To fill out the BIR Form 1601-C online, there is no need to download any additional software. Use our free PDF editor to complete the form directly in your browser. The editor is regularly updated with new features to make form completion fast and accurate.

Follow these steps to complete your BIR Form 1601-C:

Step 1: Click the "Get Form" button at the top of this page to open the online editor.

Step 2: Use the PDF editing tools to fill in all required fields. You can add text, correct existing entries, and sign the document. The editor supports typing directly into form fields, adding notes, and inserting images if needed.

The form requires specific data about compensation, tax withheld, and remittance details. Take time to gather the following before starting:

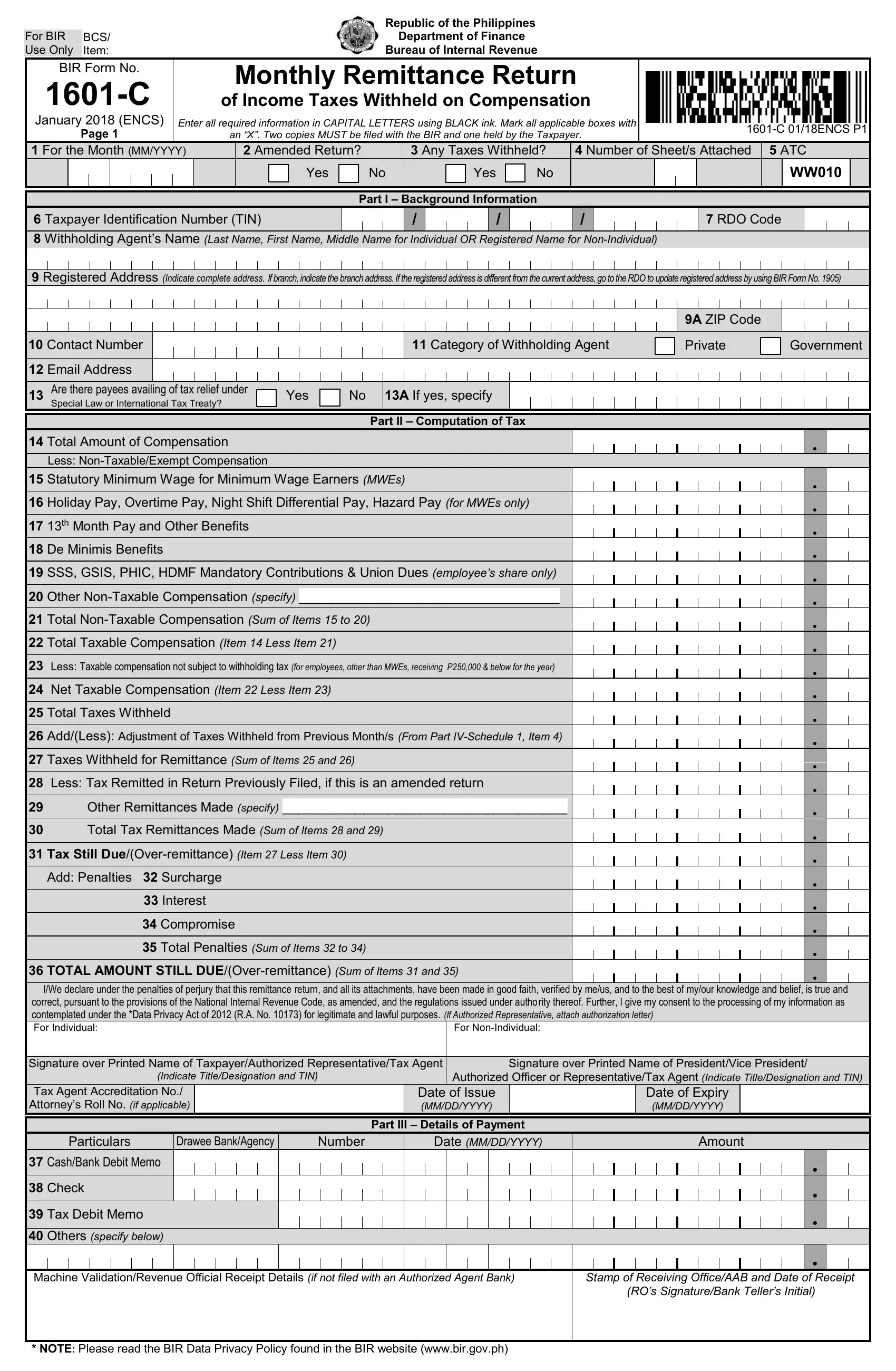

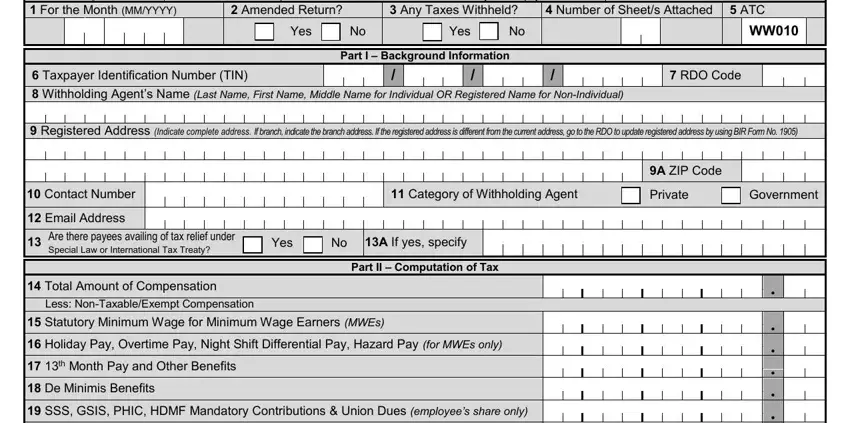

1. Complete the taxpayer information section, including the TIN, withholding agent name, address, and the taxable month covered. Accurate taxpayer details are critical for BIR matching and compliance checks.

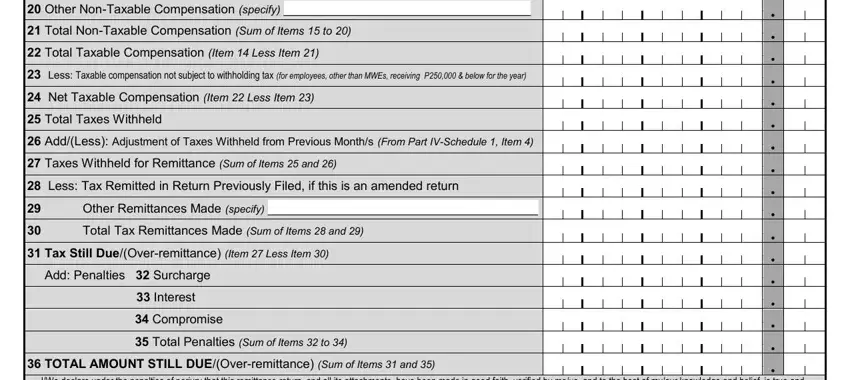

2. Enter the compensation details in the next section. Fill in the total taxable compensation, any non-taxable amounts, taxes withheld, and the net amount still due. Double-check each figure against your payroll records before continuing. Fields include Other NonTaxable Compensation, Total NonTaxable Compensation Sum, Total Taxable Compensation, Net Taxable Compensation, and Total Taxes Withheld.

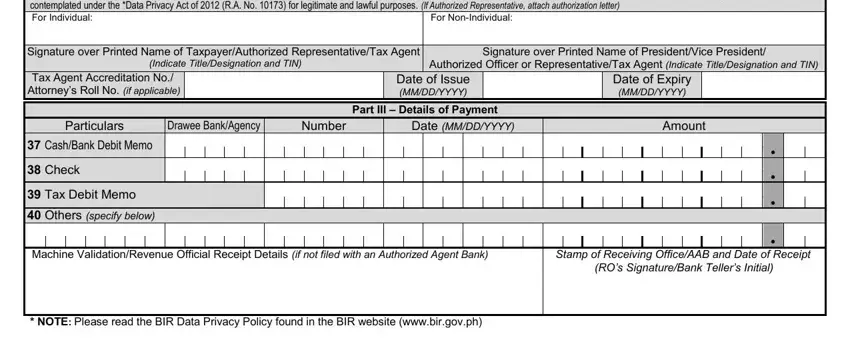

3. Complete the certification and signature section. Include the printed name, title, TIN, and tax agent accreditation number if applicable. Also fill in the Date of Issue, payment particulars, and the drawee bank or agency details. This section confirms your declaration under BIR penalties.

Review the Authorized Officer section carefully before submitting. Any errors in this area may require an amendment filing.

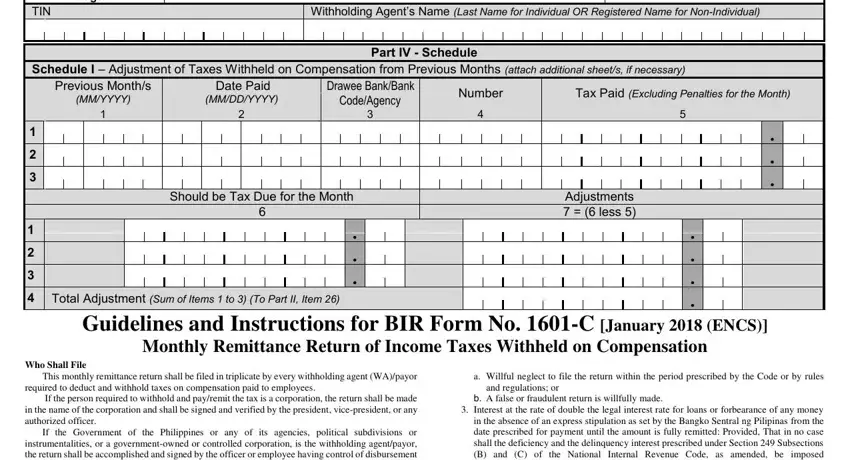

4. Complete Schedule I (Adjustment of Taxes) on page two if applicable. Fill in the Page, TIN, Withholding Agent Name, Previous Months data, Drawee Bank or Agency, Date Paid, Tax Paid excluding penalties, and the Should Be Tax Due amount for the current month.

Step 3: Review all entries for accuracy, then click "Done." After creating a free account on FormsPal.com, you can download the completed BIR Form 1601-C as a PDF or send it by email. Your form is saved to your account for future access and reference.

FormsPal also provides access to other BIR forms you may need. Use BIR Form 1601-E for expanded withholding taxes, BIR Form 1601-F for final withholding taxes on certain income, and BIR Form 1701Q for quarterly income tax returns. For the annual income tax return, see BIR Form 1701. You can also find BIR Form 0613 and BIR Form 0605 in our library.