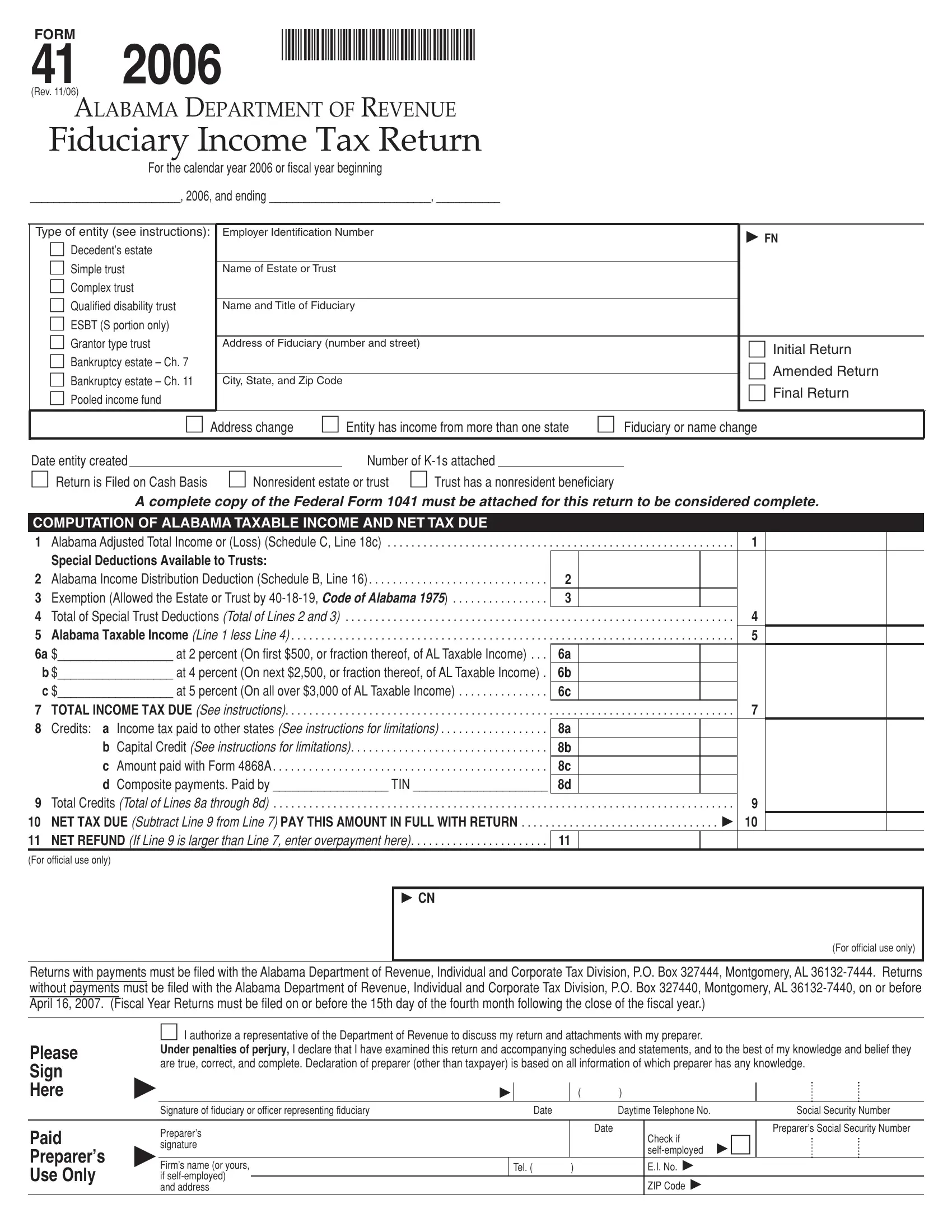

Who Needs to File Alabama Form 41

Alabama Form 41 must be filed by any fiduciary managing an estate or trust with Alabama-source income. The following entities are required to file:

- Decedent's estates, including probate estates

- Simple trusts that distribute all income annually to beneficiaries

- Complex trusts that accumulate income, distribute corpus, or make charitable contributions

- Grantor trusts and revocable living trusts with Alabama income

- Bankruptcy estates under Chapter 7 or Chapter 11 of the U.S. Bankruptcy Code

The fiduciary, which may be an executor, trustee, personal representative, or court-appointed administrator, signs the return and is responsible for ensuring the estate or trust meets its Alabama tax obligations.

What to Gather Before Completing the Form

Have the following documents and information ready before starting Alabama Form 41:

- Federal Employer Identification Number (EIN) for the estate or trust

- Fiduciary's name, mailing address, and telephone number

- Completed federal Form 1041 (used as the starting point for Alabama figures)

- Records of all income received: dividends, interest, rents, capital gains, and other income

- Documentation of all deductions, including administrative fees, professional fees, and distributions to beneficiaries

- Records of any estimated tax payments made during the year

- Charitable contribution records if the estate or trust made deductible charitable gifts

How to Complete Alabama Form 41 Step by Step

Follow these steps to fill out the Fiduciary Income Tax Return accurately:

- Enter the estate or trust identification details. Provide the legal name of the estate or trust, the EIN, the fiduciary's contact information, and the tax year covered by the return.

- Select the entity type. Mark the correct box: decedent's estate, simple trust, complex trust, grantor trust, or bankruptcy estate. This determines which schedules apply.

- Report gross income. List all Alabama-source income by category, including interest, dividends, business income, capital gains, rents, and any other income.

- Enter deductions. Deduct trustee fees, attorney fees, accounting fees, interest on estate debts, and other administration costs permitted under Alabama law.

- Complete Schedule A. If the estate or trust made deductible charitable contributions during the year, calculate the charitable deduction on Schedule A and carry the total to the main form.

- Complete Schedule B. If distributions were made to beneficiaries, calculate the income distribution deduction on Schedule B to reduce the estate or trust's taxable income.

- Complete Schedule G. Use Schedule G to record Alabama-specific adjustments, including modifications required under the Subchapter J and Business Trust Conformity Act effective after December 31, 2004.

- Compute Alabama taxable income. Subtract total deductions and Schedule G adjustments from gross income to arrive at Alabama taxable income.

- Calculate the net tax due. Apply the Alabama fiduciary income tax rate to taxable income, then subtract any credits and estimated tax payments already made.

- Sign and certify the return. The fiduciary or an authorized officer must sign under penalties of perjury, provide the date, and include the paid preparer's information if applicable.

- File by the deadline. Submit the return and any payment due by April 15 for calendar-year filers, or by the 15th day of the fourth month after a fiscal year closes.

Common Questions About Alabama Form 41

What is the deadline for Alabama Form 41?

Calendar-year filers must file by April 15. Fiscal-year filers must file by the 15th day of the fourth month after the close of the tax year. Extensions to file are available, but they do not extend the time to pay any tax owed. Any balance due must be paid by the original deadline to avoid penalties and interest charges.

How do I get an extension for Alabama Form 41?

Alabama grants an automatic six-month extension if you attach a copy of the approved federal extension (Form 7004) to your Alabama return when you file, or if you file the Alabama extension form by the original due date. Remember that the extension covers the filing date only, not the payment date.

What penalties apply to late or incorrect filings?

Alabama imposes a penalty of 5% per month on any unpaid tax after the due date, up to a maximum of 25% of the tax owed. Interest also accrues on unpaid balances at the rate set by the Alabama Department of Revenue. Filing on time and paying any balance due by the original deadline avoids these charges.

Are there other Alabama tax forms related to Form 41?

Yes. Fiduciaries may also need to complete Alabama Form A-1 for employer withholding obligations, or use Alabama Form 8453 as the electronic filing signature document when e-filing. For the decedent's final individual income tax return, use Alabama Form 40. Beneficiaries who received distributions may need to report that income on Alabama Form 40A.