 days of receiving it.

Form

PREVIOUS EDITIONS OBSOLETE

FORM

How much

There is no limit to the number of transfers or rollovers of tax- deferred money that a participant can make. A participant can transfer or roll over all or any part of a

Note: Any portion of the distribution that the participant choos- es not to transfer or roll over will be taxed as ordinary income. In addition, if the participant is younger than 59½ at the time of distribution, he or she may have to pay a 10% early withdrawal penalty tax on the amount that was not transferred or rolled over.

How does the IRC annual elective deferral limit affect transfers and rollovers?

Money that is transferred or rolled over into the TSP is not ap- plied to the annual elective deferral limit that is imposed on regu- lar employee contributions.

How does a transfer or rollover affect monthly payments?

If a TSP participant is receiving monthly payments at the time of a transfer or a rollover, the TSP will recalculate the amount or the duration of the monthly payments beginning with the first pay- ment the participant receives in the year following the transfer or rollover. If a participant is receiving payments:

•Of a speciic dollar amount, the recalculation will occur only if the participant transferred $1,000 or more, and only the duration of the payments will be affected. However, if the new duration of the payments is 10 years or more, the payments will no longer be eligible for transfer or rollover, and the tax withholding on the payments may change.

•Based on life expectancy, the recalculation should increase the amount of each payment.

For more information, see the TSP tax notice “Tax Information for TSP Participants Receiving Monthly Payments.”

What happens to the money once it reaches the TSP?

Money that is transferred or rolled over into the TSP is allocated to the TSP investment funds according to the participant’s most current contribution allocation on file. Once the money is depos- ited into the participant’s TSP account, it is treated like employee contributions and will be subject to the same plan rules as all other employee contributions in the account. These rules may be different from the rules of the IRA or plan from which the money was distributed.

When you send us a rollover check, it will be converted into an electronic funds transfer (EFT). We will make an electronic im- age of your check and use the account information on it to debit your bank account electronically for the amount of the check.

Although the debit will be reflected on your bank statement, you will not receive the cancelled check because the original will be destroyed after we image it. If for some technical reason the data from the EFT cannot be processed, we will transmit our imaged copy of your check to your bank.

Note: Because the conditions under which the TSP will accept transfers and rollovers are strict, and there may be tax conse- quences, we recommend that you consult your tax advisor before you move money into the TSP.

What Roth distributions will the TSP accept?

The TSP will only accept transfers of qualified and nonqualified Roth distributions from any applicable retirement plan, as defined in IRC § 402(e)(1), under which an employee may elect to make Roth contributions. An applicable retirement plan includes a plan qualified under IRC § 401(a) (e.g., a 401(k) plan); an IRC § 403(b)

The TSP will not accept rollovers of qualified or nonqualified Roth distributions that have already been paid to you.

If you would like to transfer Roth money into the Roth balance of your TSP account, do not complete this form; instead, complete Form

PRIVACY ACT NOTICE. We are authorized to request the information you provide on this form under 5 U.S.C. chapter 84, Federal Employees’ Retirement System. We will use this information to identify your TSP account and to process your request. In addition, this information may be shared with other Federal agencies for statistical, auditing, or archiving purposes. We may share the information with law enforcement agencies investigating a violation of civil or criminal law, or agencies implementing

a statute, rule, or order. It may be shared with congressional offices, private sector audit firms, spouses, former spouses, and beneficiaries, and their attorneys. We may disclose relevant portions of the information to appropriate parties engaged in litigation and for other routine uses as specified in the Federal Register. You are not required by law to provide this information, but if you do not provide it, we will not be able to process your request.

Form

PREVIOUS EDITIONS OBSOLETE