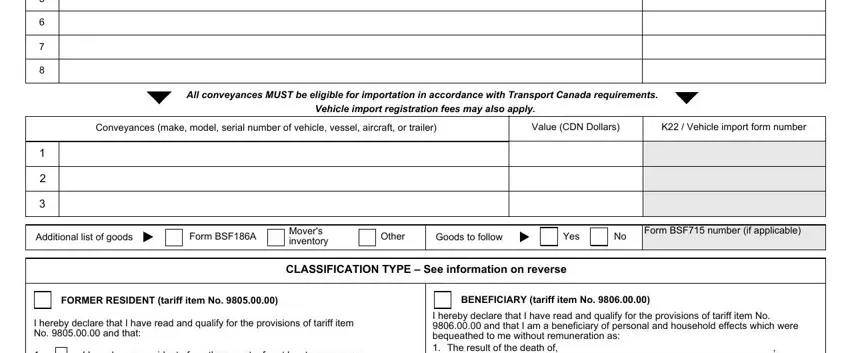

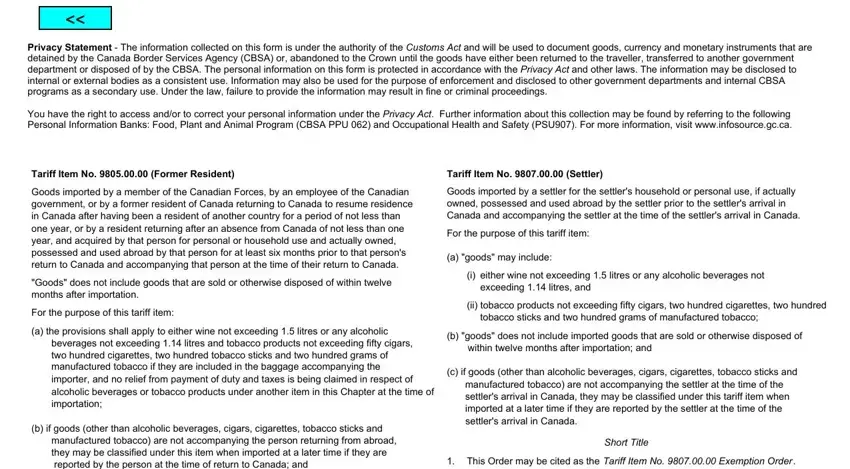

Tariff Item No. 9805.00.00 (Former Resident)

Goods imported by a member of the Canadian Forces, by an employee of the Canadian government, or by a former resident of Canada returning to Canada to resume residence in Canada after having been a resident of another country for a period of not less than one year, or by a resident returning after an absence from Canada of not less than one year, and acquired by that person for personal or household use and actually owned, possessed and used abroad by that person for at least six months prior to that person's return to Canada and accompanying that person at the time of their return to Canada.

"Goods" does not include goods that are sold or otherwise disposed of within twelve months after importation.

For the purpose of this tariff item:

(a)the provisions shall apply to either wine not exceeding 1.5 litres or any alcoholic beverages not exceeding 1.14 litres and tobacco products not exceeding fifty cigars, two hundred cigarettes, two hundred tobacco sticks and two hundred grams of manufactured tobacco if they are included in the baggage accompanying the importer, and no relief from payment of duty and taxes is being claimed in respect of alcoholic beverages or tobacco products under another item in this Chapter at the time of importation;

(b)if goods (other than alcoholic beverages, cigars, cigarettes, tobacco sticks and manufactured tobacco) are not accompanying the person returning from abroad, they may be classified under this item when imported at a later time if they are reported by the person at the time of return to Canada; and

(c)any article which was acquired after March 31, 1977 by a class of persons

named in this tariff item and which has a value for duty as determined under the Customs Act of more than $10,000 shall not be classified under this tariff item.

Section 84 of the Customs Tariff reads:

84.Goods that, but for the fact that their value for duty as determined under section 46 of the Customs Act exceeds the value specified under tariff item No. 9805.00.00, would be classified under that tariff item, shall be classified under Chapters 1 to 97 and their value for duty reduced by that specified value.

Short Title

1.This Order may be cited as the Tariff Item No. 9805.00.00 Exemption Order.

Interpretation

2.In this Order,

"bride's trousseau" means goods acquired for use in the household of a newly married couple, but does not include vehicles, vessels or aircraft;

"wedding presents" means goods of a non-commercial nature received by a person as personal gifts in consideration of that person's recent marriage or the anticipated marriage of that person within three months of the person's return to Canada.

Exemption

3.The following goods are exempt from the six-month ownership, possession or use requirements set out in tariff item No. 9805.00.00 of the Customs Tariff :

(a)alcoholic beverages owned by, in the possession of and imported by a person who has attained the minimum age at which a person may lawfully purchase alcoholic beverages in the province in which the CBSA Office where the alcoholic beverages are imported is situated;

(b)tobacco products owned by and in the possession of the importer;

(c)a bride's trousseau owned by, in the possession of and imported by a recently married person or a bride-to-be whose anticipated marriage is to take place within three months of the date of her return to Canada;

(d)wedding presents owned by, in the possession of, and imported by the recipient thereof;

(e)any goods imported by a person who has resided abroad for at least five years immediately prior to returning to Canada and who, prior to the date of return, owned, was in possession of and used the goods; and

(f)goods acquired as replacements for goods that, but for their loss or destruction as the result of fire, theft, accident or other unforeseen contingency, would have been classified under tariff item No. 9805.00.00 of the Customs Tariff, on condition that

(i)the goods acquired as replacements are of a similar class and approximately of the same value as the goods they replaced,

(ii)the goods acquired as replacements were owned by, in the possession of, and used by a person prior to the person's return to Canada, and

(iii)evidence is produced at the time the goods are accounted for under section 32 of the Customs Act that the goods they replaced were lost or destroyed as the result of fire, theft, accident or other unforeseen contingency.

Tariff Item No. 9806.00.00 (Beneficiary)

Personal and household effects of a resident of Canada who has died, on the condition that such goods were owned, possessed and used abroad by that resident;

Personal and household effects received by a resident of Canada as a result of the death or in anticipation of death of a person who is not a resident of Canada, on condition that such goods were owned, possessed and used abroad by that non-resident;

All the foregoing when bequeathed to a resident of Canada.

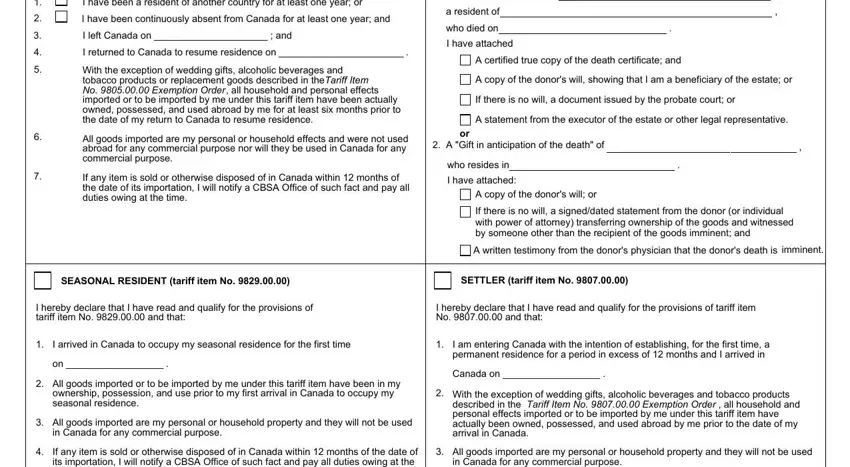

Tariff Item No. 9807.00.00 (Settler)

Goods imported by a settler for the settler's household or personal use, if actually owned, possessed and used abroad by the settler prior to the settler's arrival in Canada and accompanying the settler at the time of the settler's arrival in Canada.

For the purpose of this tariff item:

(a)"goods" may include:

(i)either wine not exceeding 1.5 litres or any alcoholic beverages not exceeding 1.14 litres, and

(ii)tobacco products not exceeding fifty cigars, two hundred cigarettes, two hundred tobacco sticks and two hundred grams of manufactured tobacco;

(b)"goods" does not include imported goods that are sold or otherwise disposed of within twelve months after importation; and

(c)if goods (other than alcoholic beverages, cigars, cigarettes, tobacco sticks and manufactured tobacco) are not accompanying the settler at the time of the settler's arrival in Canada, they may be classified under this tariff item when imported at a later time if they are reported by the settler at the time of the settler's arrival in Canada.

Short Title

1.This Order may be cited as the Tariff Item No. 9807.00.00 Exemption Order. Interpretation

2.The following goods are exempt from the use requirements specified in tariff item No. 9807.00.00 :

(a)alcoholic beverages imported by a settler who has attained the minimum age at which a person may lawfully purchase alcoholic beverages in the province in which the customs office where the alcoholic beverages are imported is situated;

(b)tobacco products;

(c)household goods acquired by a settler and set aside for use in the household of the settler whose marriage occurred within three months before the settler's arrival in Canada or is to occur within three months after the settler's arrival in Canada; and

(d)wedding gifts received outside Canada by a settler in consideration of the settler's marriage which occurred within three months before the settler's arrival in Canada or is to occur within three months after the settler's arrival in Canada.

Tariff Item No. 9829.00.00 (Seasonal Resident)

Household furniture and furnishings for a seasonal residence, excluding construction materials, electrical fixtures or other goods permanently attached to or incorporated into a seasonal residence;

Tools and equipment for the maintenance of a seasonal residence;

The foregoing, on condition that:

(i)the goods are imported by a person who is not a resident of Canada and who owns or leases for not less than three years a residence in Canada for seasonal use, other than a time-sharing residence, trailer or mobile home;

(ii)the person is entitled to only one importation for each seasonal residence under this tariff item;

(iii)the goods are for the personal use of that person or their family and are not for any commercial, industrial or occupational purpose;

(iv)the goods are owned, possessed and used by that person or their family before their first arrival in Canada to occupy the seasonal residence;

(v)the goods are not sold or otherwise disposed of in Canada for at least one year after the date of their importation; and

(vi)the goods accompany the seasonal resident at the time of the seasonal resident's first

arrival in Canada to occupy the seasonal residence or, if not imported at the time of first arrival in Canada, are, at that time, described and listed on a customs accounting document as goods to follow.

NOTE FOR FORMER RESIDENTS AND SETTLERS TO CANADA (TARIFF ITEM NOS. 9805.00.00 AND 9807.00.00)

A minimum duty applies to cigarettes, tobacco sticks, and manufactured tobacco that you include in your personal exemption entitlement. However, this duty does not apply if the products have an excise stamp "DUTY PAID CANADA DROIT ACQUITTÉ".

Please refer to section 21 of the Customs Tariff for legislative references.