BIR Form 1601-F can be opened and reviewed online very easily. Simply use the FormsPal PDF editor to view and work with the form right away. Our tool lets you open, review, and fill in any PDF form in a few clicks. To begin, follow these steps below:

Step 1: Click the orange "Get Form" button at the top of this page. This will open the BIR Form 1601-F in the FormsPal online PDF editor.

Step 2: Once the BIR Form 1601-F is open in the editor, you can enter information directly into the form fields. The form requires the following key details to be completed accurately:

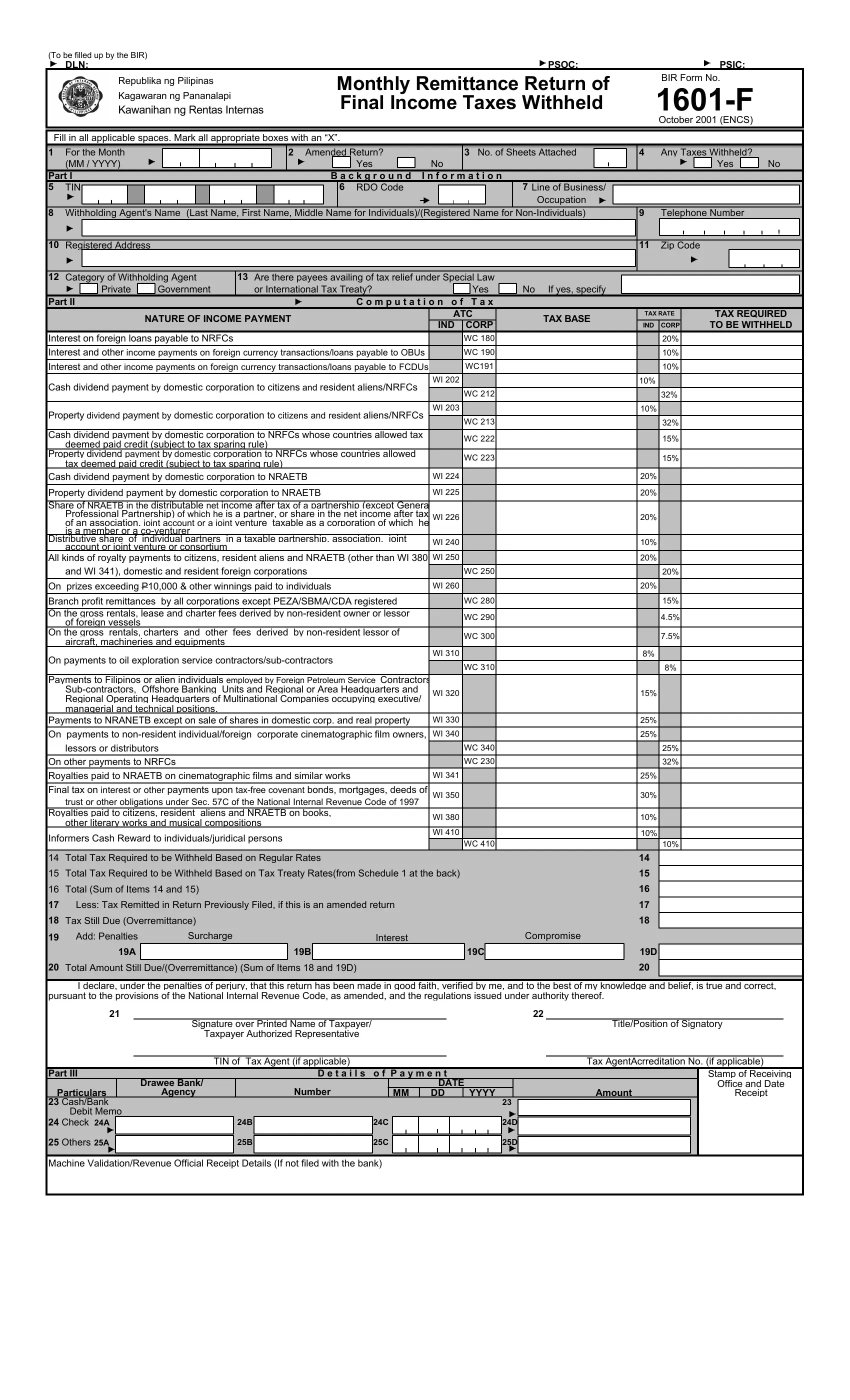

1. In Part I, enter the withholding agent's taxpayer identification number (TIN), registered name, trade name (if any), registered address, zip code, RDO code, line of business or occupation, and taxpayer classification. Also indicate the taxable year and the month the return covers.

2. In the next section, select whether this is an original or amended return. For amended returns, state the reason for the amendment. All withholding agents filing their return manually must also indicate whether they are filing under the large taxpayer division or through a regular RDO.

3. Complete Part II by entering each income payment type, the applicable ATC code, the gross income payment amount, the applicable final withholding tax rate, and the total amount of final taxes withheld during the month. Each income category has a separate row and ATC code assigned by the BIR.

4. In Part III, compute the total taxes due by summing all final withholding tax amounts from Part II. Deduct any prior payments or tax credits applied to the current return to arrive at the net tax still payable. Enter any penalties, surcharges, or interest due if the filing is late.

5. The authorized representative or withholding agent must sign and date the return in the signature block. Include the printed name, title, and TIN of the signatory. For corporations, the president, vice president, or other principal officer may sign the return.

Step 3: Once all required fields are completed, click "Done" to save the completed BIR Form 1601-F. You can then download the filled PDF and submit it, together with the corresponding tax payment, at any authorized agent bank (AAB) within the jurisdiction of your Revenue District Office (RDO), or file electronically via the BIR eFPS system. FormsPal keeps your data secure and does not store personal information entered into forms.

Frequently asked questions

What is BIR Form 1601-F used for?

BIR Form 1601-F is the Monthly Remittance Return of Final Income Taxes Withheld. Withholding agents in the Philippines use this form to report and remit final income taxes deducted from income payments such as dividends, royalties, interest on bank deposits, prizes, and other passive income subject to final withholding tax rates under the NIRC.

Who is required to file BIR Form 1601-F?

All withholding agents, including corporations, partnerships, sole proprietors, government agencies, and individuals in business, who make income payments subject to final withholding tax must file this form monthly. This applies whether the agent uses the eFPS electronic filing system or files manually at an authorized agent bank.

What is the monthly deadline for filing BIR Form 1601-F?

Non-eFPS withholding agents must file BIR Form 1601-F and remit the taxes withheld on or before the 10th day of the following month. eFPS filers follow the BIR staggered filing schedule, which varies by industry group. Failure to file on time results in a 25% surcharge, 12% annual interest, and compromise penalties based on the tax unpaid.

What income payments are covered by BIR Form 1601-F?

The form covers income payments subject to final withholding tax under the NIRC, including interest on time and savings deposits, royalties on books and other works, cash dividends from domestic corporations, prizes and winnings above the tax-exempt amount, income of non-resident foreign corporations, and income from international carriers doing business in the Philippines.

Where do I submit the completed BIR Form 1601-F?

Manual filers submit BIR Form 1601-F and the related tax payment at any authorized agent bank (AAB) within the jurisdiction of the RDO where the withholding agent is registered. In areas without an AAB, filers submit directly at the RDO cashier. eFPS users file and pay electronically through the BIR eFPS portal.

For other BIR forms, see BIR Form 1601-C for compensation tax remittances, BIR Form 1601-E for creditable withholding taxes, and BIR Form 2306 for the certificate of final tax withheld at source.