Our top web programmers worked hard to implement the PDF editor we are now excited to present to you. Our application can help you quickly prepare rrf 1 california and saves your time. Simply comply with this particular procedure.

Step 1: This web page contains an orange button stating "Get Form Now". Press it.

Step 2: Right now, you can begin modifying the rrf 1 california. Our multifunctional toolbar is available to you - add, remove, alter, highlight, and perform other commands with the content in the document.

Feel free to provide the following details to prepare the rrf 1 california PDF:

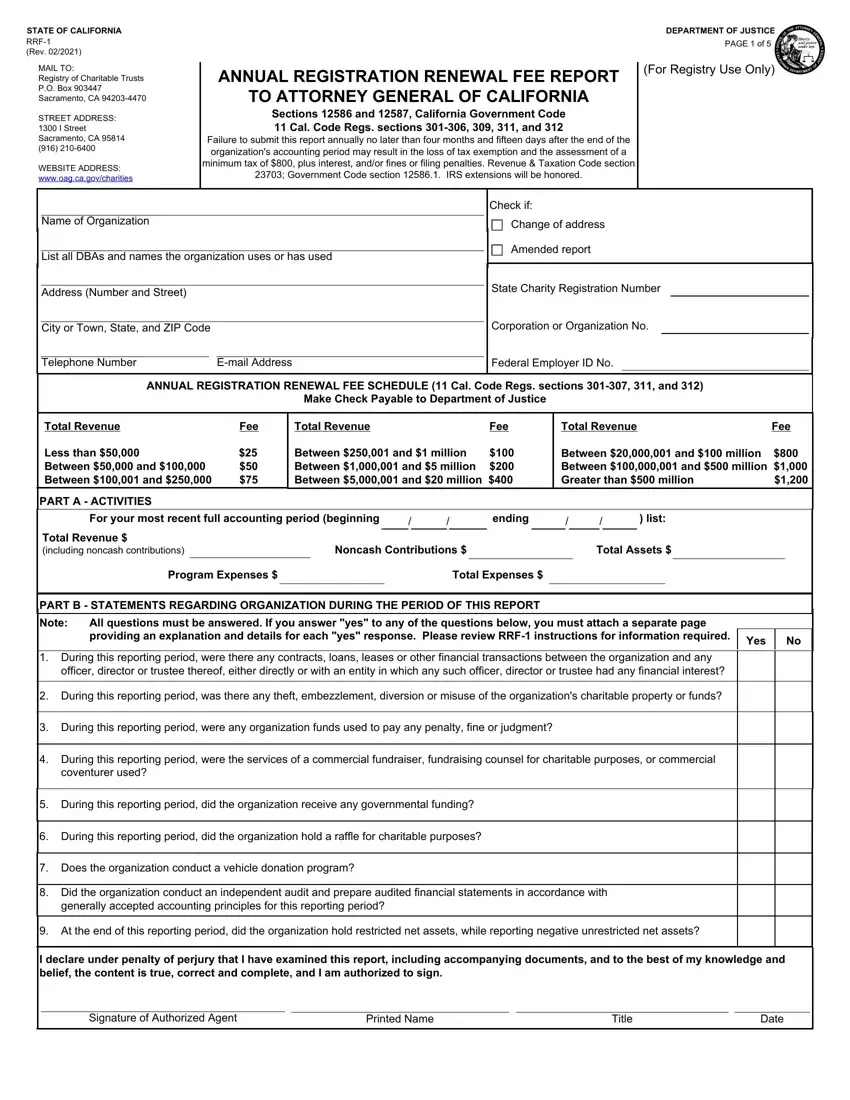

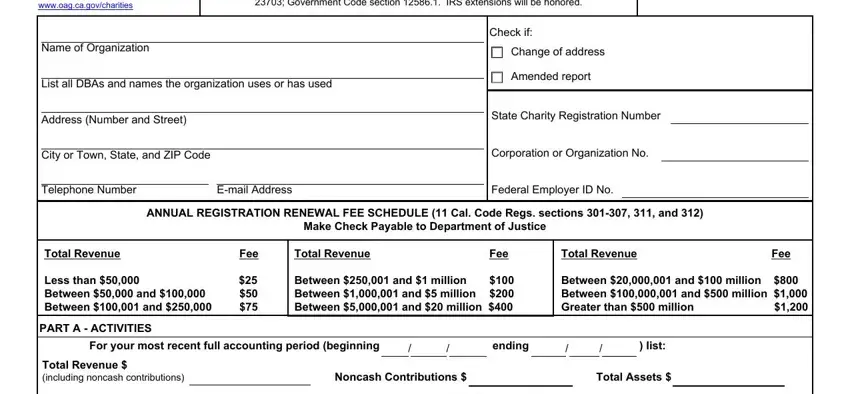

Please put down the data in the field Program Expenses, Total Expenses, PART B STATEMENTS REGARDING, Note, All questions must be answered If, Yes, During this reporting period were, During this reporting period was, During this reporting period were, During this reporting period were, During this reporting period did, During this reporting period did, Does the organization conduct a, Did the organization conduct an, and At the end of this reporting.

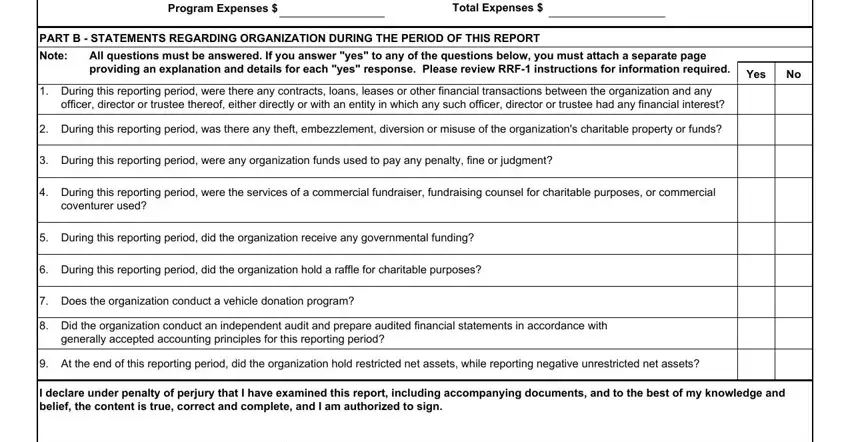

Within the area talking about The State Charity Registration, OTHER IDENTIFICATION NUMBERS, The corporation number is a, The organization number is a, The Federal Employer, Total Assets Are resources owned, Program Expenses Are expenses, Total Expenses Are all expenses, The following will assist you in, PART B, PART A, and PART B QUESTION If yes provide, it's essential to type in some vital details.

Step 3: Choose the button "Done". Your PDF form is available to be exported. You will be able upload it to your pc or send it by email.

Step 4: To prevent yourself from any specific complications in the future, you will need to make minimally a few copies of your document.