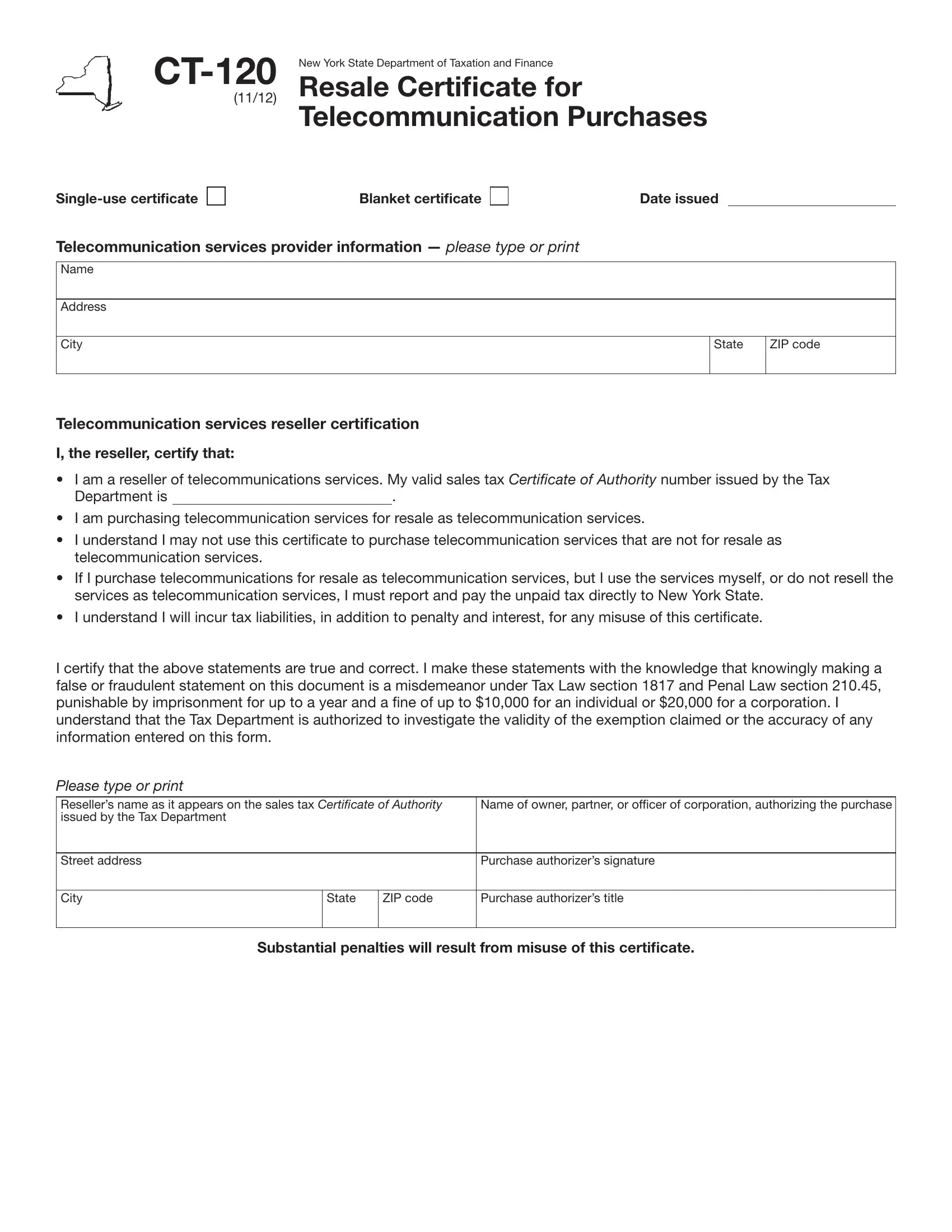

The CT 120 form is New York State's official resale certificate for telecommunication services. Under Tax Law, Article 9, section 186-e, registered New York sales tax vendors with a valid Certificate of Authority can purchase telecom services exempt from certain excise taxes, provided those services are resold to their customers. Vendors must complete this certificate before or at the time of purchase to establish the legitimacy of the tax exemption.

The form comes in two types. A single-use certificate applies to one specific transaction between a reseller and a service provider. A blanket certificate covers ongoing purchases of the same kind of service from the same provider, removing the need to issue a new certificate for every transaction. Resellers must supply their Certificate of Authority number and describe the telecommunication services purchased.

To qualify for the exemption, your business must be registered as a New York State sales tax vendor with an active Certificate of Authority. The services must be purchased specifically for resale to customers. If any portion of the purchased services will be retained for internal use, the exemption does not apply to that portion.

Service providers who receive a properly completed CT-120 certificate and act in good faith are protected from sales tax liability under New York law. Misuse of the certificate carries serious penalties, including 100% of the tax owed plus substantial fines and interest. Both buyers and sellers have legal responsibilities to ensure the certificate is used only for legitimate resale transactions.

For the standard New York resale certificate covering goods and services outside the telecom sector, see the ST-120 Resale Certificate form. For resellers also operating in Connecticut, the CT Resale Certificate may apply to your business as well.

| Question | Answer |

|---|---|

| Form Name | CT-120 (CT 120 Form) |

| Also Known As | New York Telecom Resale Certificate |

| Issuing Authority | New York State Department of Taxation and Finance |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | 120 york tax form, 120 certificate tax, 120 form state, 120 form tax |