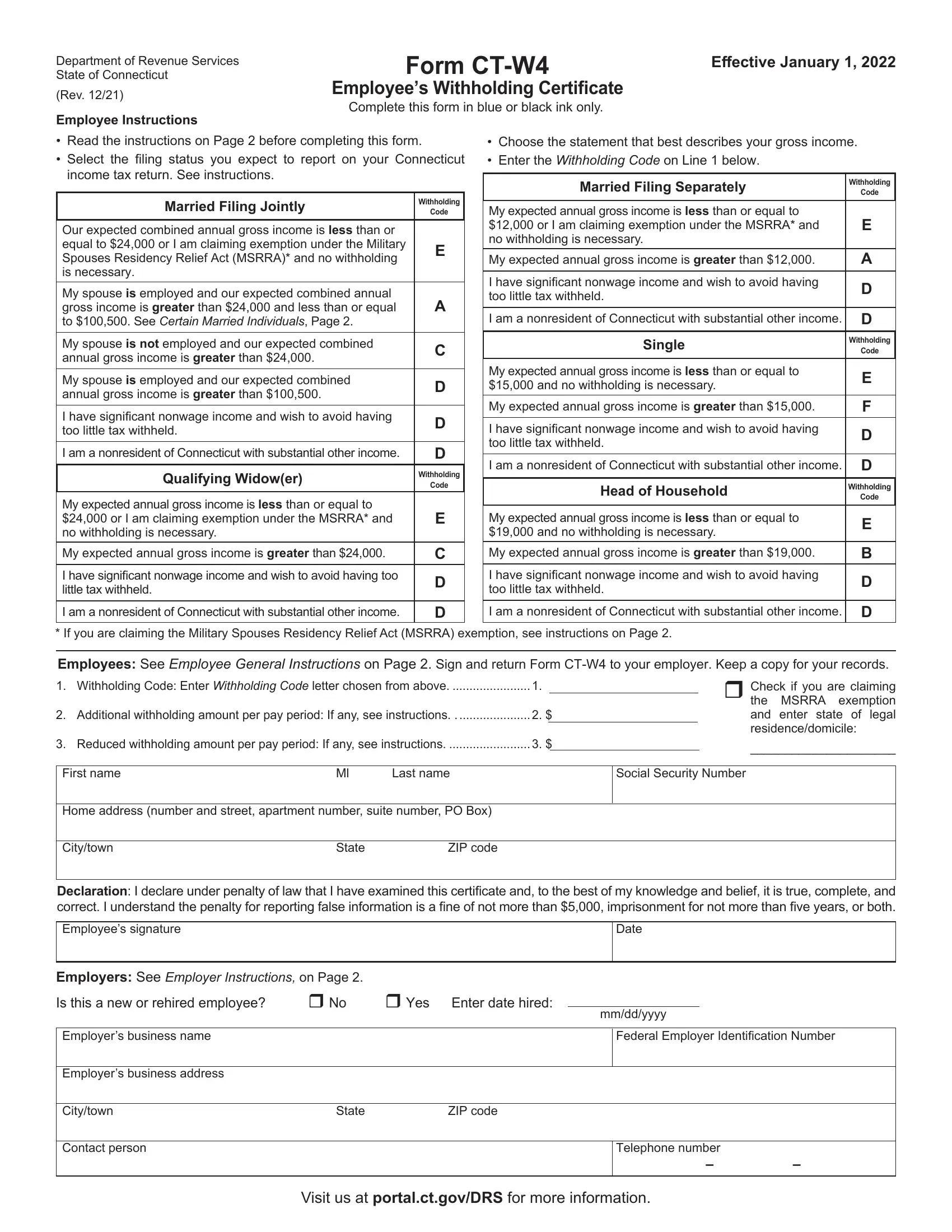

The CT-W4 form is the Connecticut Employee's Withholding Certificate. Employees give this form to their employer to set the correct amount of Connecticut income tax withheld from each paycheck. Submitting the right withholding code prevents a large tax bill or an oversized refund at the end of the year.

The form uses codes A through F to represent different withholding levels. Code A applies to single filers and married filers who want the maximum withholding. Code B applies to married filers whose combined gross income from all jobs is $100,500 or less. Code C applies when the combined income is more than $100,500 but not more than $200,500. Code D, E, and F apply to progressively higher income brackets. Employees should refer to the code chart on the back of the form to choose the code that best matches their expected filing status.

Line 2 lets employees enter a flat dollar amount to withhold in addition to the code amount. This option is useful when you have taxable income outside your regular wages, such as rental income or self-employment income. Entering an extra amount on Line 2 reduces the chance of an underpayment penalty.

Connecticut employers must keep a copy of every employee's CT-W4 on file. If an employee does not submit a completed form, the employer must withhold at the highest applicable rate. Employers must also report new and rehired employees to the Connecticut Department of Labor through the new hire reporting center at www.ctnewhires.com.

The back of the form includes a special section for nonresident employees and military spouses. A military spouse who qualifies as a Connecticut nonresident under the Military Spouses Residency Relief Act may claim an exemption from Connecticut income tax withholding by completing that section and giving the form to their employer.

| Question | Answer |

|---|---|

| Form Name | CT-W4 Form |

| Form Length | 2 pages |

| Fillable? | No |

| Fillable fields | 0 |

| Avg. time to fill out | 30 sec |

| Other names | how to fill out ct w4 form, ct w4 2021, ct w4, ct w4 fillable form 2021 |