You could prepare m3 exempt application easily with the help of our online PDF editor. To make our editor better and easier to use, we consistently implement new features, taking into consideration suggestions coming from our users. If you're looking to begin, here's what it will require:

Step 1: Just click on the "Get Form Button" at the top of this webpage to see our pdf file editing tool. Here you'll find all that is needed to work with your file.

Step 2: Using our state-of-the-art PDF editor, you're able to do more than just fill in blank fields. Try all the functions and make your documents appear great with customized text added, or fine-tune the original input to perfection - all supported by the capability to incorporate any pictures and sign the document off.

This PDF form will need particular information to be entered, so ensure that you take whatever time to enter what's expected:

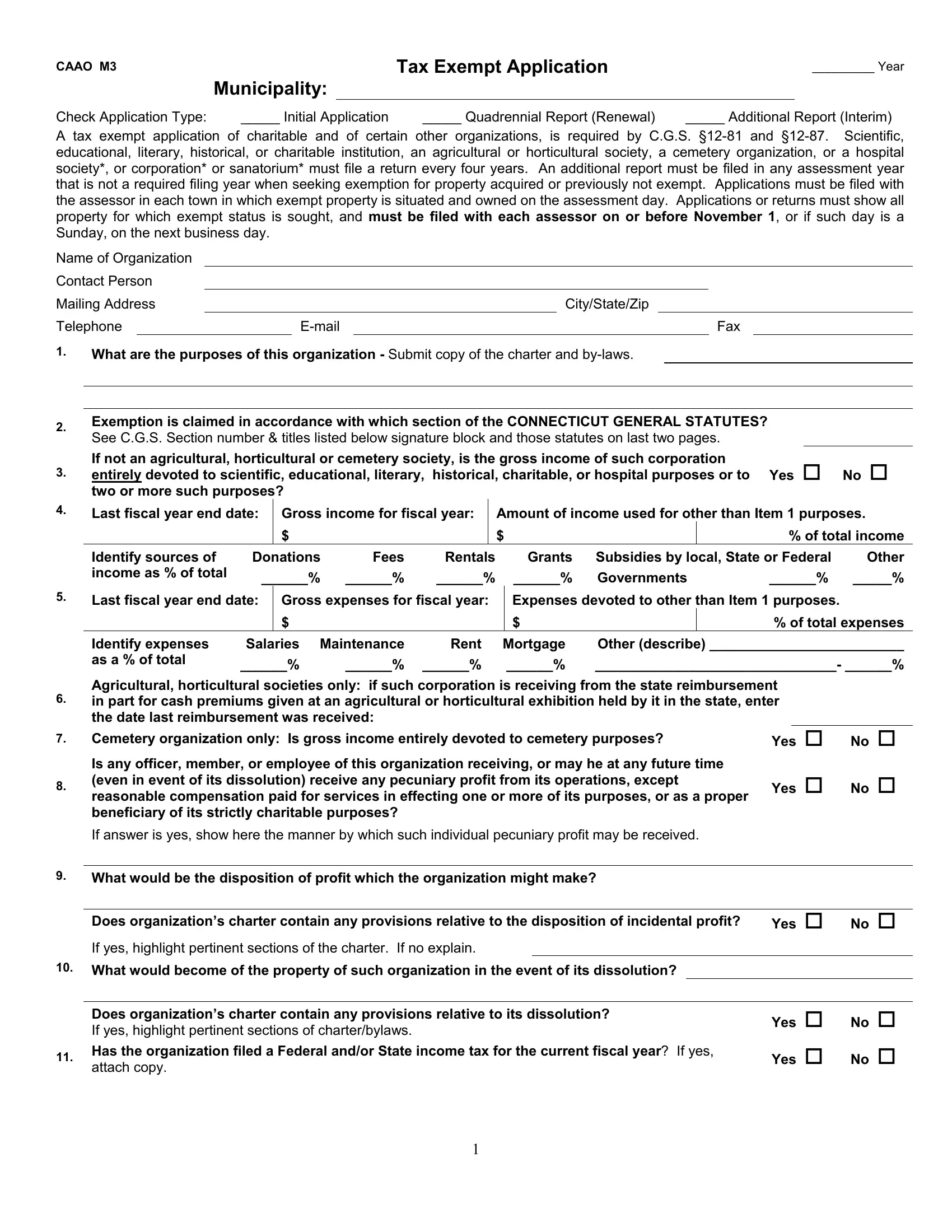

1. First, while filling out the m3 exempt application, start out with the part that includes the next blank fields:

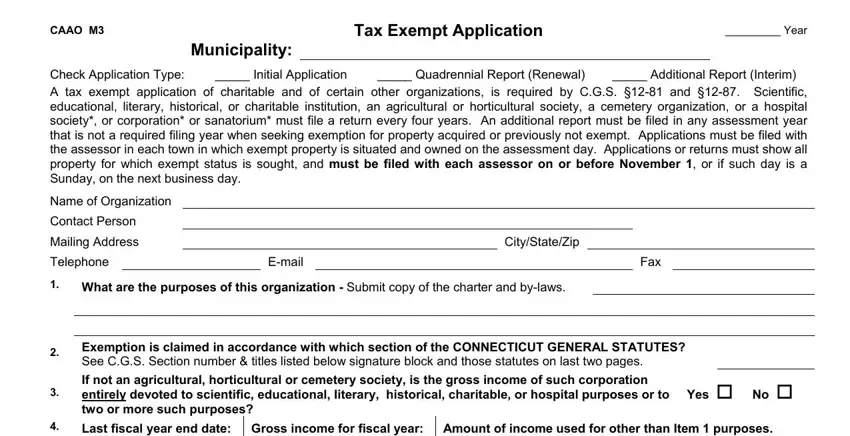

2. Just after this part is filled out, go on to enter the applicable information in these - Last fiscal year end date Gross, of total income, Identify sources of income as of, Donations, Fees, Rentals, Grants, Subsidies by local State or Federal, Other, Governments , Last fiscal year end date Gross, Expenses devoted to other than, Identify expenses as a of total, of total expenses, and Salaries.

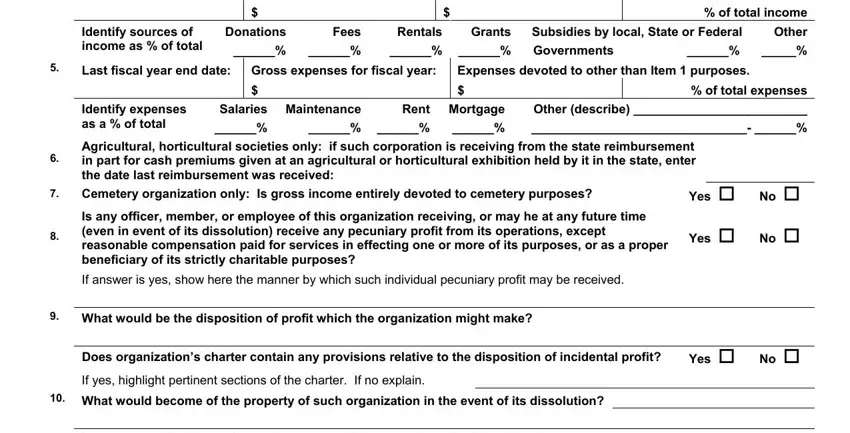

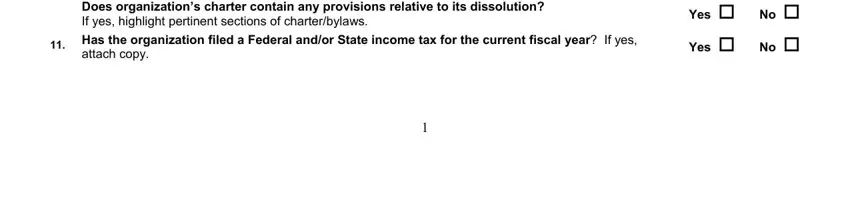

3. Completing Does organizations charter contain, Has the organization filed a, attach copy, Yes , No , Yes , and No is essential for the next step, make sure to fill them out in their entirety. Don't miss any details!

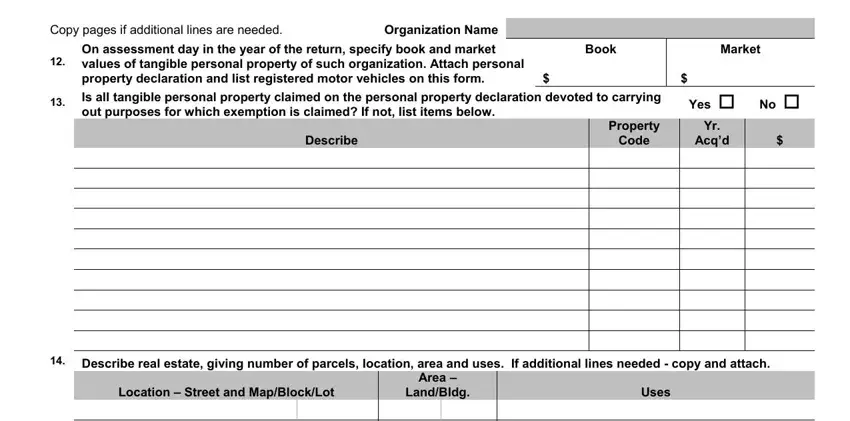

4. This next section requires some additional information. Ensure you complete all the necessary fields - Copy pages if additional lines are, Organization Name, On assessment day in the year of, Book, Market, Is all tangible personal property, Yes , No , Describe, Property, Code, Acqd, Describe real estate giving, Location Street and MapBlockLot, and Area - to proceed further in your process!

It's very easy to make errors while completing your Yes , hence ensure that you reread it prior to when you finalize the form.

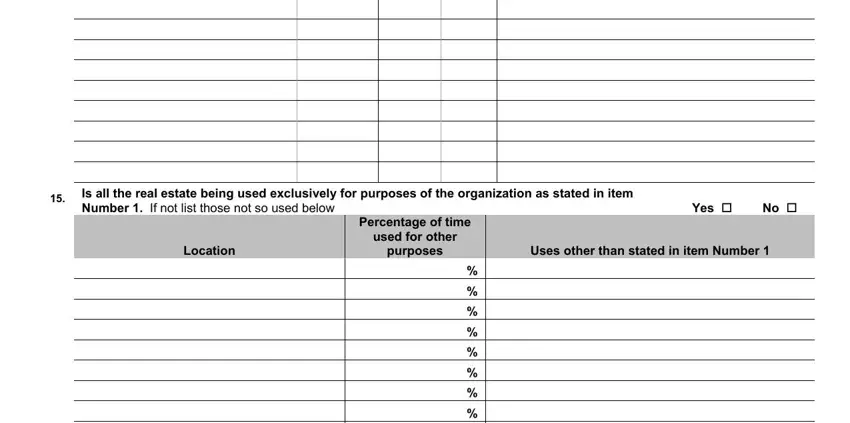

5. While you draw near to the completion of this document, there are actually a couple extra requirements that have to be satisfied. In particular, Is all the real estate being used, Yes , No , Location, Percentage of time, used for other, purposes, and Uses other than stated in item should be filled out.

Step 3: Ensure the information is right and then click "Done" to conclude the task. Go for a 7-day free trial plan with us and get immediate access to m3 exempt application - downloadable, emailable, and editable in your FormsPal account. When using FormsPal, you'll be able to complete forms without the need to be concerned about database incidents or entries getting distributed. Our protected software ensures that your personal information is maintained safely.

Related Tax Forms for Connecticut Organizations

Organizations filing the CAAO M3 Tax Exempt Application may also need these related Connecticut forms:

- ST-3 Tax Exemption Certificate - for Connecticut sales and use tax exemptions

- Charitable Donation Request Form - for documenting contributions to qualifying organizations

- Charitable Organization Worksheet - for annual nonprofit financial reporting