In an era where understanding and complying with tax regulations are crucial for businesses and individuals alike, the Uniform Sales Tax Certificate form stands out as a fundamental tool in the state of New Mexico. This legal document, which has evolved to accommodate the dynamic nature of commerce and taxation, serves multiple purposes, from facilitating tax-exempt purchases to ensuring businesses adhere to state tax laws. Within the form's framework, various types of Nontaxable Transaction Certificates (NTTCs) are delineated, each catering to specific transactions, such as purchases for resale, manufacturing inputs, and services, as well as special provisions for construction contractors, government entities, and nonprofit organizations, among others. The process demands that buyers or lessees register with the New Mexico Taxation and Revenue Department, complete the necessary application, and comply with departmental regulations to prevent misuse, which could lead to severe penalties including fines or imprisonment. This system not only underscores the importance of fiscal responsibility but also emphasizes the role of due diligence in maintaining the integrity of tax-exempt transactions. Moreover, the introduction of the Taxpayer Access Point (TAP) system for online management of NTTCs highlights the shift towards digital solutions, aiming to streamline the application process while maintaining strict control over tax exemptions, reflecting an effort to balance efficiency with regulatory compliance.

| Question | Answer |

|---|---|

| Form Name | Uniform Sales Tax Certificate Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | multi jurisdiction sales tax form, certificate use, uniform sales and use tax certificate multijurisdictional, uniform sales use tax |

New Mexico Taxation and Revenue Department

P.O Box 5557

Santa Fe, New Mexico

www.tax.newmexico.gov/

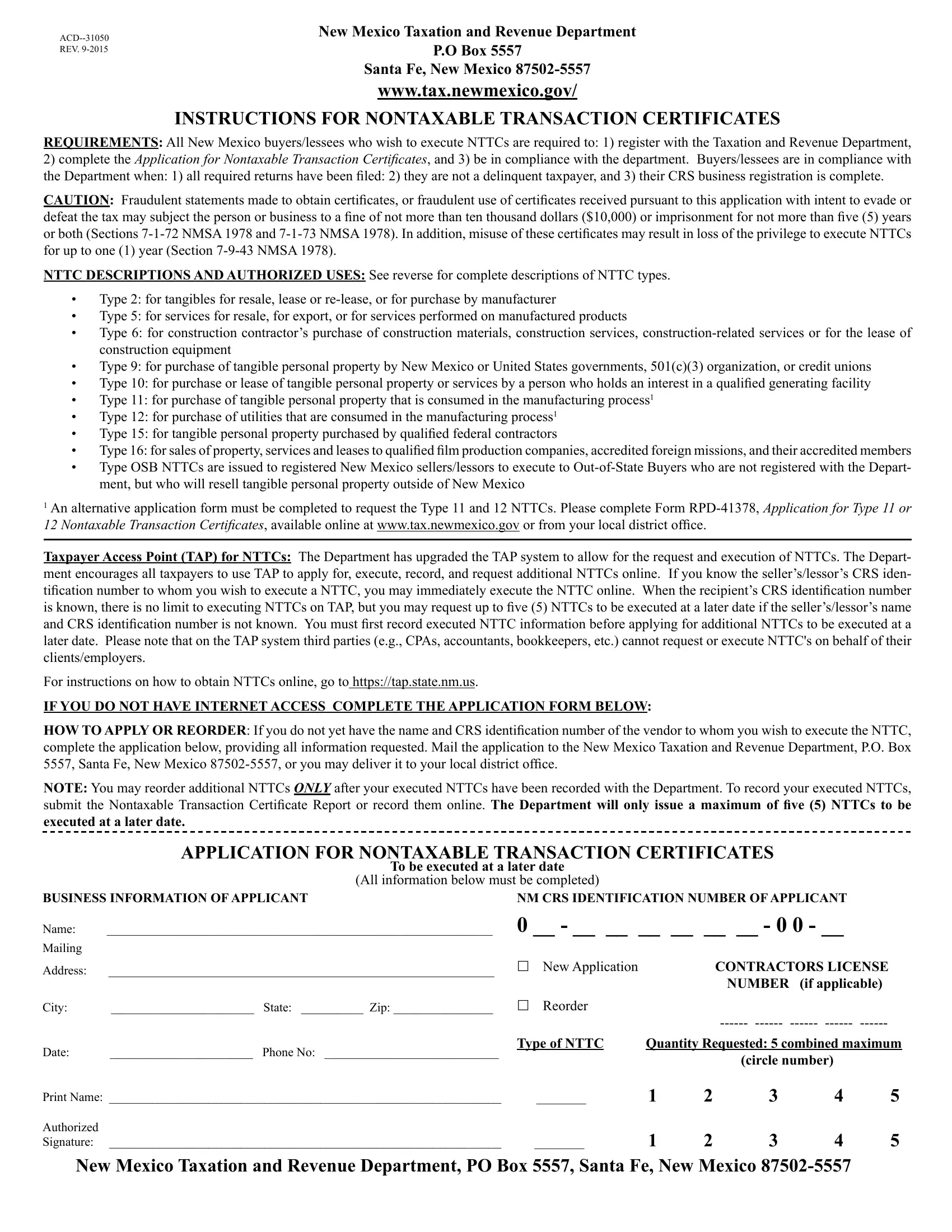

INSTRUCTIONS FOR NONTAXABLE TRANSACTION CERTIFICATES

REQUIREMENTS: All New Mexico buyers/lessees who wish to execute NTTCs are required to: 1) register with the Taxation and Revenue Department,

2)complete the Application for Nontaxable Transaction Certificates, and 3) be in compliance with the department. Buyers/lessees are in compliance with the Department when: 1) all required returns have been filed: 2) they are not a delinquent taxpayer, and 3) their CRS business registration is complete.

CAUTION: Fraudulent statements made to obtain certificates, or fraudulent use of certificates received pursuant to this application with intent to evade or defeat the tax may subject the person or business to a fine of not more than ten thousand dollars ($10,000) or imprisonment for not more than five (5) years or both (Sections

NTTC DESCRIPTIONS AND AUTHORIZED USES: See reverse for complete descriptions of NTTC types.

•Type 2: for tangibles for resale, lease or

•Type 5: for services for resale, for export, or for services performed on manufactured products

•Type 6: for construction contractor’s purchase of construction materials, construction services,

•Type 9: for purchase of tangible personal property by New Mexico or United States governments, 501(c)(3) organization, or credit unions

•Type 10: for purchase or lease of tangible personal property or services by a person who holds an interest in a qualified generating facility

•Type 11: for purchase of tangible personal property that is consumed in the manufacturing process1

•Type 12: for purchase of utilities that are consumed in the manufacturing process1

•Type 15: for tangible personal property purchased by qualified federal contractors

•Type 16: for sales of property, services and leases to qualified film production companies, accredited foreign missions, and their accredited members

•Type OSB NTTCs are issued to registered New Mexico sellers/lessors to execute to

1An alternative application form must be completed to request the Type 11 and 12 NTTCs. Please complete Form

12 Nontaxable Transaction Certificates, available online at www.tax.newmexico.gov or from your local district office.

Taxpayer Access Point (TAP) for NTTCs: The Department has upgraded the TAP system to allow for the request and execution of NTTCs. The Depart- ment encourages all taxpayers to use TAP to apply for, execute, record, and request additional NTTCs online. If you know the seller’s/lessor’s CRS iden- tification number to whom you wish to execute a NTTC, you may immediately execute the NTTC online. When the recipient’s CRS identification number is known, there is no limit to executing NTTCs on TAP, but you may request up to five (5) NTTCs to be executed at a later date if the seller’s/lessor’s name and CRS identification number is not known. You must first record executed NTTC information before applying for additional NTTCs to be executed at a later date. Please note that on the TAP system third parties (e.g., CPAs, accountants, bookkeepers, etc.) cannot request or execute NTTC's on behalf of their

clients/employers.

For instructions on how to obtain NTTCs online, go to https://tap.state.nm.us.

IF YOU DO NOT HAVE INTERNET ACCESS COMPLETE THE APPLICATION FORM BELOW:

HOW TO APPLY OR REORDER: If you do not yet have the name and CRS identification number of the vendor to whom you wish to execute the NTTC, complete the application below, providing all information requested. Mail the application to the New Mexico Taxation and Revenue Department, P.O. Box 5557, Santa Fe, New Mexico

NOTE: You may reorder additional NTTCs ONLY after your executed NTTCs have been recorded with the Department. To record your executed NTTCs, submit the Nontaxable Transaction Certificate Report or record them online. The Department will only issue a maximum of five (5) NTTCs to be

executed at a later date.

APPLICATION FOR NONTAXABLE TRANSACTION CERTIFICATES

To be executed at a later date

(All information below must be completed)

BUSINESS INFORMATION OF APPLICANT |

NM CRS IDENTIFICATION NUMBER OF APPLICANT |

|

||||||

Name: |

______________________________________________________________ |

0 __ - __ __ __ __ __ __ - 0 0 - __ |

|

|||||

Mailing |

|

|

|

|

|

|

|

|

Address: |

______________________________________________________________ |

New Application |

|

|

CONTRACTORS LICENSE |

|||

|

|

|

|

|

|

NUMBER |

(if applicable) |

|

City: |

_______________________ |

State: __________ Zip: ________________ |

Reorder |

|

|

|

||

|

|

|

|

|

|

|

||

Date: |

_______________________ |

Phone No: ____________________________ |

Type of NTTC |

Quantity Requested: 5 combined maximum |

||||

|

|

|

|

|

|

(circle number) |

|

|

Print Name: _______________________________________________________________ |

________ |

1 |

2 |

3 |

4 |

5 |

||

Authorized |

|

|

|

|

|

|

|

|

Signature: |

_______________________________________________________________ |

________ |

1 |

2 |

3 |

4 |

5 |

|

New Mexico Taxation and Revenue Department, PO Box 5557, Santa Fe, New Mexico

NTTC TYPE DESCRIPTIONS 1

TYPE 2 certificates may be executed:

1)By manufacturers for the purchase of tangible personal property that will become an ingredient or component of the manufactured product.

2)For the purchase of tangible personal property or licenses for resale either alone or in combination with other tangible personal property or licenses in the ordinary course of business.

3)By a lessee for the lease of tangible personal property or licenses for subsequent lease in the ordinary course of business, except for the lease of furniture or appliances, the receipts from the rental or lease of which are

deductible under Subsection C of Section

4)For the purchase of tangible personal property or licenses for subsequent lease in the ordinary course of business, except for the lease of furniture or appliances, the receipts from the rental or lease of which are deductible

under Subsection C of Section

5)By a person who is licensed to practice medicine, osteopathic medicine, dentistry, podiatry, optometry, chiropractic or professional nursing for the purchase of prosthetic devices.

6)By a common carrier for the purchase of fuel that is to be loaded or used in a locomotive engine.

TYPE 5 certificates may be executed:

1)For the purchase of services for resale if the subsequent sale by the buyer is in the ordinary course of business and the subsequent sale of the service is subject to gross receipts tax or governmental gross receipts tax.

2)For the purchase of services for export when sold to an

3)By manufacturers for the purchase of services performed directly upon tangible personal property they are in the business of manufacturing or upon ingredient or component parts thereof.

4)For the purchase of aerospace services for resale if the subsequent sale by the buyer is in the ordinary course of business and the services are sold to a 501(c)(3) organization, other than a national laboratory, or to the United States.

TYPE 6 certificates may be executed by a construction contractor:

1)For the purchase of construction materials that will become ingredients or components of a construction project that is either subject to gross receipts tax upon completion or that takes place on Indian tribal territory.

2)For the purchase of construction services that are directly contracted for or billed to a construction project that is either subject to gross receipts tax upon completion, upon the sale in the ordinary course of business of the real property upon which the project is constructed or that takes place on Indian tribal territory.

3)For the purchase of

Indian tribal territory.

4)For the lease of construction equipment that is used at the construction location of a construction project that is either subject to gross receipts tax upon completion, upon the sale in the ordinary course of business of the real property upon which the project is constructed or that takes place on Indian tribal territory.

TYPE 9 certificates may be executed for the purchase of tangible personal property only and may NOT be used for the purchase of services, the pur- chase of a license or other intangible property, for the lease of property or to purchase construction materials for use in construction projects (except as provided in #2 below). The following may execute Type 9 NTTCs:

1)Governmental agencies.

2)501(c)(3) organizations.

Taxation and Revenue Department and submit proof of Internal Revenue Service 501(c)(3) nonprofit determination before they may execute Type 9

NTTCs. Those 501(c)(3) organizations that are organized for the purpose of providing homeownership opportunities to

3)Federal or

4)Indian tribes, nations or pueblos when purchasing tangible personal property for use on Indian reservations or pueblo grants.

TYPE 10 certificates may be executed by a person that holds an interest in a qualified generating facility for the purchase or lease of tangible personal

property or services that are eligible generation plant costs. In addition to required reporting on the

Advanced Energy Deduction.

TYPE 11 certificates may be executed by manufactures for the purchase of tangible personal property that will be consumed in the manufacturing process and may not be used to purchase tools or equipment that may be used to create the manufactured product. The Type 11 NTTC is not to be used for the purchase of utilities.

TYPE 12 certificates may be executed by manufactures for the purchase of utilities that will be consumed in the manufacturing process.

TYPE 16 certificates may be executed by:

1)Qualified film production companies to purchase property, lease property or purchase services. A qualified production company must submit proof of registration with the New Mexico Film Division of the Economic Development Department.

2)Accredited diplomats or missions for the purchase of property or services or the leasing of property.

TYPE

1

2

3

For more information on the use of different types of NTTCs and special reporting requirements please see publication

at

Proof that a construction contractor's license is not required includes a detailed written statement explaining the circumstances that exclude the contractor from the jurisdiction

or application of New Mexico statutes which provide for construction contractor's licensing and regulation of construction activity.

Type 11 and 12 NTTCs require the completion of an alternative application, Form