Ct 5 1 Form is a document that is used to report on the wages of employees. This form is used to calculate the taxes that are owed by the employee and your business. The form must be completed accurately in order to ensure that you and your employees pay the correct amount of taxes. There are specific instructions that must be followed when completing this form, so it is important to understand its purpose and use. By understanding Ct 5 1 Form, you can comply with state tax laws and correctly report employee wages.

| Question | Answer |

|---|---|

| Form Name | Ct 5 1 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | Instructions for Form CT-5 Request for Six-Month Extension to ... |

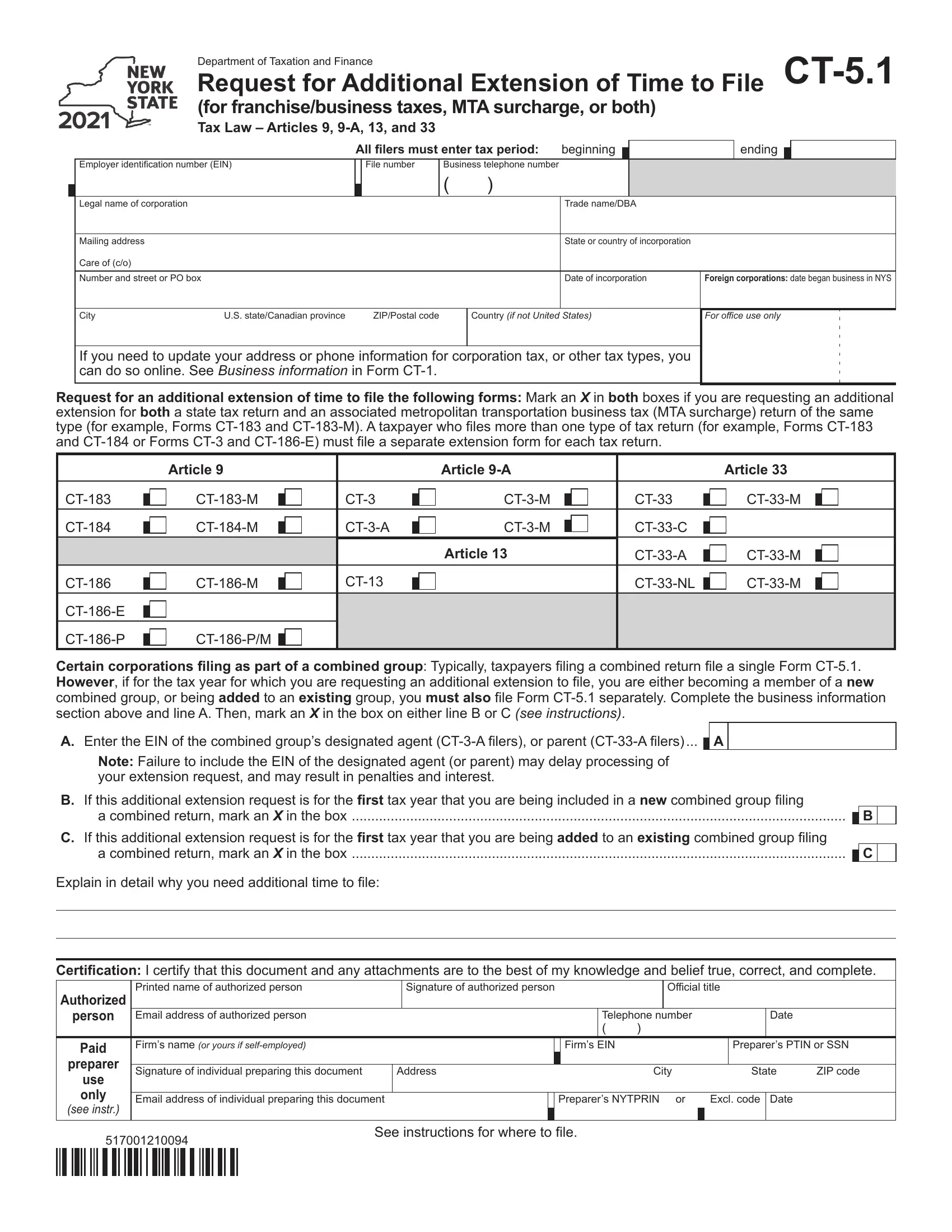

Department of Taxation and Finance |

|

Request for Additional Extension of Time to File |

|

(for franchise/business taxes, MTA surcharge, or both) |

|

Tax Law – Articles 9, |

|

|

All filers must enter tax period: |

beginning |

|

|

ending |

|

|

|

|

|

|

||||||

Employer identification number (EIN) |

File number |

Business telephone number |

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

||

|

Legal name of corporation |

|

|

|

|

Trade name/DBA |

|

|

|

|

|

|

|

|

|

|

Mailing address |

|

|

|

|

State or country of incorporation |

|

|

Care of (c/o) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and street or PO box |

|

|

|

|

Date of incorporation |

Foreign corporations: date began business in NYS |

|

|

|

|

|

|

|

|

|

City |

U.S. state/Canadian province |

|

ZIP/Postal code |

Country (if not United States) |

For office use only |

|

|

|

|

|

|

|

|

|

If you need to update your address or phone information for corporation tax, or other tax types, you

can do so online. See Business information in Form

Request for an additional extension of time to file the following forms: Mark an X in both boxes if you are requesting an additional extension for both a state tax return and an associated metropolitan transportation business tax (MTA surcharge) return of the same

type (for example, Forms

|

|

|

Article 9 |

|

|

|

Article |

|

|

Article 33 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Article 13 |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Certain corporations filing as part of a combined group: Typically, taxpayers filing a combined return file a single Form

A. Enter the EIN of the combined group’s designated agent

Note: Failure to include the EIN of the designated agent (or parent) may delay processing of

your extension request, and may result in penalties and interest.

B.If this additional extension request is for the first tax year that you are being included in a new combined group filing

a combined return, mark an X in the box |

|

B |

|

|

C.If this additional extension request is for the first tax year that you are being added to an existing combined group filing

a combined return, mark an X in the box |

|

C |

|

|

Explain in detail why you need additional time to file:

Certification: I certify that this document and any attachments are to the best of my knowledge and belief true, correct, and complete.

Authorized |

Printed name of authorized person |

|

Signature of authorized person |

|

|

|

Official title |

|

||||

person |

Email address of authorized person |

|

|

|

Telephone number |

|

|

Date |

|

|||

|

|

|

|

|

( |

) |

|

|

|

|

|

|

Paid |

Firm’s name (or yours if |

|

|

Firm’s |

EIN |

|

|

|

|

Preparer’s PTIN or SSN |

||

preparer |

|

|

|

|

|

|

|

|

|

|

|

|

Signature of individual preparing this document |

Address |

|

|

City |

|

State |

ZIP code |

|||||

use |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

only |

|

|

|

|

|

|

|

|

||||

Email address of individual preparing this document |

|

|

Preparer’s NYTPRIN or |

Excl. code |

Date |

|

||||||

(see instr.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

517001210094

See instructions for where to file.

Page 2 of 2

Instructions

General information

If you have already applied for an extension of time to file your return(s) and you still need more time, use Form

extension.

A corporation taxable under Article 9 with a valid

A corporation taxable under Article

A separate Form

New York S corporations may not use this form since they are not allowed an additional extension of time beyond six months.

Where to file

Mail this form to: NYS CORPORATION TAX

PO BOX 15180

ALBANY NY

Private delivery services

See Publication 55, Designated Private Delivery Services.

Approval of request for additional extension

Additional time to file your return will be allowed if you meet the following conditions:

–you have a valid reason for requesting additional time; and

–you have filed a valid request for a franchise/business tax or MTA surcharge return extension (Form

Having an additional extension of time to file your federal tax return does not extend the filing date of your New York

State franchise tax return.

Combined groups

The parent or designated agent of a new, or existing, combined group will file one Form

•Each taxpayer member corporation of a new combined group must also file a separate Form

•Each taxpayer member corporation being newly added to an existing combined group must also file a separate Form

Note:

Neither filing, nor the failure to file, a particular extension

request in any way impacts who must be included in a combined group.

When to file

File Form

current extension.

Signature

The document must be certified by the president, vice

president, treasurer, assistant treasurer, chief accounting

officer, or other officer authorized by the taxpayer corporation.

The document of an association, publicly traded partnership, or business conducted by a trustee or trustees must be signed by a person authorized to act for the association, publicly traded partnership, or business.

If an outside individual or firm prepared the document,

all applicable entries in the paid preparer section must be completed, including identification numbers (see Paid preparer identification numbers in Form

to sign the document will delay the processing of any refunds and may result in penalties.

Need help? and Privacy notification

See Form

517002210094