General Purpose: A qualifying exempt organization must issue this certificate to retailers when purchasing items to be used by the organization exclusively for the purposes for which it was established. Under Conn. Gen. Stat. §12-412(8), a qualifying exempt organization is either:

•An organization issued an exemption permit by the Department of Revenue Services (DRS) under Conn. Agencies Regs. §12-426-15, if the permit has not been canceled or revoked by DRS; or

•An organization that is exempt from federal income tax under I.R.C. §501(a) and has been issued a determination letter by the U.S. Treasury Department as an organization described in I.R.C. §501(c)(3) or (13), if the determination letter has not been revoked by the Internal Revenue Service (IRS).

A qualifying exempt organization may use this certificate to purchase any tangible personal property for resale at one of five fundraising or social events of a day’s duration during any calendar year. The event must be exempt from tax under Conn. Gen. Stat. §12-412(94). Otherwise, exempt organizations are not allowed to purchase tangible personal property for resale with this certificate. See Special Notice 98(11), Exemption From Sales and Use Taxes of Sales by Nonprofit Organizations at Fundraising or Social Events.

Purchases of Meals and Lodging: In general, qualifying exempt organizations may not use this certificate to purchase meals and lodging, but must get preapproval from DRS for these purchases, and use CERT-112, Exempt Purchases of Meals and Lodging by Exempt Entities, or CERT-123, Blanket Certificate for Exempt Qualifying Purchases of Meals or Lodging by an Exempt Entity.

However, a qualifying exempt organization may purchase meals tax exempt using this certificate, without prior approval from DRS, when it will resell the meals at one of five fundraising or social events per year exempt under Conn. Gen. Stat. §12-412(94). See Policy Statement 2003(4), Purchases of Meals of Lodging by Exempt Entities.

If the purchaser is not a qualifying exempt organization or does not use the property or services purchased exclusively for the purposes for which the organization was established, the purchaser owes use tax on the total purchase price of the property or services.

Statutory Authority: Conn. Gen. Stat. §12-412(8) and (94).

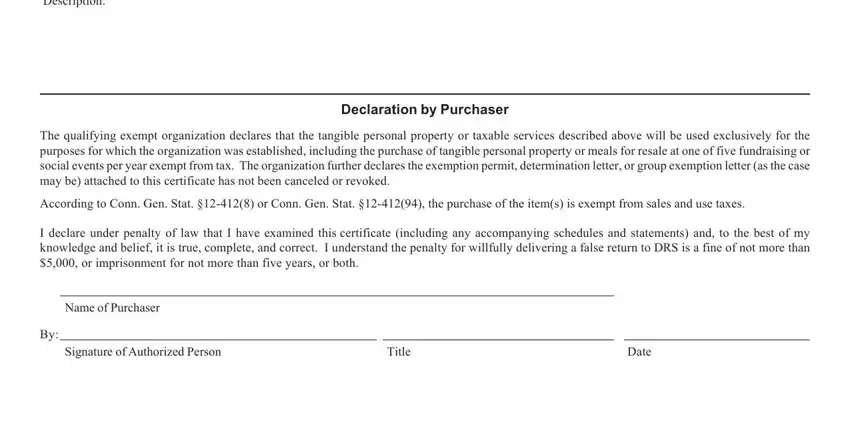

Instructions for the Purchaser: An officer of a qualifying exempt organization must issue and sign this certificate to advise the seller of tangible personal property or taxable services that sales and use taxes do not apply to the purchase. Keep a copy of this certificate, the documents attached, and records that substantiate the information entered on this certificate for at least six years from the date this certificate is issued.

The purchaser must attach to this certificate a copy of the:

•Exemption permit issued to the organization by DRS under Conn. Agencies Regs. §12-426-15; or

•Determination letter or group exemption letter issued by the IRS which establishes that the organization has been determined to be an exempt organization described in I.R.C. §501(c)(3) or (13).

For purchases made on or after January 1, 1996, a qualifying exempt organization covered by a group exemption letter, and that was not issued an exemption permit by DRS under Conn. Agencies Regs. §12-426-15, must attach to this certificate a copy of:

•The group exemption letter issued by the IRS to subordinate organizations (including the qualifying exempt organization) on whose behalf a central organization applied for recognition of exemption;

•The organization’s written consent to the central organization to be covered by the group exemption letter; and

•The central organization’s written notification to the IRS that the organization consents to be covered by the group exemption letter.

Instructions for the Seller: Acceptance of this certificate, when properly completed, relieves the seller from the burden of proving the sale and the storage, use, or consumption of the tangible personal property or taxable services are not subject to sales and use taxes. This certificate is valid only if taken in good faith from a qualifying exempt organization. The good faith of the seller will be questioned if the seller knows of facts that suggest the purchaser is not a qualifying exempt organization.

Keep this certificate, the documents attached, and bills or invoices to the purchaser for at least six years from the date the items or services were purchased. The bills, invoices or records covering the purchase made under this certificate must be marked “Exempt Under CERT-119” to indicate the purchase was exempt.

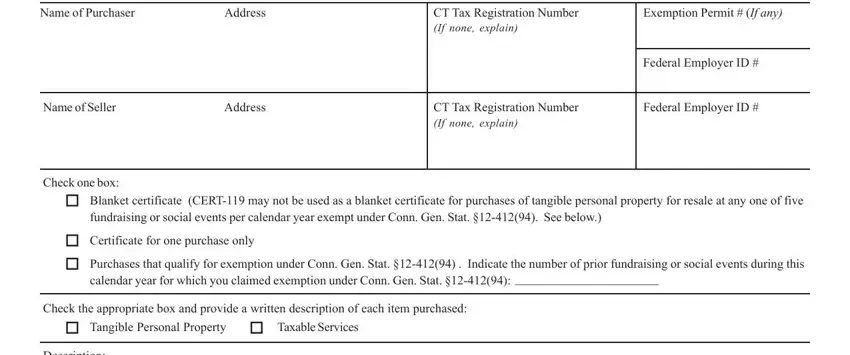

This certificate may be used for a single exempt purchase, in which case the box marked “Certificate for One Purchase Only” must be checked. This certificate may also be used for a continuing line of exempt purchases, in which case the box marked “Blanket Certificate” must be checked. A blanket certificate remains in effect for three years unless the purchaser revokes it in writing before the expiration of the three-year period. CERT-119 may not be used as a blanket certificate for purchases of tangible personal property for resale at any one of five fundraising or social events per calendar year exempt under Conn. Gen. Stat. §12-412(94).

An exempt organization must pay for its exempt purchases by a check drawn on its checking account or by a credit card issued in its name (and not in the name of any of its members or officers). An exempt organization may make a purchase of $10 or less using cash from the organization’s own funds. However, a blanket CERT-119 may not be used for a cash purchase, and a properly completed CERT-119, with the appropriate documents attached, must be issued to the retailer at the time of each cash purchase.

For More Information: Call Taxpayer Services at 1-800-382-9463 (in-state) or 860-297-5962 (from anywhere). TTY, TDD, and Text Telephone users only may transmit inquiries 24 hours a day by calling 860-297-4911. Preview and download forms and publications from the DRS Web site at www.ct.gov/DRS