- Foreword

- Marriage Patterns are Changing Dramatically

- The Overall Impact of COVID-19 Pandemic

- Covid Impact on Money And Resources as Reason for Divorce

- Coronavirus disease (COVID-19): Small public gatherings

- The Good and the Bad News About Marriage in COVID Times

- Childcare Issues in the COVID-19 Context

- Estate Planning During COVID-19: Things You Must Know

- What Documents Comprise Estate Planning?

- To Sum It All Up

Foreword

New researches concerning the influence of the Covid pandemic—both short and long-term—are appearing throughout the globe, one after another, in a continuous fashion. Small wonder: first, the prolonged state of uncertainty and, let’s be honest, fear and at times, panic, could not but have had the most profound effect on the entire scope of social and individual matters of nearly every nation on the planet; second of all, the institution of marriage and the side issues involved have been literally transformed, if not ultimately reimagined. And the major change, of course, has not come unnoticed both by the average and by people of science, too.

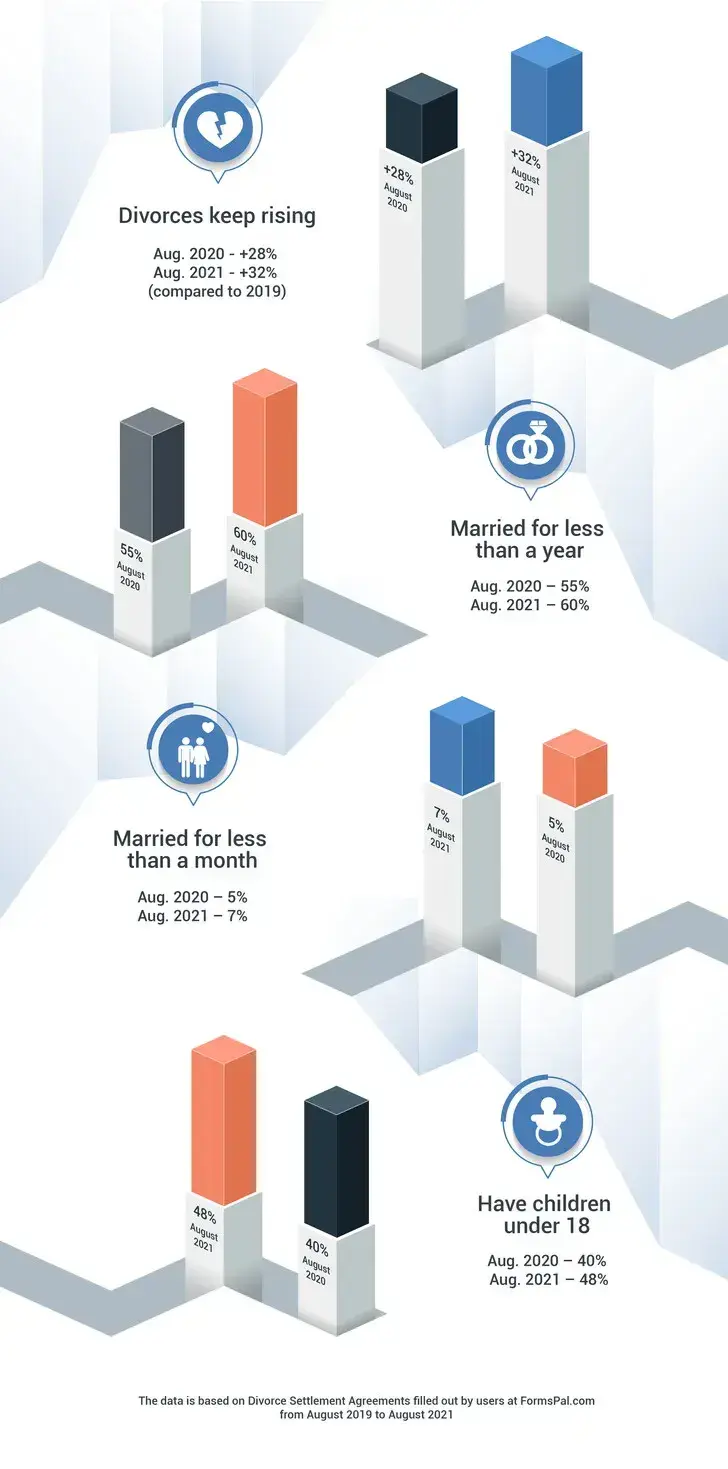

Through analysis and building up of the statistical data, we have acquired evidence of the ongoing peaking divorce rates in the USA in the times of the covid pandemic. To gain insights, we analyzed the input data from divorce settlement agreement templates filled out by users on our website. The document, known by different names depending on the place of residence of the person divorcing, is aimed to contain the conditions concerning several aspects of post-marital lives of ex-spouses, including child support and alimony.

To complete the form, one needs to take several steps, including court and marriage info, details concerning both parties divorcing, their children, conditions of assets division, alimony, etc. The people’s completion of certain steps of the form on our website granted us the needed info for statistical analysis.

During the pandemic, we have identified a considerable increase in numbers of people who complete the divorce settlement form using the builder on our website, amounting to nigh 21% as opposed to this time in 2020. The trend that started over a year ago is still on the rise and exacerbating, while the pandemic has not yet subsided.

With this data—collected completely legally and anonymously and compiled during more than a year-long timespan—our team decided to take a more detailed look at the problem.

Here is what we have managed to identify:

- The rise in life insurance and payments included in divorce documents.

About 53% of the divorcing parties paying spousal support are required to have an insurance policy amounting to $421,375 on average, which is a slight increase compared to 2020 with its 48% and an average amount of $380,934.

- The just-married have been most affected by a considerable margin.

It took many couples less time to start the divorce process after the beginning of the married life: particularly, less than a year to make the crucial decision, compared to the same period of 2020. Overall, over 60% of the divorced have been married for no more than 1 year, compared to the 55% in 2020.

- The southern-state marriages have been hardest hit.

The rate of divorce settlement agreement completions in the south of the country has been on the rise, especially in Mississippi, Oklahoma, and Arkansas, which is nearly two times as high as in other regions of the US.

- Families with children have come apart more often since the pandemic outbreak.

While the couples with children younger than the age of majority tend to divorce less, the pandemic has entailed a nearly 5% increase in divorce agreement initiated by such couples in 2021 compared to 2020.

- 7% of newly-married couples have proven to be unable to withstand even a month of marriage.

The newlyweds may have fallen in a so-called Phase of Disaster as a result of the stress and anxiety the pandemic has entailed. In such situations, people tend to react negatively, which is among the causes of interpersonal conflicts and family break-ups.

Further in our article, we will:

- Walk you into the relevant researches’ discoveries in the field of the changing marriage, family life, and divorce patterns in the USA;

- Flip through the latest data on childcare issues amid the pandemic;

- Look at the baby boom and domestic abuse cases;

- Discuss several documents one needs to keep in mind while divorcing, and, above all,

- Try to make out the reasons for the dramatic change and give some projections for the future.

But first off, let us consider the changing marriage patterns and the crucial effects concerned.

Marriage Patterns are Changing Dramatically

What seems to unite the revealed statistical facts is that, after being interpreted, they agree with the notion that the influence of the pandemic will subside only in the years to come, unless it will stay with us for a while longer. The divorce rates, having been on the rise for several decades anywhere globally, are still crawling up to register at somewhat unprecedented tops. And let us not neglect that the afore-mentioned event is always a challenge: unpleasant in its complexity and aggravating for a divorcing couple as it surely is, the children do suffer, too. Let alone the cases when the path to the inevitable divorce is paved with domestic abuse, violence, and indecisiveness of either party to put a stop sign and look around for a while, to see what is going on with clear and adequate vision. But how can it be possible when perpetual economic and behavioral convulsions have already vaporized the last drop of patience?

Besides the exclusively matrimonial and socio-economical issues a divorce process usually entails, it also faces the divorcing parties with a ton of paperwork: such spheres of life—unheard by many before the divorce court session— as estate planning, last will, and living will forms completion, designating a proxy for the Medical Power of Attorney, and more, reveal themselves in their entirety. Indeed, it can take up many consecutive hours before one can figure out what documents to sign and what date they are due, which adds even more fuel to the flames of a divorce procedure. Can it be any different, though?

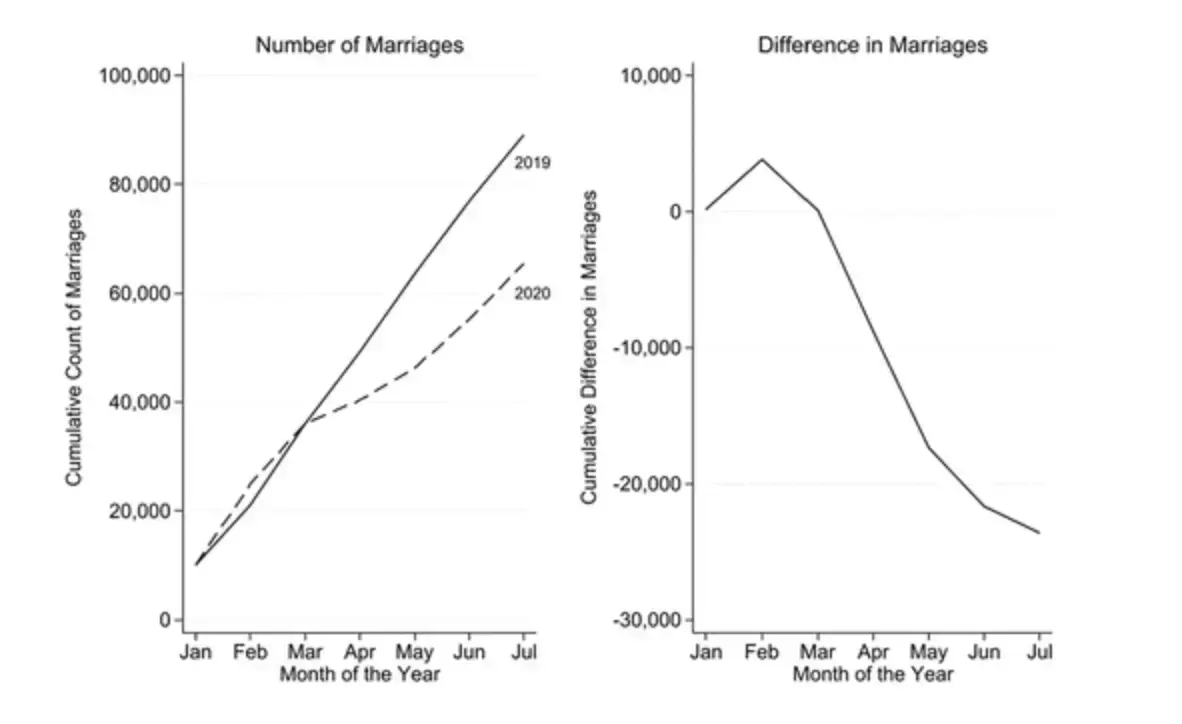

While the full amount of effects caused to the marriage still requires careful compilation, thorough calculation, and interpretation, as for now, we can apply certain approaches and find out at least the basics of what is happening to marriage as union formation. For one, the decline in the number of marriage certificates and applications for marriage can serve as proof that the figures have dragged down, compared to 2019 and early 2020. Year-to-date marriages are down, as well as the numbers of people wishing to get married soon. Relying on such administrative data fills the gap existing in the public understanding of the problem’s real scale.

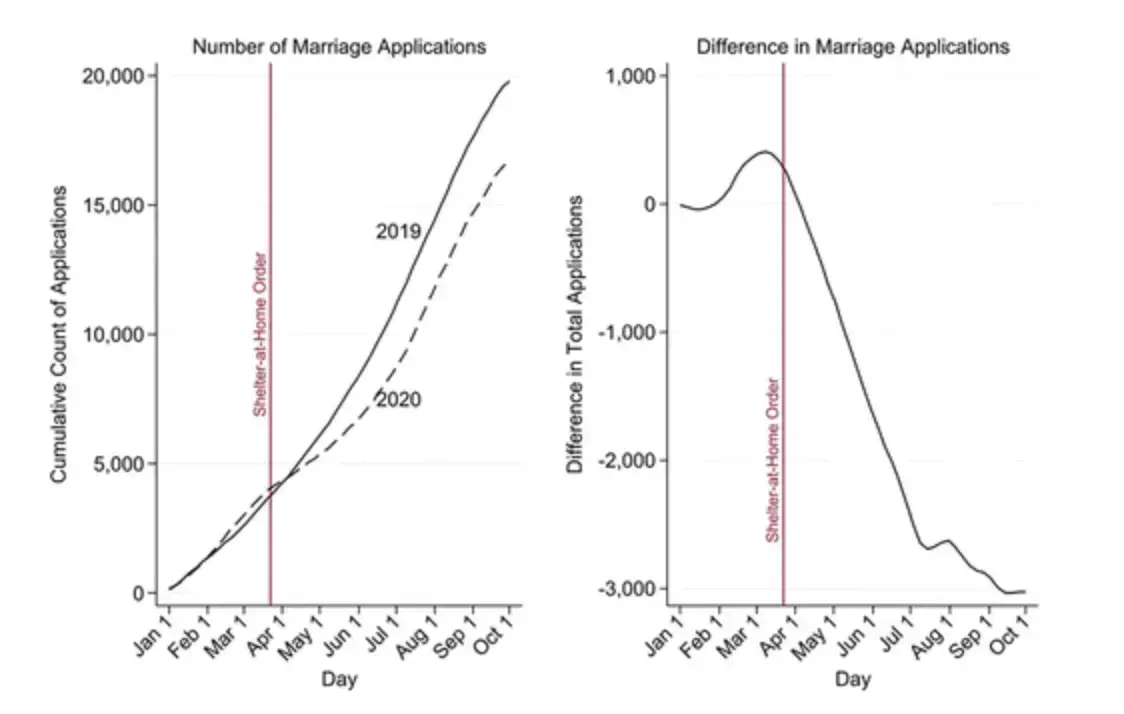

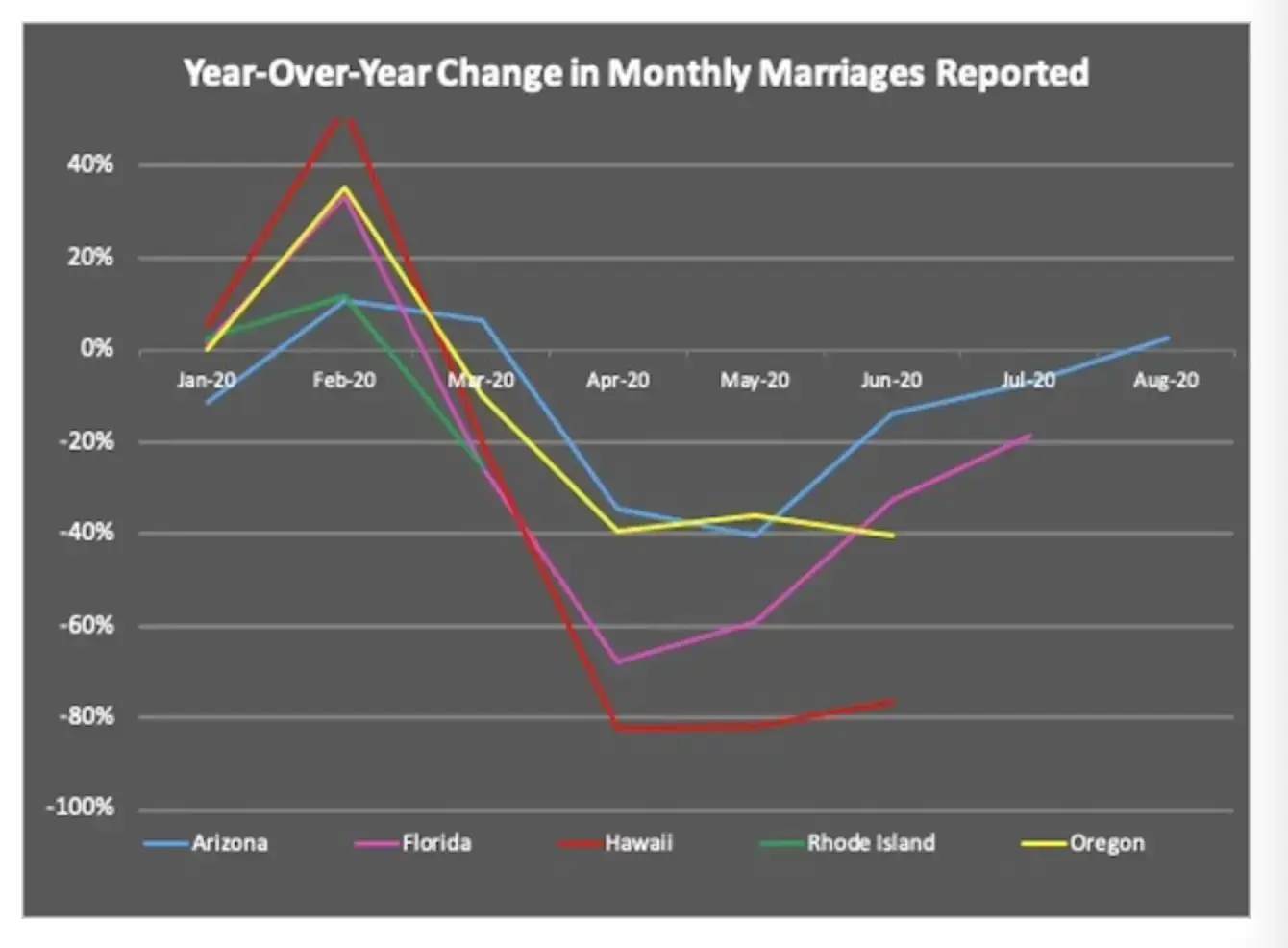

While the procedure in view of documentation involved is pretty much uniform across the country, the figures obtained by the approach are universal for the USA. Let us consider the graphs below demonstrating the downward trend for the year-to-date cumulative number of marriages in Florida and the number of marriage applications in the Seattle metropolitan statistical area as of summer 2020. Now, nearly a year after the start of lockdowns, the situation looks as dramatic.

Starting from March 2020, fewer and fewer marriage certificates have been issued in the city, decreasing to about 30 percent, compared with the previous year.

While the 15-percent decline in applications for marriage in Seattle seems to draw a more pleasant picture in comparison with that in Florida, researchers studying the problem claim that in such regions, where the decrease in marriages fluctuated between 15—30 percent, everything will get back to the norm in the nearest future.

In 2021, the situation has not normalized yet, with the prolonged lockdowns and other restrictions, which, researchers claim, all together have become formative in people’s growing desire to get divorced in the USA, at least in the short term. While researchers have tried to tie the issue with the like effects on marriage patterns posed by natural disasters, the impact of the pandemic is yet to be comprehended.

The Overall Impact of COVID-19 Pandemic

Let us delve into the information concerning all adverse aspects of the COVID-19 pandemic influence. A married couple is exposed to the effect of the processes going on externally: a micro version of society, peace in a family, therefore, depends much on the factors lying beyond the sensual and romantic.

Stress and anxiety—and in some severe cases, depressive state and suicidal manias— have become an inevitable part of almost any family environment during the pandemic. The problems facing people throughout the globe have only been accumulating due to the long-lasting lockdowns and self-isolation measures, researchers have revealed .

The impact on the population seems to have extended to all realms of human life: both social and psychological effects of the pandemic should be studied thoroughly in order to discover or, perhaps, invent specific approaches to combat the adverse influence in the long run.

Below, we will take a shot at evaluating psychological and behavioral effects on the people in the USA and figure out prospective steps our nation should aim at in the nearest future, tightly entwined with social security and mental health improvements.

But let us first unveil political and social factors that demand our close studying and acknowledgment. Take a look at the table:

| Political Impacts | In the very beginning of 2020, while some officials responsible for handling and curbing the pandemic effects in China were losing their posts in the midst of the growing public uneasiness, other nations around the globe extended their helping hands—both politically and materially—in the act of solidarity with the Chinese people fighting with the disease. Former US president Mr. Trump has been generally accused of his inability to keep the situation under control. He seemed to diminish the real scale of the danger posed over the nation, falsely claiming, stating, and relaying all the responsibility onto China. With such developments in the backdrop, small wonder that the election was dominated by his opponent Joe Biden, whose approach towards the pandemic is diametrically opposite. |

| Sovereignty | Referred to as a massive financial crisis in the first place by members of the advisory board at the World Bank, the pandemic is projected to bring about instability and dysfunction in geopolitical and economic spheres worldwide. |

| Civil Rights and democracy | As some developing nations such as Oman and Jordan have restricted press print and distribution, in more developed countries, some top officials are getting unlimited and unregulated powers. Case in point— Hungary. |

| World peace | Military conflicts around the globe seem to have gained acuteness in the pandemic setting. While some of the hard-hit nations agreed on ceasefire measures, others only tightened the grip on their rifles. The situation appears to be unstable in some regions of the planet, causing international peacemakers a ton of painstaking and challenging decision-making. However, a specimen of humanitarian pause has been observed as well. |

| Educational impact | The pandemic has shattered the educational systems of the world: remote learning necessity has extended a challenge to the policymakers of most, even well-developed regions. Schools and universities are being closed; some of them never reopen again. One hundred sixty-five countries worldwide have faced massive closures of educational institutions, affecting around 2 billion students overall, UNESCO claims. |

| Coronavirus and inequality | Families with low incomes have been reported to be more likely to face severe effects of the virus: from contracting it to death from the disease. New York, the hardest-hit city in the USA, has been a battlefield for some low-income districts, where people died at a higher rate than anywhere. The reasons: reduced access to social insurance and medical care in conditions of massive unemployment and poverty. |

| Religious impact | Religion in the USA has also been affected by the pandemic. We are praying together for the soon end. As a result, a National Day of Prayer for “God’s healing hand to be placed on the people of our Nation.” has been established by Mr. Trump in March 2020. |

| Psychological impact |

Last year, WHO created a report about mental issues facing people due to the pandemic, aiming to instruct societies on possible actions to withstand the psychological pressure. Suicide There is an upward tendency in suicides heated up by lockdown and social-distancing measures and is most vocal in unemployed individuals dealing with fears and anxiety. Risk perception The spotlight of the public audience has leaped from the environmental problems, poverty proliferation, or any other, even severe, issues onto the COVID pandemic. While being dangerously overlooked, these have not gone anywhere. Coronaphobia Another side effect of the covid frenzy is coronaphobia. All aspects of life seem to be affected; hence, a possibility of getting phobia. Socialization issues It’s gotten hard for many to keep socializing in the context of the frightening death tolls all over the globe. The return to the norm, too, has been uneasy and with a pinch of madness. The behavioral patterns overcome individuals and bring new, not always pleasant, discoveries of both spouses in each other’s tempers. |

| Personal gatherings | Getting together has been so minimized and involves either contagious or law-related side effects. As the distance grows safer and less doubtful, the more regular pre-pandemic patterns might return or might not. |

| Domestic violence | Researches and subjects of the current hot discussions around the growing numbers of domestic violence cases indiscriminately demonstrate: it has grown worse and less controllable behind the closed doors of the quarantining households. |

| Elderly care | The more advanced in life part of our society, the older people have been reported widely to be the primary target of the worst covid’s symptoms and post-syndromes. The death rate in the pocket of society is still peaking. Despite this, the elderly individuals need to have their care doubled, which poses a challenge over medical facilities and their families—a hard-to-get goal during the pandemic. |

| People with disabilities | Also vulnerable to the impact of the pandemic are disabled people. It can be really tough to keep track of the hygienic measures’ heeding in case of a mental disability of the person. In the isolation times, these members of the population can experience the worsened states and conditions in addition to those they had before the pandemic broke out. |

Covid Impact on Money And Resources as Reason for Divorce

The horrible effects of the pandemic have been portrayed in recent research by the Health Foundation. Among them, money issues play a crucial part as a pillar of the stability and sustainability of a marriage. The future of people’s well-being seems to be largely dependent on the subject as well. The rise in talks on inequality is evidence of the things getting widely spread all around the planet. While it had not been all perfect in terms of people’s incomes in the pre-pandemic times, now, it has exploded. The numbers of people possessing no home or basics of survival are becoming oversized, as is seen from the studies and by the look around.

People living in the deepest poverty have been hit particularly hard. The hardest suffered the poorest, nearly a half of the nation, with fewer chances to treat the covid itself or maintain the normal health condition after the treatment is over and the patient is released home. Among the poorest group of people, disabled Americans are at the peak of risk. All these factors lead to the disintegration and further distancing of the layers of society from each other.

The government’s response

Families with tiny incomes have been taken care of, with so many governmental campaigns aimed at supporting the most vulnerable bits of our communities. However, as the major part of essential and low-paid jobs has been put on the migrants’ shoulders, the uneasiness around hate crimes is being heated up perpetually.

Coronavirus disease (COVID-19): Small public gatherings

Every event, big or small, should not slip from under the observant eye of authorities. And this, for a reason: safety first. WHO has developed a guideline on organizing and holding public events, highlighting the importance of the preventive measures and their simplicity compared to the steps to treat the disease.

Below, there is a top 10 list of recommendations by WHO:

- Be aware of the regulations currently implemented in your area.

- If you don’t feel well, stay home.

- Stay away from the others by 1 meter at minimum. Use handkerchiefs and tissues.

- Mind your hygiene.

- Inform all the guests of the measures.

- Get it on the outside.

- Avoid crowds.

- Buy and distribute sanitizers and soap.

- Watch your kids closely.

- Be up to date with the vaccination news.

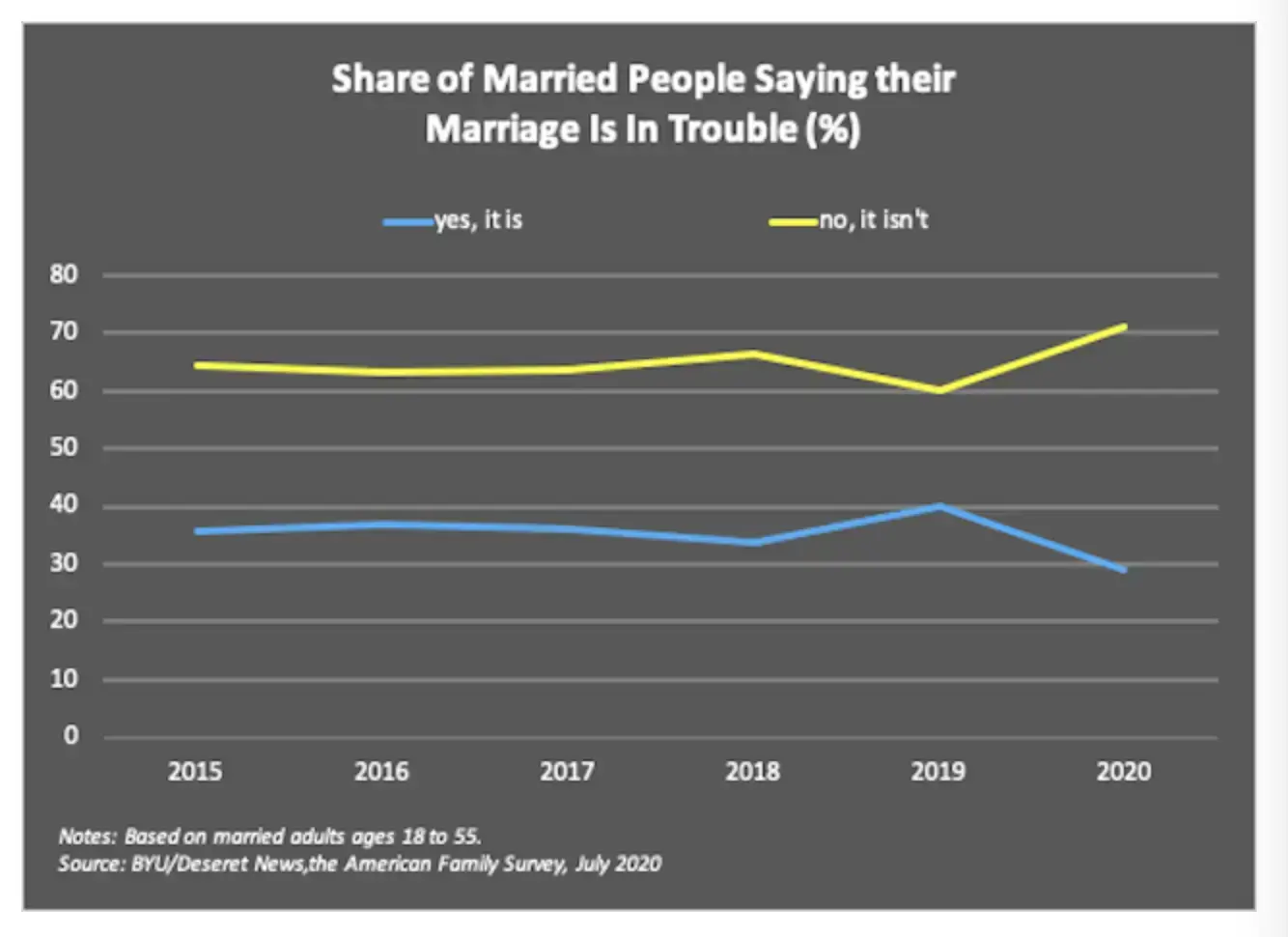

The Good and the Bad News About Marriage in COVID Times

Some researchers , however, see the bright side of the pandemic. While it may sound odd against the terrible things happening on Earth due to the pandemic, there might be some positive aspects of the covid on families. But first, let us put forward the bad ones.

The Bad News

You need no research to state that people are being exhausted and stress-out. Out of work, out of money, out of the hard-won comfort, people report the worsening tendency in terms of stress.

Marriage Is Down

Because the lockdown measures have affected the marriage patterns throughout the globe, marriages have dropped down by 6 to 20 percent in the USA. The marriage rate is at the historical bottom, surveys demonstrate.

The possibility of a more dramatic decline seems to be more palpable. This is reflected in the changes in marriage certificates filed every month in the USA.

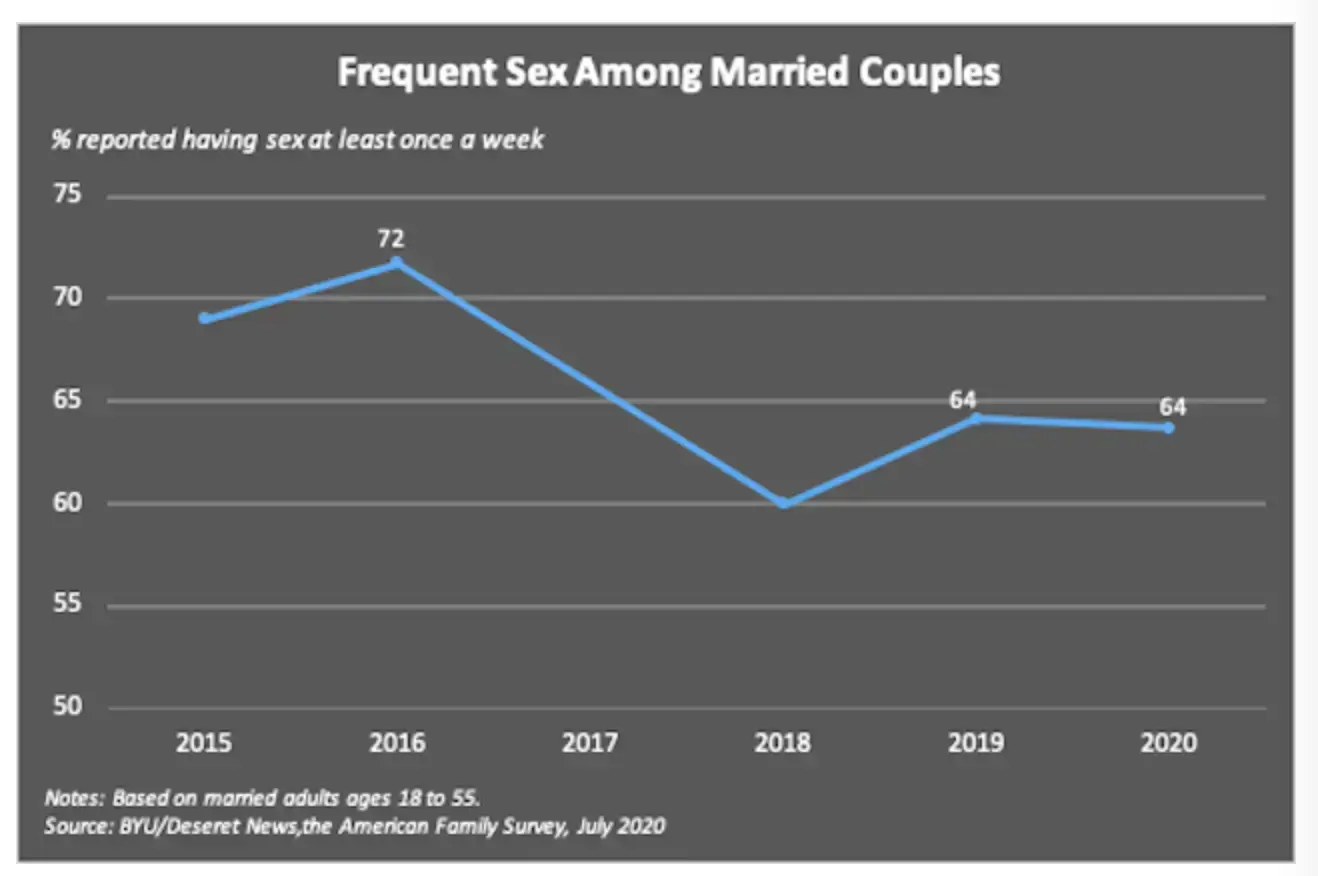

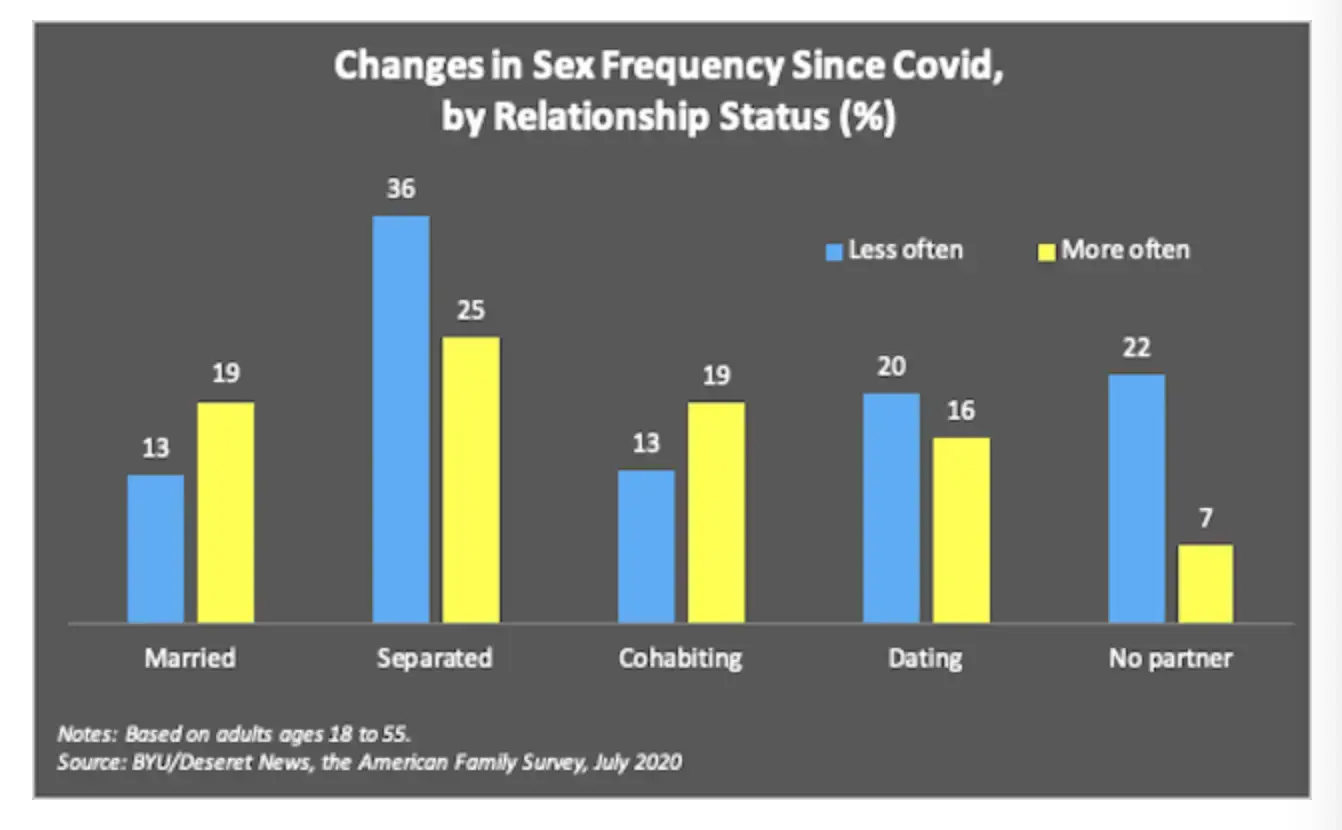

The decline is evident for most states; most of them are yet to come back to the norm. Marriages keep delaying and finalizing against the backdrop of the problems in relationships, economy, and romance in a couple’s life. Below is a figure showing the reduced cases of sex in married couples.

What seems to look like a positive trait is increased sexual contact between the married of 18—58 years old.

The Good News

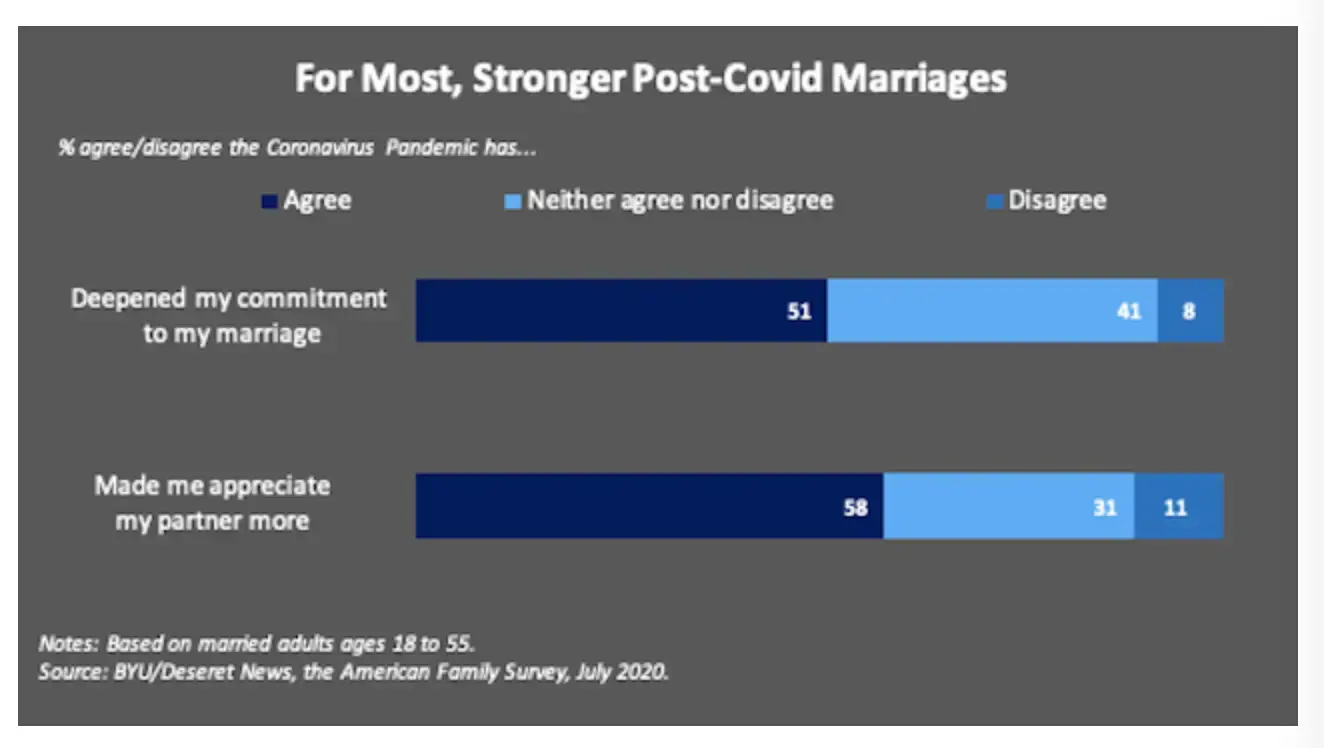

As to the bright side of the COVID-19 impact on families, the increase in mutual respect, adoration, and commitment of a deeper kind has been reported by many Americans. Hard times seemed to have affirmed and fortified some families in the USA.

Less divorce?

Some stats and lessons of past experience reveal that the marriage rate should go up in the nearest future and take a more stable direction for the years to come.

The reality is not as simple as it might seem while looking at some stats and graphs. The complexity of issues caused by the pandemic regarding family life and marriage patterns has incorporated both negative and positive trends. Poverty, unemployment, instability, stress do exist but surely will not last forever. Analysts say that the initial projections on the pandemic’s impact were far worse than the actual drawbacks. While the times are hard for many, some couples find the nerve not to let go of each other’s hand, supporting and understanding in mind.

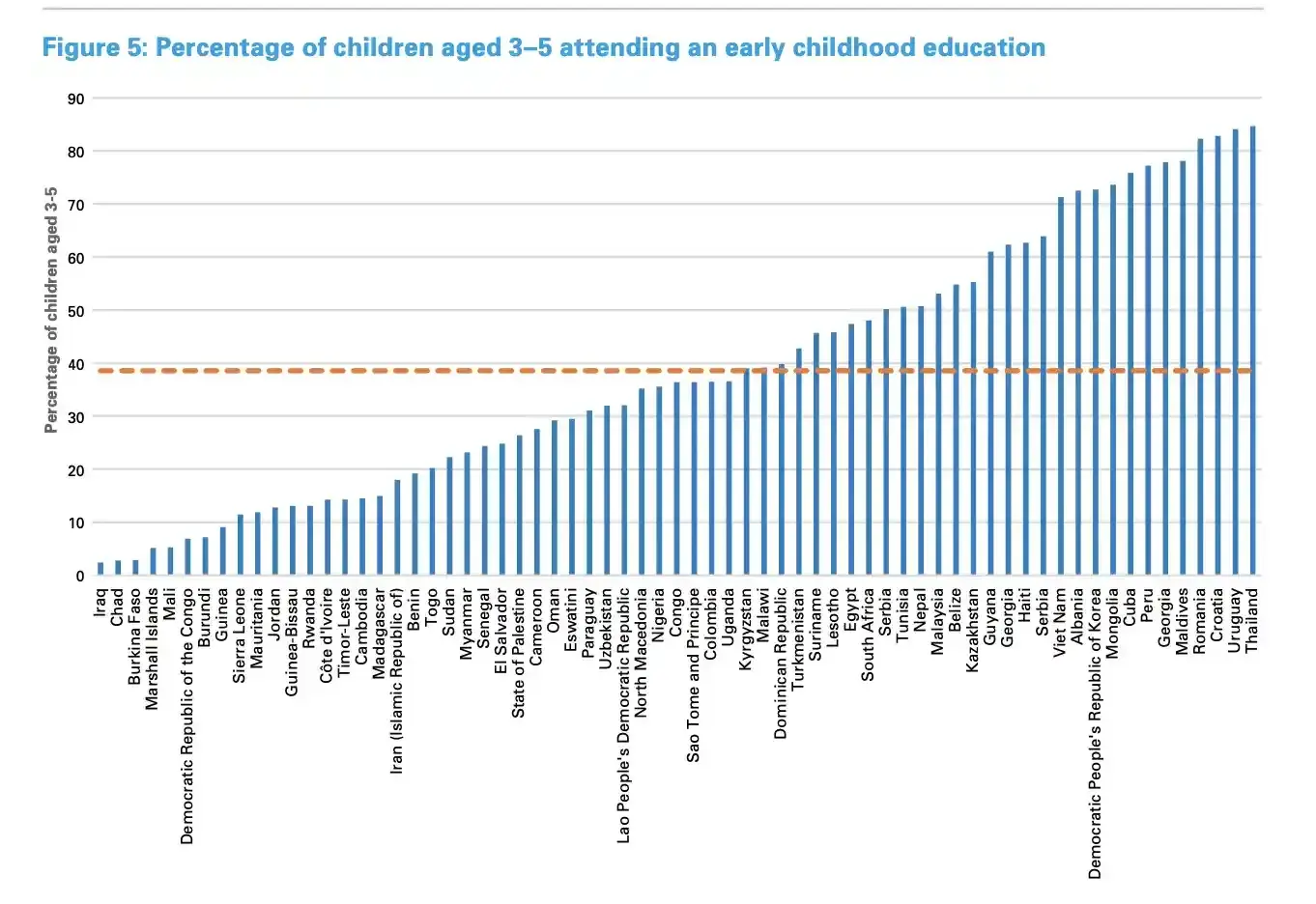

Childcare Issues in the COVID-19 Context

The impact of the pandemic has been seen widely in the younger parts of society: while most parents face severe challenges in relationships, money, and the economy overall, the childcare crisis is ongoing. No supervision or proper medical care, let alone overwhelmed mothers—all that adds to the already not-so-pretty picture. The way out is robust governmental support and material payments, analysts say.

Globally, the quality and accessibility of child care have been decreasing due to the pandemic. Mothers worldwide, who traditionally tend to put up with all the domestic chores, as well as take up the biggest part of child-rising duties, are at risk of stressing out, depression, and more severe health problems.

Emotionally, children cannot but react, though subconsciously, to the stress posed by the pandemic, which makes them highly vulnerable in the context of the COVID-19 outbreak.

Grandparents and siblings can be involved in the child care process, which is often the case. However, due to the ongoing restrictions and lockdown measures, it has become impossible for some families to get together to make it happen.

Childcare policies implemented worldwide are also changing the quality of childcare, providing more chances to the hardest-hit to sustain the after-effect of the pandemic, including the long-term ones.

All school educational facilities have been facing significant changes as well. While some schools had to be closed, others remained afloat, with hope for help from authorities.

The responses of the governments to the child care issues have been different so far; however, there are specific recommendations designed by WHO that governments need to keep in mind.

Estate Planning During COVID-19: Things You Must Know

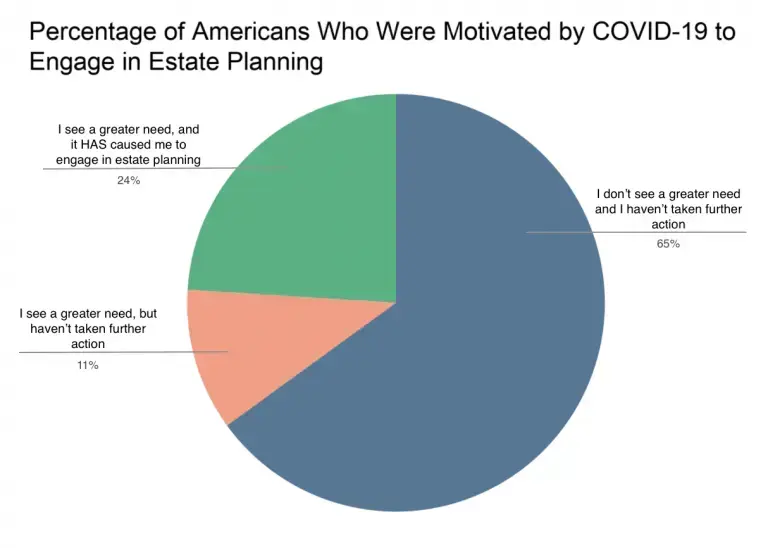

The global pandemic has brought many changes upon us, and we haven’t realized their impact entirely yet. At this point, we can say that a combination of an unprecedented economic downturn that occurred during the spring months of 2020 and the subsequent presidential election (amid the impeachment and the fuss surrounding it) combined have entirely changed the game in the residential estate and investment market. Below, we will tell you why it is high time you changed your estate plan.

The key to understanding global processes lies in the fact that people create all the hype and feedback the market reacts to. Most of you probably remember the spring of 2020 very vividly: the increasing health concerns, global lockdown, restrictions to leave your homes without reason, unclear death rates, and the overall growing anxiety. All of the uncertainty has produced global hysteria and forced people to save and accumulate rather than acquire anything new. Such a behavior pattern is logical, but it has had some apparent consequences regarding the estate market.

What Exactly Is Happening and Why?

The anxiety has been growing ever since March 2020. It resulted in real estate sellers and landlords being afraid to allow strangers into their property due to either lack of trust or pandemic restrictions. The effect kind of relented in the summer: the housing sales seemingly went back up, and people thought everything was back to normal. The thing is, back then, no one really knew how long it was going to last, so the construction companies, governments, and realtors had already taken measures.

The banks with federal funding have started offering concessional loans and mortgages to support the construction industry and boost the demand for housing. Truth be told, this has been happening in many countries worldwide, and it helped for a while. But in the US, the reminiscences of the 2007 housing bubble still linger in people’s minds.

Just like in any crisis, some acquire and get richer, and some lose their last. This time, people have decided to reconsider their consumption and housing needs. As you can see in the trend below, a significant share of people in the US was concerned about the post-pandemic consequences and, thus, have taken action and changed their estate plans:

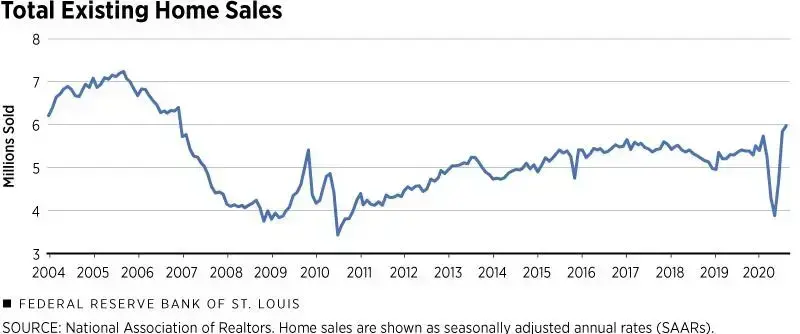

Was it due to cold calculation and consideration or basic human fear of the unknown—it is still hard to say unequivocally. People were hesitating to sell their properties in the wake of the global COVID-19 pandemic. Thus, in April-May of 2020, the overall housing sales have dropped to their lowest since 2007. Then, just one year later, the number of delisted dwelling units increased by approximately 25%.

A think tank headquartered in Saint Louis and called the Federal Reserve Bank had gathered statistics of all houses sold and median sale prices to see what is currently happening in the housing market. Here is what they have discovered.

New listings have dropped by over 40% by April compared to the same period of 2019. It all had created a severe decrease in inventory, and the housing supply has officially hit a new low. Refer to the table below to see how the housing demand and supply statistics changed during the first wave of the pandemic restrictions.

The same trends are fair as to the property-buying activity in the US. On average, property showings per listing decreased drastically (for more than 40%) in April 2020 compared to the same period of 2019. And it is not just the sales themselves; the online search activity was also down by a lot back in April.

But this is not the most surprising thing yet. You know how—typically—a significant decline in demand contributes to a similarly significant drop in prices for new housing. Well, that did not happen. On the contrary, the market faced a rise already in May 2020. The COVID-19 has caused turmoil that, in turn, has created a unique economic environment and circumstances: historically low mortgage rate, low demand, and relatively low supply. Take a closer look at the table below to see it for yourself.

Sure, the results differ significantly by area and depend on the local conditions and investment climate. Thus, while metro areas have faced an average decrease of approximately 34% (according to the National Association of Realtors research), some urban areas have suffered a more severe decline. For instance, there was a 58% drop in sales in New York City and a 74% drop (the biggest one so far) in Detroit.

Relevant changes to consider

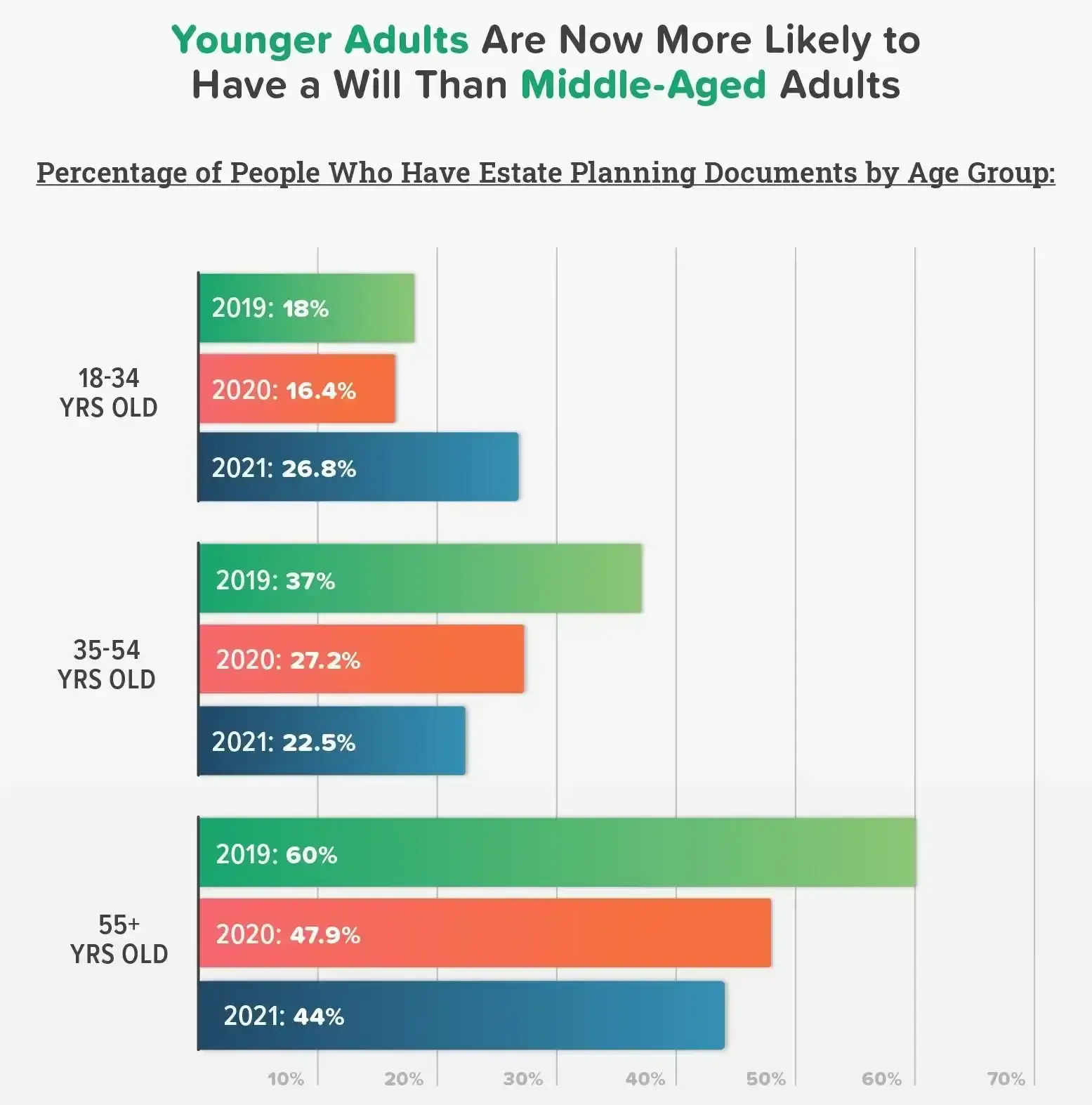

Slowly but surely, we have gotten to a point where we can describe what this all means for estate planning and each of us in particular. To start with, 2020 is the first year ever when the number of young adults (18-34 year-olds) has surpassed the number of 35-54 year-olds with a will.

Gentreo, one of the biggest US companies specializing in estate planning, admits that it has seen a 143% increase in online will requests within the first week of global lockdown (the end of March-beginning of April). That is a huge number. Another big fish in the legal assistance market, Trust & Will, has outlined a 63% uptick in online users over the last year. It is worth mentioning that in 2019, the Uniform Law Commission passed the Electronic Wills Act, which allows licensed and certified agencies to issue electronic wills that are identical to their paper analogs in terms of legal force.

All subjective factors aside, young people started to treat their health and inheritance matters more seriously, and getting a will is the best way to prove that. You can grant your properties, savings, business shares, and other assets to people you care about free of charge. Thus, if anything happens to you suddenly, your close and loved ones will not be left without any means or ability to make a living.

Okay, so suppose you have finally decided to grant your real estate and other assets to your closest relatives and heirs. What do you do next?

You should know that any gift (whether in real estate or cash) is considered personal income and is subject to taxation. As of 2020, an individual can transfer $11,58 million to heirs-in-law without the necessity to pay taxes. If it is a married couple, they can transfer double that amount which equals $23,16 million. Such transactions and relations are regulated by the Federal Estate and Gift tax legislation. But you should also consider that due to absent Congressional action, the amount is most likely to revert to circa $5-6 million adjusted to inflation (effective January 1, 2026).

Thus, business people and people with significant accumulations desiring to prepare and notarize a final will should be very cautious. By all means, it is high time you reconsidered your estate plan, and here are the five primary factors you should take into account:

- Individual financial plan, income rate (with changes due to COVID-19), and objectives;

- Housing or business market value preservation;

- Historically low-interest rates (combined with low demand and relatively low supply);

- Group dynamics of a subject household o family;

- Tax legislation changes and personal income tax matters.

Now, let us briefly focus on each of these factors to comprehend their meaning concerning a household.

Individual financial plan

Technically, the name of this parameter says it all, but let us take a closer look at what elements it includes.

First off, the plan should include the income rates (both credit card and cash inflows) and paramount expenses in the short and long run. There are at least two reasons to comprise such a plan:

- One — you will better understand your current financial situation and manage your finances way more efficiently.

- Two — you will know what income flows you need to keep for your personal needs and objectives.

There is no reason to give these assets to someone if you personally need them right now (even if you are not entirely optimistic about the possible future outcomes and scenarios).

The same applies to retirement plans and insurance. It is important to have a strategy so that the resulting and assets granting would be consistent for both the giver and the recipient.

Estate Market Value Preservation

It is no secret that some businesses lose their total value in post-crisis times. Thus, the low valuation tendencies allowing people to qualify for tax reduction and be eligible for estate and gift tax exemptions have side effects. There were speculations that the 2020 presidential elections would make certain corrections to the estate and gift taxation legislation (that is active up to 2026). However, these predictions have not come true yet. But if the reduction happens, individuals and business people who haven’t used their highest exemption will most definitely lose their benefit.

Lowest Interest Rates in History

As we have established above, the interest rates all over the globe have officially hit a new low and for obvious reasons. The truth is, such measures are generally very favorable for the economic and investment environment. Sure, the balance should be kept in everything, and we will probably see the housing bubble grow in the future, but this is where estate planning comes into action.

We keep repeating this, but you indeed should be very cautious when choosing your new estate strategy. For instance, you can transfer your assets to a trust fund in exchange for an annuity. The dividends you get as a result will depend directly on the current interest rate. Thus, the lower the interest rate stays, the more beneficial your strategy is.

At the end of the day, it does not matter what strategy you eventually choose. With the low interest rates accepted due to COVID-29 restrictions, the good news is that the effectiveness of the estate planning strategies has significantly increased.

Household Dynamics

You can transfer your property within the household effortlessly. In the past years, this measure was prevalent amongst business people who granted their business partially or entirely to their children with tax exemption. Over time, the strategy has gained recognition way outside the business sphere. The main issue is to do it so that the renewed ownership structure does not lead to significant losses in fair market value.

When transferring tangible property or other assets, one should always keep in mind that it alleviates the owners’ tax burden during the economic downturn. If your family does not manage to transition properly, disputes will be inevitable in the future. And disputes, in turn, will immensely hurt the reputation of your business and eventually reduce its market value. To make the granting strategy consistent, you should comprise the estate ownership succession plan.

Tax Legislation Changes

We have briefly touched upon the estate and gift taxation policies, but there are other tax consequences one should mind when planning an individual estate strategy. The trick is, the assets (real estate and other savings) of a decedent get set up for income tax purposes by the IRS, but the assets granted by the decedent during the lifetime do not. However, mind that using just gift tax exemptions and nothing else for your estate preservation is not the most effective estate planning strategy.

Yet another major issue one should consider when comprising a comprehensive estate plan is the local tax legislation. You can employ an estate and assets granting strategy to gain a tax reduction in some circumstances. The statement is mainly fair for high-rate income tax states. We highly recommend you to check with the renewed list of high-income tax states on the IRS official website.

What Documents Comprise Estate Planning?

People often view estate planning as just preparing and having a will at hand. But there are other documents that are equally essential for the strategy. You, as the planner, should pay special attention to the following three legal documents:

- Medical Power of Attorney;

- Living Will;

- Last Will.

All of them combined will provide you the essential legal protection in case of an unexpected hardship or accident. Below, we will tell you more about each of the above-mentioned legal form types in particular.

Medical Power of Attorney

A Medical Power of Attorney is typically used when the owner is incapacitated or has a medical condition restraining them from making any serious life decisions.

Depending on the state, the document may be called Medical or Durable Power of Attorney or a Healthcare Proxy. Regardless of the name, the paper’s essence stays the same. With an adequately composed Medical POA, the applicant can assign a legal healthcare representative to make informed health-related decisions on their behalf.

The MPOA (or DPOA) will help you accomplish the following objectives:

- Appoint a legal healthcare representative (advocate) to make medical decisions on your behalf once you are unable to. It is worth mentioning that spouses or close relatives do not automatically become healthcare advocates for each other.

- Allow access to the patient’s medical treatment data to third parties. No person in the world can legally review your health-related info without your official consent (following the Health Insurance Portability and Accountability Act, 1996).

- Decide to stop any medical treatment. Usually, by an MPOA, the patient can decide whether they want life-sustaining therapy once they are in a coma or other irreversible vegetative state.

The list of decisions may also include pain management, recreational therapy, treatment methods, etc. As long as these measures directly influence the quality of life, you should only choose a person you can trust unconditionally to be your healthcare advocate, someone who possesses the necessary professional qualifications and personal qualities, including compassion.

If you already have an effective MPOA, we suggest you review it considering the currently emerging circumstances. The effect that COVID-19 has on the human system has not been fully explored yet. That is why it would be wise to reconsider your healthcare strategy now.

You may consult your physician to make an informed and qualified decision and make the necessary amends to your existing MPOA. Ensure to authorize any changes that you make to your MPOA. The authorities tend to view all handwritten changes with a fair share of skepticism and for a good reason.

Last but not least, keep the completed document at hand at all times, just in case. Take it with you when you go to the hospital and provide an additional copy for both your therapist and healthcare advocate.

Living Will

Next up is a Living Will form. You might know this document under a different name—an Advance Directive. It is a legal form determined to specify the particular medical treatment type for a person whose life is threatened. That is the major difference between the medical power of attorney and an advance directive.

The subject person may be unconscious (in a coma) or otherwise unable to communicate their life-sustaining and medical treatment wishes and desires verbally. But it is important to understand that doctors will not refer to a living will to get consultation on standard medical treatment and procedures. The will is only there to help them decide what to do when the patient is terminal or in a life-threatening situation.

The Living Will covers several issues related to the medical treatment of incapacitated or inevitably terminal patients, including:

- Resuscitation by electric shock

- Lungs ventilation

- Organs transplantation

- Dialysis

- Pain relief

- Organ donation (in case of death)

If family members or Medicare specialists are afraid, no brain activity will be left for the patient after the treatment is over, or there is a high chance the patient will remain unconscious for the rest of their life, the range of the Living Will action may be extended.

Such situations do not necessarily occur when the illness is terminal. Neither do they happen exclusively to people of age. Every single system reacts to disease and is affected by it differently. That is exactly what COVID-19 has shown us once again, and that is why it is never too early or too late to prepare a Living Will.

If the patient does not have an authorized Living Will, the spouse, children, or third parties (significant others) get to decide on the patient’s behalf. However, they may not know about the patient’s relevant wishes and desires. Moreover, in the absence of a person’s legal will confirmation, family members are most likely to disagree with the treatment policy or even sue the medical personnel for it.

Frankly speaking, the distinctive line between a Living Will and a Health Proxy (or Medical Power of Attorney) is very subtle. It may highly depend on the local or state regulation and the drafting requirements. But there are some focal points to help navigate through the entire process. Generally, an MPOA or a Healthcare Proxy can provide professional consultation on a broader range of issues. Plus, with a Living Will, you can only express your wishes related to medicare and its outcomes, while with an MPOA, you get a legal representative who makes all health-related decisions for you.

Last Will

This legal paper is applied to distribute the estate and assets of a deceased person in accordance with their last will. When filling out the document, the person assigns people they want to inherit their monetary or non-monetary accumulations and tangible property. The same applies to inheriting stocks, shares, cash, business assets, and custody over underaged children. Following the decedent’s last will, the beneficiaries acquire their respective rights and responsibilities.

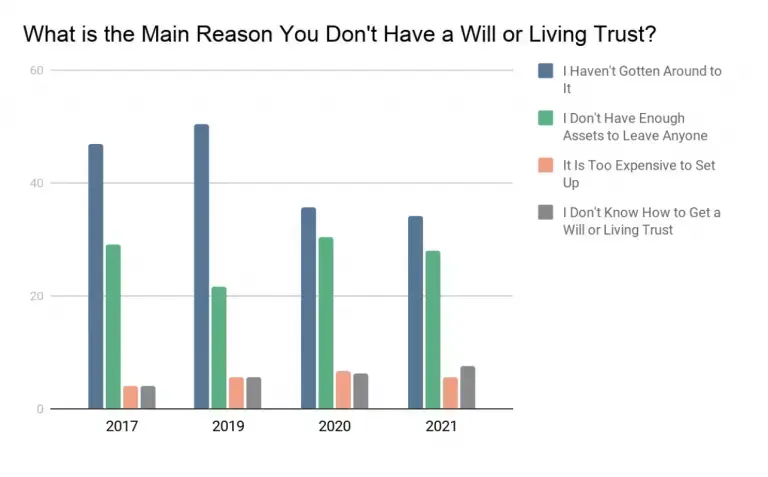

During the pandemic, particular social changes have occurred in issuing and requesting Last Will templates. According to a survey conducted by Caring.com (an organization providing caregiving services), 32% of Americans have created a will because of the COVID-19 fears or because someone they know has contracted the illness. Yet, about a quarter of the population does not have a will at all for various reasons.

Interestingly enough, most people do not get a Will because they believe they do not have enough assets for someone to inherit. Thus, the most recent statistics show the following results (see the table below):

The next most popular misconception is that the government will do all the work for you, and the court will automatically distribute your estate among your heirs. Well, in all fairness, part of it is true: the government will manage your estate after your passing. However, no one said they would do it fairly and squarely or even remotely how you would want it to be done.

There are so many reasons why a Last Will should be a compulsory part of your estate plan, but we have gathered and outlined the five most convincing ones:

- If you do not write a final will yourself, the state will do it for you, and there is no guarantee that yours and the state’s point of view will coincide. For example, if a person passes away without a written will in New York State, the local authorities will leave all your savings and valuable assets to the surviving spouse and children. But in Texas, the decedent’s assets would be only distributed by intestacy probate.

- A verbal agreement between the parties does not count for a full-fledged Last Will. It is a relatively common situation when the spouses agree that the surviving one will get to keep and take care of the joint children if one of them passes away, and then the mother-in-law decides that she wants to be in charge. Unfortunately, cases and precedents like that are widely known to the legal practice. With a written and notarized Last Will, this would not be an issue.

- Nobody is ever immune to fraud. If you have significant accumulations of welfare in possession, we highly recommend you make a will. Once you do, keep several copies of it, just in case, and hire a qualified family law attorney to be your legal representative. Thus, you will nip all possible estate-related disputes in the bud.

- It is a common misconception that young people do not need a will, and because of that, a broad population category is left without legal protection in case of death. The pandemic has resulted in many unexpected deaths, and people were left hopeless in situations they were not legally equipped or even mentally prepared for. Remember that having a will does not mean you are pessimistic but pragmatic.

- Today, you can comprise a will without any legal help using online form-building software and services. It will cost you under $40, but you and your family will be legally protected from any unexpected circumstances that might come your way.

Please remember to make timely updates to your Last Will if you have anything to add, amend, or eliminate. If an argument occurs, the court will decide based on the last updated and notarized version you leave behind.

Sure, additional legal forms can make changes to the will regardless of what is stated there, such as life insurance policy, retirement plan, trust- and transfer-on-death. In legal terms, they are social contracts and come into force independently.

To Sum It All Up

The global pandemic has changed our approach to many things, the uncertainty even more so. That is why people around the world have independently come to the same conclusion: it is better to appreciate and preserve what you have, and it is necessary to create a legal protection basis to avoid any unwanted stress and emotional hardship.

Luckily, nowadays, you do not even have to leave your home to make legal adjustments. All you need to do is find certified online tools that will help you build and customize any legal form you need. Moreover, you can follow illustrated step-by-step filing instructions that will lead you through the entire process. We refresh our database regularly, so you can always find up-to-date form templates on our official website.