E-585

Web-Fill |

Nonprofit and Governmental Entity Claim for Refund |

1-20 |

State, County, and Transit Sales and Use Taxes |

|

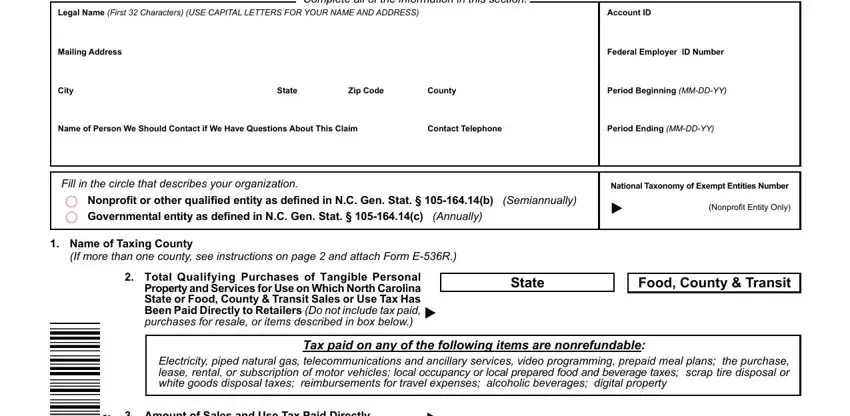

Complete all of the information in this section. |

|

|

|

Legal Name (First 32 Characters) (USE CAPITAL LETTERS FOR YOUR NAME AND ADDRESS) |

Account ID |

Federal Employer ID Number

City |

State |

Zip Code |

County |

Period Beginning (MM-DD-YY)

Name of Person We Should Contact if We Have Questions About This Claim |

Contact Telephone |

Fill in the circle that describes your organization.

Nonprofit or other qualified entity as defined in N.C. Gen. Stat. § 105-164.14(b) (Semiannually) Governmental entity as defined in N.C. Gen. Stat. § 105-164.14(c) (Annually)

National Taxonomy of Exempt Entities Number

(Nonprofit Entity Only)

1.Name of Taxing County

(If more than one county, see instructions on page 2 and attach Form E-536R.)

|

2. Total Qualifying Purchases of Tangible Personal |

|

|

State |

|

Property and Services for Use on Which North Carolina |

|

State or Food, County & Transit Sales or Use Tax Has |

|

|

Been Paid Directly to Retailers (Do not include tax paid, |

|

|

purchases for resale, or items described in box below.) |

|

Tax paid on any of the following items are nonrefundable:

Electricity, piped natural gas, telecommunications and ancillary services, video programming, prepaid meal plans; the purchase, lease, rental, or subscription of motor vehicles; local occupancy or local prepared food and beverage taxes; scrap tire disposal or white goods disposal taxes; reimbursements for travel expenses; alcoholic beverages; digital property

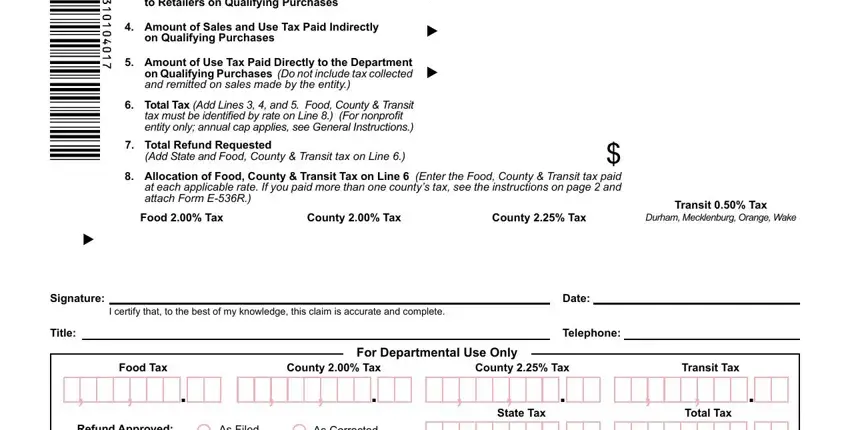

3.Amount of Sales and Use Tax Paid Directly to Retailers on Qualifying Purchases

4.Amount of Sales and Use Tax Paid Indirectly on Qualifying Purchases

5.Amount of Use Tax Paid Directly to the Department on Qualifying Purchases (Do not include tax collected

and remitted on sales made by the entity.)

6. |

Total Tax (Add Lines 3, 4, and 5. Food, County & Transit |

|

|

tax must be identified by rate on Line 8.) (For nonprofit |

|

|

entity only; annual cap applies, see General Instructions.) |

|

7. |

Total Refund Requested |

$ |

|

(Add State and Food, County & Transit tax on Line 6.) |

8.Allocation of Food, County & Transit Tax on Line 6 (Enter the Food, County & Transit tax paid at each applicable rate. If you paid more than one county’s tax, see the instructions on page 2 and attach Form E-536R.)

Food 2.00% Tax |

County 2.00% Tax |

County 2.25% Tax |

Transit 0.50% Tax

Durham, Mecklenburg, Orange, Wake

I certify that, to the best of my knowledge, this claim is accurate and complete.

For Departmental Use Only

. |

, |

County 2.00% Tax |

, |

County 2.25% Tax |

, |

. |

, |

. |

|

|

|

|

, |

State Tax |

. |

As Filed |

|

As Corrected |

, |

|

|

|

|

By: |

|

Date: |

|

|

|

|

|

|

MAIL TO: NC Department of Revenue, P.O. Box 25000, Raleigh, NC 27640-0001 |

|

Line by Line Instructions

Page 2, E-585, Web-Fill, 1-20 |

General Instructions |

Use blue or black ink to complete this form. An Account ID is required to process the claim.

This form is to be filed by the following entities as specified:

-Nonprofit or other qualified entities as permitted in N.C. Gen. Stat. § 105-164.14(b): A claim for refund of taxes paid during the first six months of the calendar year is due to be filed by October 15 of that year. A claim for refund of taxes paid during the last six months of the calendar year is due to be filed by April 15 of the following year. Enter the National Taxonomy of Exempt Entities (“NTEE”) classification code for the entity. The NTEE code system is used by the Internal Revenue Service and the National Center for Charitable Statistics to classify nonprofit organizations. Organizations properly classified in any of the following major group areas of the NTEE do not qualify for a refund: Community Improvement and Capacity Building, Public and Societal Benefit, and Mutual and Membership Benefit.

For a nonprofit entity, the total State sales and use tax refund amount for both six month periods may not exceed $31,700,000 for the State’s fiscal year and the total Food, County & Transit tax refund amount for both six month periods may not exceed $13,300,000 for the State’s fiscal year.

A hospital not listed in N.C. Gen. Stat. § 105-164.14(b) is only allowed a semiannual refund of sales and use taxes paid by it on over-the-counter drugs purchased for use in carrying out its work.

-Governmental entities as permitted in N.C. Gen. Stat. § 105-164.14(c): Claims for refund are due on a fiscal year basis within six months of the close of the fiscal year of the claimant. A refund for only the Food, County, & Transit sales and use tax for local school administrative units and joint agencies created by interlocal agreement among local school administrative units pursuant to N.C. Gen. Stat. § 160A-462 are authorized in N.C. Gen. Stat. § 105-467(b).

Records must be maintained, and distinguish the following information on a county by county basis: qualifying purchases of tangible personal property and services; State, county & transit tax paid directly to retailers on qualifying purchases for use as shown on sales receipts and invoices; State, county & transit tax paid indirectly on qualifying purchases of building materials, supplies, fixtures, and equipment as shown on certified statements; and State, county & transit tax paid directly to the Department of Revenue.

Records must be maintained for qualifying direct purchases and qualifying indirect purchases as follows:

-Qualifying direct purchases - Adequate documentation for tax paid directly to the vendor is an invoice or copy of an invoice that identifies the item purchased, the date of the purchase, the cost of the item, and the amount of sales or use tax paid. Reimbursements for travel expenses to an authorized person of the entity are not considered to be a direct purchase; therefore, the sales or use tax paid on such are not refundable.

-Qualifying indirect purchases - Adequate documentation for sales or use tax paid on qualifying indirect purchases is a certified statement from the real property contractor or other person that purchased the items. The statement must indicate the date the property was purchased; the type of property purchased; the name of the person from whom the purchase was made and the invoice number of the purchase; the purchase price of property purchased and the amount of sales and use tax paid thereon; the project for which the property was used; if the property was purchased in this State, a copy of the sales receipt and the statement must include the county in which it was delivered; and if the property was not purchased in this State, the county in North Carolina in which the property was used must be included. Only sales and use taxes paid on building materials, supplies, fixtures, and equipment that become part of or annexed to a building or structure that is owned or leased by or is being erected, altered, or repaired for use by the nonprofit entity for carrying on its nonprofit activities or by the governmental entity are sales and use tax paid on qualifying indirect purchases eligible for refund.

For a claim for refund filed within the statute of limitations, the Department must take one of the following actions within six months after the date the claim for refund is filed: (1) send the taxpayer a refund of the amount shown due on the claim for refund; (2) adjust the amount of the refund shown due and send the taxpayer a refund of the adjusted amount; (3) deny the refund and send the taxpayer a notice of proposed denial; or (4) request additional information from the taxpayer. If the Department does not take one of the actions within six months, the inaction is considered a proposed denial of the requested refund. A taxpayer who objects to a proposed denial of a refund may request a Departmental review of the proposed action by filing a Form NC-242, Objection and Request for Departmental Review within the time provided in N.C. Gen. Stat. § 105-241.11. If the Department selects a claim for refund for examination, the taxpayer has the same rights that the taxpayer would have during an examination of a return by the Department. If the Department determines that a claim for refund was not filed within the statute of limitations, the refund request will be denied and the Department will issue a notice of proposed denial of refund.

For a full explanation of the Departmental review process, refer to the North Carolina Taxpayers’ Bill of Rights found at www.ncdor.gov or the provisions of N.C. Gen. Stat. § 105-241.11.

If you have questions about how to complete this form, more detailed instructions can be found on our website at www.ncdor.gov or call the Department at 1-877-252-3052 (toll-free).

Line 1 - If all taxes were paid in only one county, enter the name of that county. If you made purchases and paid county & transit tax in more than one county, do not list a county on Line 1.

For Lines 2 through 6, local school administrative units and associated joint agencies should only complete the Food, County & Transit column.

Line 2 - Enter in the State column the total amount of qualifying purchases of tangible personal property and services for use on which State sales or use tax was paid to retailers. The taxable purchase price of a modular home, manufactured home, boat, or aircraft is included in the State column only. Enter in the Food, County & Transit column the total amount of qualifying purchases of tangible personal property and services for use on which food, county & transit sales or use tax was paid to retailers.

For Lines 3 through 6, State tax must be entered in the State column and food, county & transit tax must be entered in the Food, County & Transit column.

Line 3 - Enter the amount of sales and use tax paid directly to retailers on qualifying purchases for use, as shown on sales receipts or invoices. Do not include tax paid on nonrefundable purchases as described in the box on the front of claim form.

Line 4 - Enter the total amount of sales and use tax paid indirectly on qualifying purchases of building materials, supplies, fixtures, and equipment as shown on certified statements from real property contractors or other persons.

Line 5 - Enter the total amount of use tax paid to the Department by the entity on its sales and use tax returns for qualifying purchases. Do not include tax collected and paid on taxable sales made by your entity.

Line 6 - Add the amounts of tax by column on Lines 3, 4, and 5 and enter the sum.

Line 7 - Add the State and Food, County & Transit taxes on Line 6 and enter the sum. This is the total amount of refund requested for the period.

Line 8 - Allocate the amount of county and transit taxes included on Line 6 in the Food, County & Transit Tax column to the applicable rate. If county or transit tax was paid for more than one county, complete Form E-536R, Schedule of County Sales and Use Taxes for Claims for Refund, to identify the applicable rates and individual counties to which tax was paid for the period. The total of all entries on Form E-536R must equal the food, county and transit tax shown on Line 6.

For nonprofit entity only: If the total entries of food, county, & transit tax on Form E-536R for both six month periods exceeds $13,300,000 for the State’s fiscal year, then each entry of the food, county, & transit tax for both six month periods on Form E-536R must be proportionally reduced to the refund cap of $13,300,000 for the State’s fiscal year. Contact the Department for assistance.

®

® ,

,

,

,

,

,

,

,

,

,

,

,

,

,