Understanding the complexities of telecommunication service transactions in New York State requires familiarity with the CT-120 form, a crucial document for resellers in the industry. This Resale Certificate, issued by the New York State Department of Taxation and Finance, serves to authenticate the purchase of telecommunication services for resale purposes without the imposition of excise taxes under certain conditions outlined in Tax Law, Article 9, section 186-e. The CT-120 form distinguishes between single-use and blanket certificates, addressing the ongoing needs of telecommunication resellers who must provide their valid sales tax Certificate of Authority number among other vital information to qualify for these tax exemptions. Resellers are mandated to certify their intent for the purchased services, highlighting the legality and tax obligations tied to their resale activities. Misuse of this certificate not only entails tax liabilities but also hefty penalties and interest, underscoring the document's significance in maintaining tax compliance within the telecommunication resale market. Providers of telecommunication services, on the other hand, are protected from liability when accepting validly completed resale certificates within the stipulated timeframe, hence the emphasis on diligence and good faith in these transactions. With penalties for fraudulent exemption certificates being notably severe, including a 100% tax due and additional fines, the CT-120 form stands as a fundamental regulatory measure for both resellers and providers navigating the telecommunication landscape in New York State.

| Question | Answer |

|---|---|

| Form Name | Ct 120 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 120 york tax form, 120 certificate tax, 120 form state, 120 form tax |

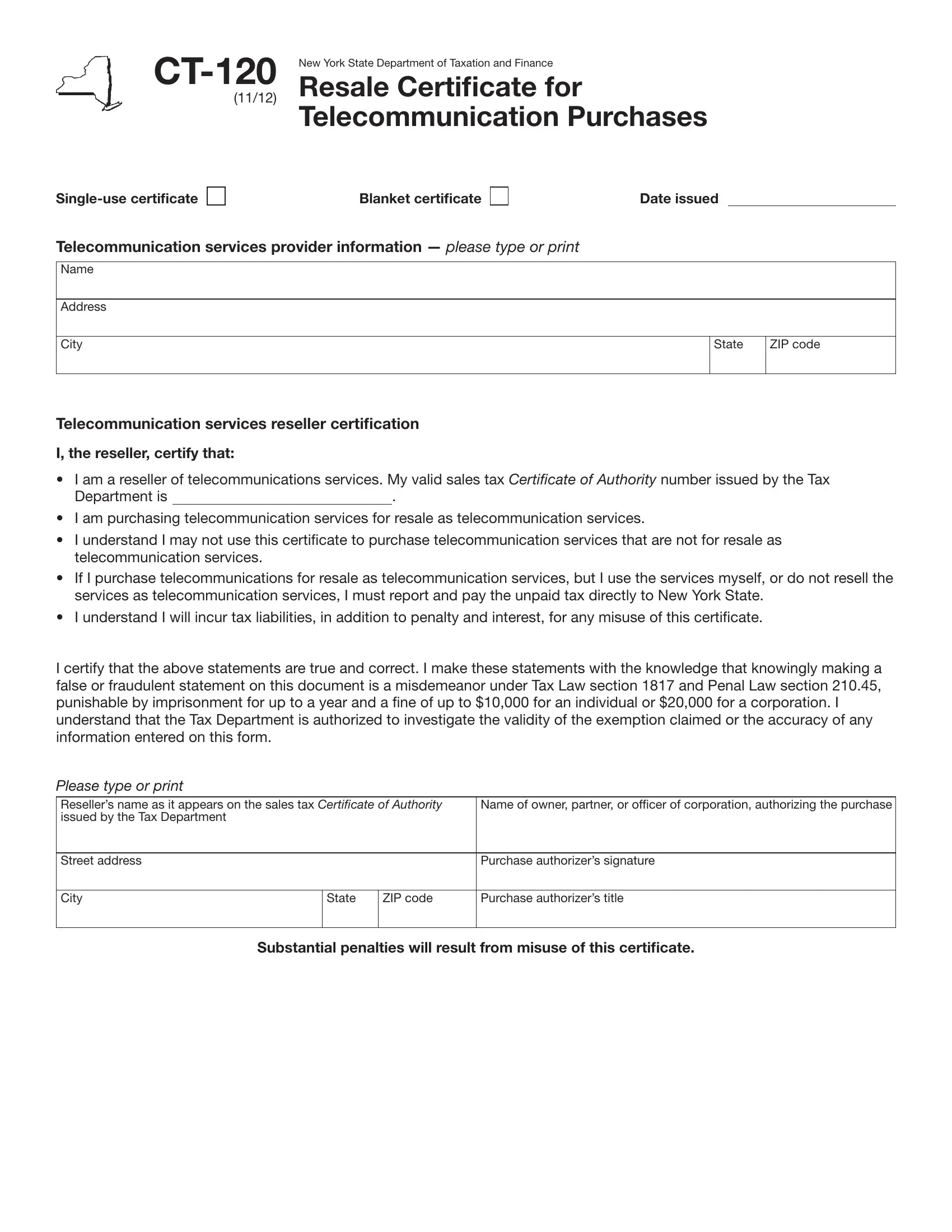

New York State Department of Taxation and Finance |

|

Resale Certificate for |

|

(11/12) |

|

Telecommunication Purchases

Blanket certificate

Date issued

Telecommunication services provider information — please type or print

Name

Address

City

State

ZIP code

Telecommunication services reseller certification

I, the reseller, certify that:

•I am a reseller of telecommunications services. My valid sales tax Certificate of Authority number issued by the Tax

Department is |

|

. |

•I am purchasing telecommunication services for resale as telecommunication services.

•I understand I may not use this certiicate to purchase telecommunication services that are not for resale as telecommunication services.

•If I purchase telecommunications for resale as telecommunication services, but I use the services myself, or do not resell the services as telecommunication services, I must report and pay the unpaid tax directly to New York State.

•I understand I will incur tax liabilities, in addition to penalty and interest, for any misuse of this certiicate.

I certify that the above statements are true and correct. I make these statements with the knowledge that knowingly making a false or fraudulent statement on this document is a misdemeanor under Tax Law section 1817 and Penal Law section 210.45, punishable by imprisonment for up to a year and a ine of up to $10,000 for an individual or $20,000 for a corporation. I understand that the Tax Department is authorized to investigate the validity of the exemption claimed or the accuracy of any information entered on this form.

Please type or print

Reseller’s name as it appears on the sales tax Certificate of Authority |

Name of owner, partner, or oficer of corporation, authorizing the purchase |

||

issued by the Tax Department |

|

|

|

|

|

|

|

Street address |

|

|

Purchase authorizer’s signature |

|

|

|

|

City |

State |

ZIP code |

Purchase authorizer’s title |

|

|

|

|

Substantial penalties will result from misuse of this certificate.

Page 2 of 2

Instructions

General information

Form

This certiicate is only for use by a reseller of telecommunication services who:

•is registered as a New York State sales tax vendor ;

•has a valid sales tax Certificate of Authority issued by the Tax

Department; and

•is making purchases of telecommunication services that will be resold as such to the reseller’s customers.

A properly completed certiicate must be provided to the provider within 90 days after the provision of the telecommunication services. A certiicate of resale is not properly completed if it does not include the reseller’s sales tax Certificate of Authority number issued by the Tax Department.

A resale certiicate received on time that is not properly completed will be considered satisfactory if the deiciency is corrected within a reasonable period. You must also maintain a method of associating an invoice (or other source document) for an exempt sale made to a reseller with the resale certiicate you have on ile from that reseller.

Invalid exemption certificates

Sales of telecommunication services not supported by valid resale certiicates are deemed to be taxable excise tax sales. The burden of proof that the tax was not required to be collected is upon the provider.

Retention of exemption certificates

You must keep this certificate for at least three years after the due date of the return to which it relates, or the date the return was iled, if later.

This certiicate is valid only for purchases made on or after January 1, 2009.

To the reseller

Enter all the information requested on page 1. You may mark an X in the Blanket certificate box to cover all telecommunications services purchased for resale as telecommunication services. If you do not mark the Blanket certificate box, the certiicate will be deemed a

If you intentionally issue a fraudulent exemption certiicate, you will become liable for penalties and interest, in addition to the excise tax initially due. Some penalties that may apply:

•100% of the tax due

•$50 for each fraudulent exemption certiicate issued

If you do not resell as telecommunication services the telecommunications services purchased with this resale certiicate, report and pay the unpaid tax on Form

To the provider of telecommunication services

If you are providing telecommunication services and you accept a resale certiicate, you will be protected from liability for the tax if the certiicate is valid. The certiicate will be considered valid if it was:

•accepted in good faith;

•in your possession within 90 days after the provision of the service; and

•properly completed (all entries were made).

A certiicate is accepted in good faith when a provider has no knowledge that the resale certiicate is false or is fraudulently given, and reasonable care is exercised in the acceptance of the certiicate.

You must get a properly completed resale certiicate from the reseller no later than 90 days after the provision of the service. When you receive a certiicate after the 90 days, both you and the reseller are subject to the burden of proving that the sale was exempt, and additional documentation may be required.

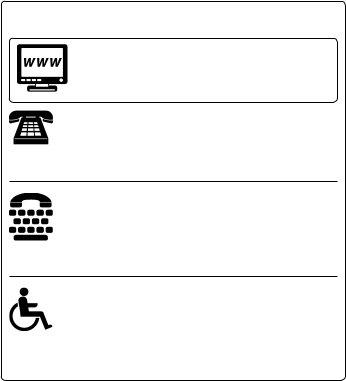

Need help?

Visit our Web site at www.tax.ny.gov

•get information and manage your taxes online

•check for new online services and features

Telephone assistance

Corporation Tax Information Center: (518)

To order forms and publications: |

(518) |

Text Telephone (TTY) Hotline (for persons with hearing and speech disabilities using a TTY): If you have access to a TTY, contact us at (518)

Persons with disabilities: In compliance with the

Americans with Disabilities Act, we will ensure that our lobbies, ofices, meeting rooms, and other facilities are accessible to persons with disabilities. If you have questions about special accommodations for persons with disabilities, call the information center.

Privacy notification

The Commissioner of Taxation and Finance may collect and maintain personal information pursuant to the New York State Tax Law, including

but not limited to, sections

social security numbers pursuant to 42 USC 405(c)(2)(C)(i).

This information will be used to determine and administer tax liabilities and, when authorized by law, for certain tax offset and exchange of tax information programs as well as for any other lawful purpose.

Information concerning quarterly wages paid to employees is provided to certain state agencies for purposes of fraud prevention, support enforcement, evaluation of the effectiveness of certain employment and training programs and other purposes authorized by law.

Failure to provide the required information may subject you to civil or criminal penalties, or both, under the Tax Law.

This information is maintained by the Manager of Document

Management, NYS Tax Department, W A Harriman Campus, Albany NY 12227; telephone (518)