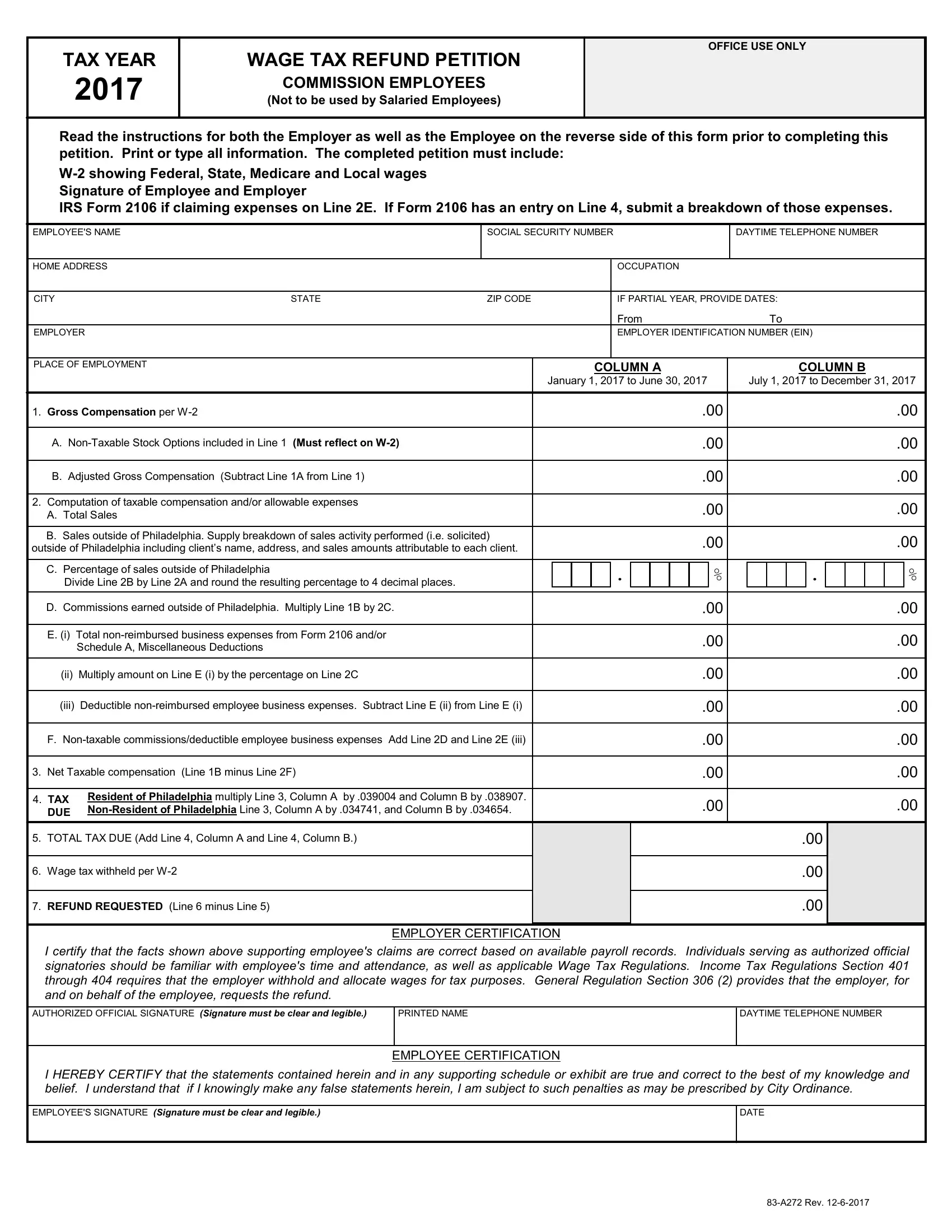

Filing for a Wage Tax Refund is a critical process for commission employees who believe they have overpaid on their taxes, and the Wage Tax Refund Petition form serves as their primary tool in submitting such claims for the tax year 2017. This detailed form, designed explicitly for commission employees and not for those on a salaried basis, necessitates careful attention to complete accurately. It requires pertinent information such as the employee's personal details, employment data, and a comprehensive breakdown of earnings both within and outside of Philadelphia. Moreover, it mandates the attachment of essential documents including the W-2 form and IRS Form 2106 if claiming non-reimbursed business expenses. The process underscores the necessity for both employee and employer certifications, ensuring that all information is accurate and truthful. The inclusion of tax rates for residents and non-residents, along with specific instructions for calculating taxable compensation and allowable expenses, further delineates the criteria for what constitutes a valid claim. Ultimately, this petition form embodies a structured pathway for commission-based employees to seek refunds on potentially over-withheld wage taxes, stipulating meticulous documentation and adherence to established tax regulations as facilitated by the Philadelphia Department of Revenue.

| Question | Answer |

|---|---|

| Form Name | Wage Tax Refund Petititon Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 2017 philadelphia refund, philadelphia wage refund petition 2020, wage refund petition, 2018 fillable philadelphia wage tax refund petiton |

TAX YEAR |

|

WAGE TAX REFUND PETITION |

|

|

|

|

|

|

|

OFFICE USE ONLY |

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

2017 |

|

COMMISSION EMPLOYEES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

(Not to be used by Salaried Employees) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Read the instructions for both the Employer as well as the Employee on the reverse side of this form prior to completing this |

|

|

|||||||||||||||||||||||||

petition. Print or type all information. The completed petition must include: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Signature of Employee and Employer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

IRS Form 2106 if claiming expenses on Line 2E. If Form 2106 has an entry on Line 4, submit a breakdown of those expenses. |

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

EMPLOYEE'S NAME |

|

|

SOCIAL SECURITY NUMBER |

|

|

DAYTIME TELEPHONE NUMBER |

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

HOME ADDRESS |

|

|

|

|

|

|

|

|

OCCUPATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

|

STATE |

|

ZIP CODE |

|

|

IF PARTIAL YEAR, PROVIDE DATES: |

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

From |

|

|

|

|

To |

|

|

|||||||||

EMPLOYER |

|

|

|

|

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER (EIN) |

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

PLACE OF EMPLOYMENT |

|

|

|

|

|

|

|

COLUMN A |

|

|

|

|

|

COLUMN B |

|

|

|||||||||||

|

|

|

|

|

|

January 1, 2017 to June 30, 2017 |

|

July 1, 2017 to December 31, 2017 |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. Gross Compensation per |

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

A. |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B. Adjusted Gross Compensation (Subtract Line 1A from Line 1) |

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2. Computation of taxable compensation and/or allowable expenses |

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||

A. Total Sales |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

B. Sales outside of Philadelphia. Supply breakdown of sales activity performed (i.e. solicited) |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||||

outside of Philadelphia including client’s name, address, and sales amounts attributable to each client. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

C. Percentage of sales outside of Philadelphia |

|

|

|

|

|

|

|

. |

|

|

|

|

% |

|

|

|

|

. |

|

|

|

|

|

% |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Divide Line 2B by Line 2A and round the resulting percentage to 4 decimal places. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D. Commissions earned outside of Philadelphia. Multiply Line 1B by 2C. |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

E. (i) Total |

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||

|

Schedule A, Miscellaneous Deductions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(ii) Multiply amount on Line E (i) by the percentage on Line 2C |

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

(iii) Deductible |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

F. |

Add Line 2D and Line 2E (iii) |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

3. Net Taxable compensation (Line 1B minus Line 2F) |

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4. TAX |

Resident of Philadelphia multiply Line 3, Column A by .039004 and Column B by .038907. |

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

.00 |

||||||

DUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

5. TOTAL TAX DUE (Add Line 4, Column A and Line 4, Column B.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

6. Wage tax withheld per |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7. REFUND REQUESTED (Line 6 minus Line 5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMPLOYER CERTIFICATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

I certify that the facts shown above supporting employee's claims are correct based on available payroll records. Individuals serving as authorized official signatories should be familiar with employee's time and attendance, as well as applicable Wage Tax Regulations. Income Tax Regulations Section 401 through 404 requires that the employer withhold and allocate wages for tax purposes. General Regulation Section 306 (2) provides that the employer, for and on behalf of the employee, requests the refund.

AUTHORIZED OFFICIAL SIGNATURE (Signature must be clear and legible.) |

PRINTED NAME |

DAYTIME TELEPHONE NUMBER |

|

|

|

EMPLOYEE CERTIFICATION

I HEREBY CERTIFY that the statements contained herein and in any supporting schedule or exhibit are true and correct to the best of my knowledge and belief. I understand that if I knowingly make any false statements herein, I am subject to such penalties as may be prescribed by City Ordinance.

EMPLOYEE'S SIGNATURE (Signature must be clear and legible.) |

DATE |

|

|

INSTRUCTIONS FOR FILING WAGE TAX REFUND PETITION

(Commission Employees Only)

You must attach the applicable

2017 TAX RATES

Resident Rates: January 1, 2017 to June 30, 2017 = 3.9004% (.039004)

July 1, 2017 to December 31, 2017 = 3.8907% (.038907)

July 1, 2017 to December 31, 2017 = 3.4654% (.034654)

Statute of Limitations - any claim for refund must be filed within three (3) years from the date the tax was paid or due, whichever date is later.

Only

The taxability of sales by commission employees is based on the place of solicitation. You may exclude sales outside of Philadelphia if you are out of Philadelphia when the sale is solicited and the order taken. If you are selling by phone from Philadelphia, these sales are taxable no matter where the customer is located.

Both the employer and employee must sign the petition for refund. A petition for refund of "erroneously withheld wage tax from an employee must be made by the employer for and on behalf of the employee" (General Regulations Section 306 (2)). The authorizing official signing this form should do so only if they know of the employee's whereabouts as they relate to this petition, as well as an understanding of how this information applies to Sections 401, 402, 403, 404, 405 and 407 of the Philadelphia Income Tax Regulations. These regulations are available at www.phila.gov/revenue.

Partial Year: In the context of this form, a partial year is one in which your liability or status for Wage Tax changes. It could be the result of becoming a resident, starting a new job, terminating a job, etc. In any of these situations you need to indicate the period for which you

were liable for Wage Tax with a particular employer.

Line 1: Enter your Gross Compensation (generally the highest compensation figure on the

Line 1A: The only income excludable from gross compensation would be income received as the result of exercising an employee stock option. Stock option must reflect on

Line 2: This line should reflect Total Sales for the year. If your compensation is based on more than one commission or a combination of salary, commissions, fee, etc., prepare a worksheet calculating the amount due and attach it to the petition, marking this line "see attached".

Line 2B: This line should reflect Sales Outside of Philadelphia as noted above. Supply breakdown of sales activity performed (i.e. solicited) outside of Philadelphia including client’s name, address, and sales amounts attributable to each client.

Line 2E - Expenses: An entry on Line 2E must be supported by Federal Form #2106. If unreimbursed employee expenses are claimed on Federal Schedule A, you must also include Schedule A. Photocopies are acceptable. Expenses are deductible if the total expenses are reduced by any amounts reimbursed by your employer and they are ordinary, necessary and reasonable. Examples of expenses which are not deductible are: transportation to and from work, educational expenses, dues, subscriptions, and pension plan payments. Note: If your Federal #2106 has an entry on Line 4, you must submit a breakdown of those expenses.

Mail completed petition to:

CITY OF PHILADELPHIA DEPARTMENT OF REVENUE

P.O. BOX 53360

PHILADELPHIA, PA 19105

For further information you may reach the Revenue Department Refund Unit at:

Fax:

Send

8 www.phila.gov/revenue